Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

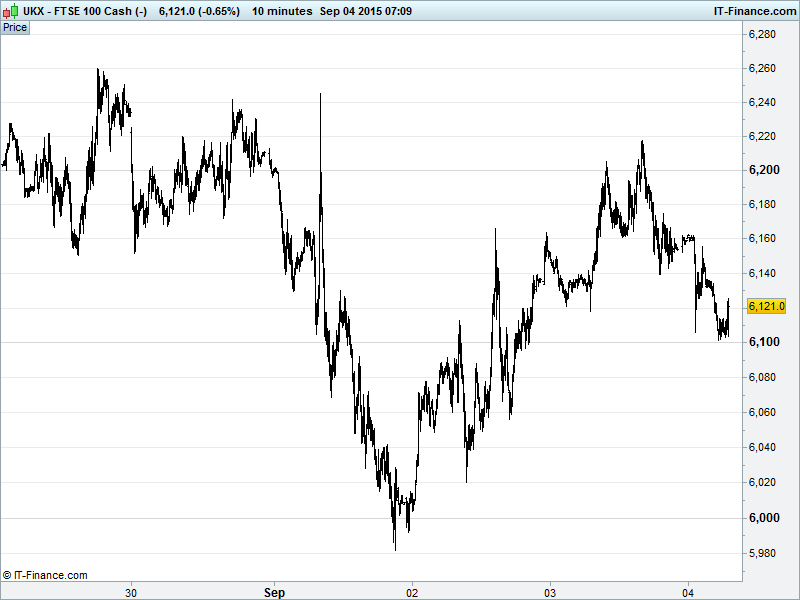

UK 100 Index called to open -75pts at 6120 having retreated from its post-ECB/Draghi highs of 6215 to trade around the Aug trend-line of falling highs above which we tested yesterday. As expected, a bettering of 6260 late-Aug highs still likely required before the bulls rush back in. We note overnight support 6100 keeping alive uptrend from 23 Aug multi-year lows. Watch levels: Bullish 6170, Bearish 6090.

The negative opening call comes after Asian markets voted for risk-off in the run-up to the US jobs report. This is in stark contrast to yesterday’s positive European and US sessions following a very dovish ECB message (growth + inflation forecasts cut; might need to be cut more) with President Mario Draghi highlighting downside risks (China, Emerging markets, volatility, strong Euro, deflation threat) and his institution’s willingness to bolster its radical QE stimulus programme.

Markets typically cautions ahead of the monthly US Non-Farm Payrolls Jobs Report which is sure to spice up the debate on whether the US Federal Reserve has enough proof that an interest rate hike is both wearable and warranted from historic lows or whether low inflation and market volatility will see it hold off until year-end or even next year as the IMF would appear to prefer.

A fade in the rally by US stocks provided a weak handover to Asia bourses (China still closed thankfully) while weak Japanese Cash earnings and a stronger JPY (safehaven seeking) helped the Nikkei make fresh September lows. However, Australia’s ASX higher thanks to progress by Miners following Rio Tinto’s upbeat China outlook and despite a weak AUD amid concerns China will reduce support for its stock market when post-holiday trading resumes on Monday.

US stock traders attempted to stay on the side-lines ahead of today’s Non-farms Jobs report. Many were tempted back into the fray, however, by the siren that was a dovish Mario Draghi, indicating that the ECB will continue to do whatever it takes to get sluggish Eurozone inflation moving towards that 2% target.

Low oil blamed as usual (not wrongly) for that while recent EM volatility deemed a temporary headwind to market sentiment. US bourses climbed in the immediate aftermath of Draghi’s speech before coming back into the close. A positive US jobs report today likely to push the EUR/USD below 1.10.

Fed chatter included Mineapolis chief Narayana Kocherlakota saying what the doves always say – that inflation is nowhere near where it should be to warrant a September US rate rise and that hiking rates now would serve only to further stifle inflation growth.

In focus today….well it’s all about the US Jobs Report this afternoon (consensus 215K), however, without a blowout (300K) or disastrous number (100K) we still doubt the Fed will hike this month given market volatility, China concerns and inflation still MIA. Watch Unemployment and Participation rates for underlying jobs market trend as well as Wages for clues on consumer confidence and key inflation.

After the Fed’s Kocherlakota said inflation too low for a rate hike, watch what Lacker has to say just before the Jobs report given that the title of his speech is “The Case Against Further Delay”. Thereafter we have the ECB’s Nowotny and German Chancellor Merkel speaking before the weekend.

Crude prices took a round trip – around that ECB press conference – to trade flat. Brent (now $50) touching $53 and WTI (now $46) getting close to $49, neither managing to break Sept highs before returning to pre-Draghi levels on a stronger USD, low Asia volume and the reality of swollen US storage facilities.

Gold ($1125) set for a second week of declines spurred by a stronger USD, especially against the Euro, and Chinese public holidays sapping volume. What traders there are in the market continue to be wary of taking up fresh positions ahead of US non-farms with all eyes on what that will mean for US monetary policy and ergo where risk-averse investors should park their cash.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – it’s all part of the service.

UK Company Headlines: (Source: Reuters/DJ Newswires)

- GVC Holdings reached agreement with Bwin.party on terms of recommended offer. Scupper BWIN deal with 888

- AstraZeneca says US FDA approved new dose of its blood thinner, Brilinta, for patients with a history of heart attack

- August was the worst month for British retail sales since the global financial crisis of 2008

- British retailer John Lewis said department store sales were down 3.4 percent in the latest week

- Aer Lingus August load factor rises to 90.3 pct

- Ladbrokes says Darren Shapland to retire from non – exec role