Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

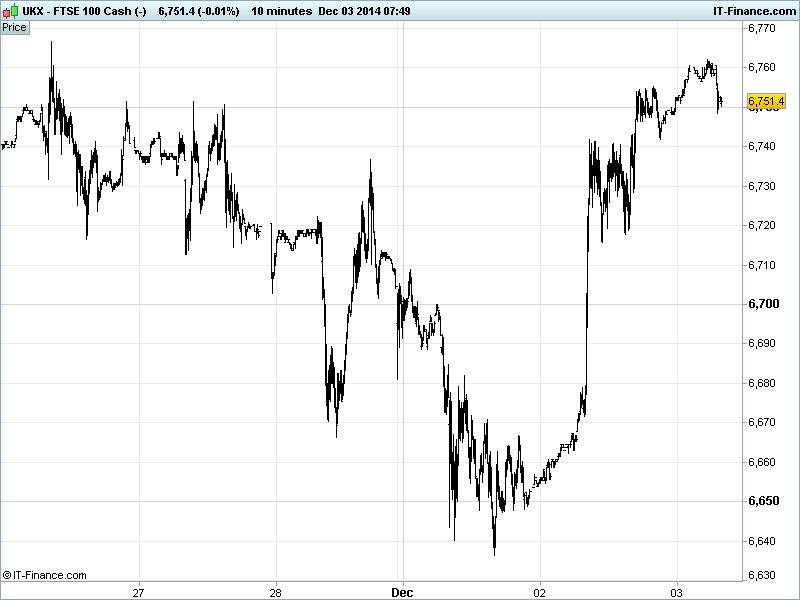

UK 100 Index called to open +15pts at 6750, having rallied back to late-Nov highs, a re-enactment of the 20 Nov bounce. After the sharp move higher, the risk is that momentum cools ahead of the ECB meeting on Thursday (QE or not QE?) and US Jobs report on Friday. Any break higher, open up September highs 6900, while any retracement could see a revisit of recent lows. Watch levels: Bullish 6780 and Bearish 6730.

The positive opening call stems from a positive US finish on upbeat data, some talk of US tax break extensions, Oil’s rebound on speculation of OPEC pain and M&A speculation (BP/RDS) helping commodities.

This is combined with overnight Chinese PMI Services data showing small improvements (quickest growth for new orders in 2.5ys), suggesting the sector is helping weather property downturn, appeasing worries related to slowing growth in the world’s #2 economy.

US equities benefited from upbeat data in the form of strong November Auto Sales along with better than expected ISM New York and a bigger rebound in Construction Spending. Note hawkish (USD positive) commentary from the Fed’s Fischer saying FOMC close to dropping ‘considerable time’ language in relation to rates staying low.

Overnight, Asia largely positive on US lead, with Japan’s Nikkei still benefiting from a strong USD and weak JPY (7yr low) as well as a return to growth for the nation’s PMI Services and read-across from US auto sales.

Downunder, Australia’s ASX buoyed by Japan/China PMIs which has offset its own disappointing GDP print underscoring growth concerns and a ‘disturbingly weak’ Services sector (14-month low), both adding to existing AUD weakness (lowest since Jul 2010) via the rampant USD.

In focus, we have Eurozone PMI Services, where final November readings are seen confirming France still in contraction, Germany giving up some growth and thus the region doing so too. Anything disastrous could help force the ECB’s hand tomorrow (although an FT piece says it is destined to disappoint). The UK is expected to maintain its strength of growth (70% GDP) while Eurozone Retail Sales are forecast to have rebounded in October.

In the afternoon, the US ADP Employment Change (Non-Farm Payrolls warm-up act ahead for Friday) is seen pretty stable in November (in-line 4-month average)while US PMI Services, is seen edging lower, but maintaining a strong reading, and ISM Non-Manufacturing is even forecast to edge higher. The Fed releases its Beige Book economic assessment update in the evening.

In commodities, Gold is being held back below its 5-week high $1220 by a strong USD damping demand for the store of value/safehaven. The strong USD comes from the Oil rebound and Fed talk of language change related to how long rates will stay low. Happy trading around $1200 for now though.

After Oil’s rebound on hopes of continued global central bank stimulus, momentum has waned seeing the downtrend from late November resume. The rampant USD is hurting along with OPEC’s decision to prolong the game of chicken with the US on production levels. US Light Crude back below $68 with Brent around $70.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – it’s all part of the service.

Key Overnight Macro Data: (Source: Reuters/DJ Newswires)

- UK BRC Shop Price Index Still weak

- AU GDP Miss, Growth slowed

- CN PMI Non-Manufacturing Ticked up

- JP PMI Services Back to growth

- CN HSBC PMI Services Ticked up

- CH GDP Beat, Accelerated

See Live Macro Calendar for full data line-up, incl. consensus expectations

UK Company Headlines: (Source: Reuters/DJ Newswires)

- Chesnara says CEO Graham Kettleborough to resign from company

- Esure says Dame Helen Alexander and Anthony Hobson to step down

- Max Petroleum says working on restructuring loan from Sberbank

- Antofagasta appoints mining division CEO

- Sage says on track to meet 2015 targets

- Brewin Dolphin FY pretax profit down 70 pct to 8.6 mln pounds

- Kenmare appoints new COO

- Lloyds sells portfolio of Irish mortgages to Goldman Sachs and CarVal