Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

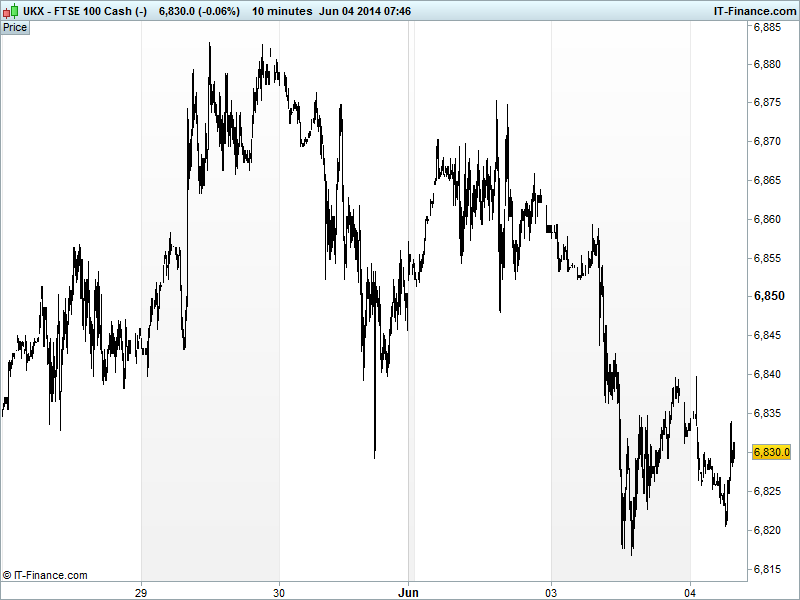

UK 100 called to open flat at 6830 after US bourses closed with small losses and Asia mixed, taking a pause after the run of recent highs and despite solid US macro data (Factory Orders, Econ Optimism, vehicle sales) and following hawkish rhetoric by the Fed’s George favouring an earlier rate rise. Apprehension still dominating sentiment ahead of key risk events: ECB action and US jobs report.

China a notable underperformer in Asia after Vice Environment Minister said pollution control may affect GDP growth, while Japan’s Nikkei has just gone positive helped by improved PMI Services and a weaker JPY.

Australia’s ASX in the red, and AUD/USD back from its 0.93 spike highs, following/despite a stellar GDP report with growth accelerating to the fastest in nearly 2 years, and AIG Services improving to near breakeven, supporting Treasurer Hockey saying the transition from mining is underway and the economy resilient.

Bloomberg reports that ECB President Draghi is likely to signal tomorrow that any interest rate cut this week won’t necessarily be the last when he announces measures to help counter the region’s deflationary threat. With EUR/USD down around 1.36, if a rate cut, and maybe more, priced in?

On the other side of the pond, the WSJ’s also reports that Fed officials are nervous about market complacency and lack of volatility in the markets.

The UK index is back around recent support at 6830 having been as low as 6820 and as high as 6840 overnight (another limited trading range today?). The downtrend from end-May persists, with potential for pressure (risk event disappointment?) to result in a fall-back to lows of 6770 which could be the correction needed before another rally.

In focus this morning we have Eurozone PMI Services where growth should be confirmed by all but France, with Spain, Germany and UK doing best. The second estimate for Eurozone GDP and PPI are expected to be confirmed at the preliminary readings although any downward revisions would likely pile the pressure on the ECB ahead of tomorrow’s key policy decision.

In the afternoon, the US ADP employment change will be considered a warm-up for Friday’s Non-Farm Payrolls - gains of 200K expected for both. The US Trade Deficit is seen unchanged while US PMI Services may have given up a little ground but the ISM Non-Manuf gained – both well in growth territory. The evening sees the US Beige book published which could impact late trading sentiment.

In commodities, Gold has settled around the $1245/oz, in-line with the pause in equities as traders await the latest updates on ECB policy and US jobs situation. Pause before recovery, or resumption of downtrend?

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – all part of the service.

Overnight Macro Data: (Source: Reuters/DJ Newswires)

- UK BRC Shop Price Index Worse, failed to improved

- AU AIG Services Perf Improved

- AU GDP Better, accelerated

- JP PMI Services Improved, still contracting

- IN HSBC PMI Services Improved, back to growth

See Live Macro calendar for full details

UK Company Headlines: (Source: Reuters/DJ Newswires)

- Tesco's British sales slide worsens

- Synergy Health FY adj. pretax profit rises to 54.7 mln stg

- Blaze at Dutch Shell chemical plant extinguished, two hurt

- Workspace Group FY net asset value jumps 43 pct

- Monitise names former Visa executive as co-CEO

- RPC group revenue up 7 percent on organic growth, acquisitions