Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

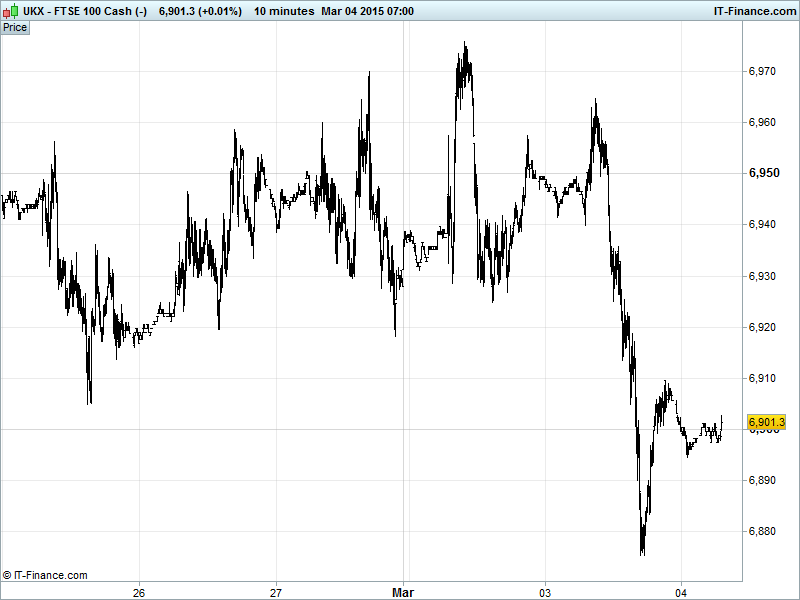

UK 100 called to open +10pts at 6900, making a recovery from yesterday’s lows of 6875 but likely hindered by the now breached Feb rising support. Still in uptrend from mid-December but with potential for a consolidation pause to digest the gains of the last 6 weeks and recent progress to make fresh all-time highs. Watch levels: Bullish 6920, Bearish 6870.

The positive open comes after HSBC China PMI Services edged up from a six month low in February, reviving confidence in the world’s #2 economy, coupled with the PBOC adding to recent stimulus measures but cutting short-term lending rates to banks which offset a weak US finish and disappointing Aussie GDP.

US markets closed in negative territory after US Auto sales disappointed and Israeli PM Netanyahu delivered some fairly aggressive rhetoric regarding Iran and its potential for nuclear armament. There were also worries about Greece’s finances with talk of it being forced to tap into cash reserves, pension funds and other public sector entities to cover short-term needs.

Asian markets tracked US peers into the red, although India’s Sensex hit 30,000 for the first time after the RBI cut rates, with HSBC China PMI Services improvement in February failing to offset Japan’s reading falling into contraction. While Australia saw a rebound in its services sector, Q4 GDP growth missed expectations, the slowest annual growth in a year, adding to calls for another RBA rate cut after it stayed put yesterday, especially after negative comments from the RBA’s Edwards on growth/unemployment.

Japan’s Nikkei un-helped by a stronger USD/weaker JPY or BoJ Kuroda’s comments that little chance of confidence in policy being lost and that adjustments (more stimulus) can be made is necessary. China stocks benefiting from Services PMI data and PBOC cutting interest rates on its short term lending facility (SLF) for local branches and tripling the funds available to bring down financing costs.

In focus in Europe today we have PMI Services readings which are expected to show growth decent across the board, and improvements in many cases. Eurozone Retail Sales growth seen slowing slightly in January, while the US ADP Employment Change (NFP warm-up) is expected to show a higher number of jobs added in Feb. US PMI Services seen improving nicely and US EIA Crude Oil Inventories forecast to show another build, but less than the prior week echoing the API data from yesterday.

Oil traded up marginally overnight with API data showing a lower than expected rise in US crude and Iran nuclear talks leaving traders concerned about a possible flood of Iranian crude to the market. Brent pulled back slightly from its Tuesday highs to trade around $60 this morning with support at rising Feb lows but possible hindrance at falling Feb highs. US Light ($50), hovering around a flat line this morning in anticipation of more closely watched EIA data due this afternoon, remains in a tentative recovery from 26-Feb lows with similar support and resistance.

Gold ($1206) rose slightly in choppy Asian trading overnight while remaining essentially range bound due to a dearth of meaningful economic drivers leaving simple supply and demand factors to do the work. The safe haven commodity broke below its rising Feb channel with potential for further downside this week beneath falling resistance from the beginning of the month.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – it’s all part of the service.

Key Overnight Macro Data: (Source: Reuters/DJ Newswires)

- UK BRC Shop Price Index Miss, Deteriorated

- Japan Services PMI Deteriorated

- China Services PMI Improved

See Live Macro Calendar for full data line-up, incl. consensus expectations

UK Company Headlines: (Source: Reuters/DJ Newswires)

- Lookers sees more growth this year after 2014 profits rise

- ITV to return 250 mln stg via special dividend

- British baker Greggs reports 41 pct jump in annual profit

- Exova full – year underlying organic revenue rises 4 pct

- Melrose FY headline pretax profit up 21 pct

- Legal & General 2014 operating profit rises 10 percent

- Carillion wins 1.5 bln stg 6 – year contract from Scape

- Novae Group says FY profit rose to 62.6 mln stg

- Subsea 7 axes dividend, sees lower 2015 earnings due weak market

- Miner Fresnillo's full – year profit falls on low silver, gold prices

- Eurocell announces IPO offer price of 175 pence per share

- Great Portland Estates pre-lets Oxford Street store to New Look

- Afren says not to pay $15 mln interest under 2016 notes due Feb 1