Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

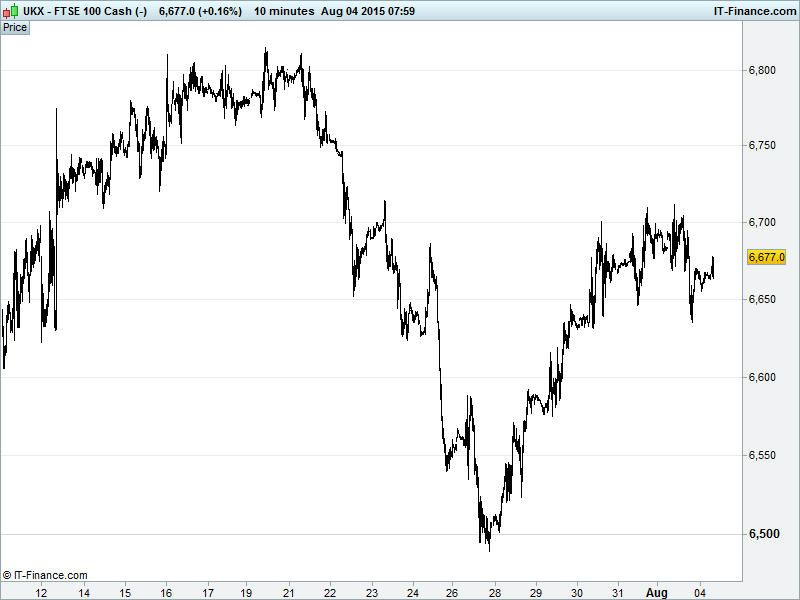

UK 100 Index called to open -25pts at 6665 with 6710 remaining resistance yesterday and the index dropping back to probe below 6650 overnight. Having recovered from overnight lows this puts the index in a 6650-6700 4-day range. The bulls will be hoping this serves as a sideways pause for digestion of the rebound from 6500 lows while the bears will be looking for a breakdown towards 6600. Updated watch levels: Bullish 6715, Bearish 6630.

The negative opening call comes as the commodity price slide continues to dampen investor sentiment with copper approaching bear market status, Gold holding 5yr lows, Platinum at its lowest since Jan 09 and Brent Crude testing <$50. With markets already worried about Chinese growth and a strong USD ahead of a US rate rise, some apprehension in the run-up to Friday’s Non-Farms jobs report and disappointing US data adding fuel to the fire.

US equities were dragged lower by steepening declines in the oil price (-50% since last summer) holding back Energy stocks and poor stateside macro data adding to doubts about the Fed’s plan to raise rates as soon as September. US manufacturing declined, prices paid slumped and construction slowed, while US Personal Spending growth fell back despite Personal Income growth remaining solid. Note negative revisions to the prior month for both.

Asian stocks mostly higher overnight despite weak cues from Wall Street and stiff commodity price headwinds (copper, rubber both now in bear market territory) which are hurting the UK’s listed miners (see UK Index laggards above for a who’s who). China’s stock market in the green for the time being after the People’s Government took further action to curb volatility by getting tough on short sellers.

In Australia, the RBA left interest rates unchanged, as expected, while a marked difference in language when referring to the AUD sent the currency higher. References to the likelihood (and necessity) of further depreciation were dropped amid growing optimism in the labour market as a spate of positive macroeconomic readings came through, beating consensus and carrying upward revisions to last month’s figures. Note however the EUR/AUD pair approaching the floor of a 3-month rising channel which could lead to a bounce and re-test of the 1.51 level this week.

In Europe, reports that the ECB may not need to raise emergency lending (ELA) to Greek banks thanks to capital controls reducing deposit outflows was offset by S&P downgrading its outlook for the EU from stable to negative even if it kept the rating at AA+.

Note China still clutching at straws, now implementing curbs on short selling in order to freeze out day-traders to reduce volatility and stabilise the world’s #2 equity market. Curbs have seen China lose its title as most liquid stock market with trading suspensions and regulatory efforts to outlaw any form of Bearishness seeing investors shy away.

In bank-land the UK government last night began selling-down its 78% bailout stake in RBS by placing ~£2bn/5.4% of shares with institutional investors at 330p, a 2.25% discount to yesterday’s 337.6p closing price and well below the 502p paid for the £45bn bailout in 2008 and the 407p at which the Chancellor says the UK taxpayer would breakeven.

In focus today – Eurozone Producer Price Inflation seen remaining anything but inflationary, while US Factory Orders are forecast to rebound in June although US Economic Optimism is expected to give up a little ground in August.

Brent crude testing sub $50 levels while US Light now below $46. Monday’s 4% losses pared slightly but not in any meaningful way just yet with OPEC pumping around 30m barrels into the market every day and the situation set to worsen once Iran gets in on the action with its 1m bpd output target. Low demand from China widely believed to be priced in already, but you’d be mad to take both eyes off the world’s #2 economy for further commodity price drivers.

Gold ($1088) has bounced back from near 5.5yr lows but is failing to better resistance $1089. Volatility in the USD well mirrored in the dollar-denominated yellow metal this morning, while a potential Fed rate hike in September will be putting added pressure on the non-interest bearing safe haven. Investors also looking past poor US manufacturing data and on towards Friday’s non-farms print for cues.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – it’s all part of the service.

UK Company Headlines: (Source: Reuters/DJ Newswires/Bloomberg)

- Standard Life H1 operating profit +6 %

- Rolls – Royce shares rise as activist stake fuels turnaround talk

- METALS – London copper struggles near six – year lows on growth concerns

- Just Eat raises FY revenue expectations to around £230m

- UK house prices edge up in July – Nationwide

- Travis Perkins says trading in line with forecasts

- Meggitt on track as military orders offset energy declines

- Pendragon sees full – year performance ahead of expectations

- Rotork H1 pretax profit £56.3m vs £61.5m

- Direct Line H1 pretax profit from cont ops almost doubles

- Fresnillo cuts 2015 capex to $570m

- Spirax-Sarco sells M&M International to Rotork for €9.7m

- UK starts RBS sell-off with $3.3bn stake sale

- Morgan Sindall full-year expectations remain unchanged

- Glencore starts "business rescue" at South Africa coal unit