Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

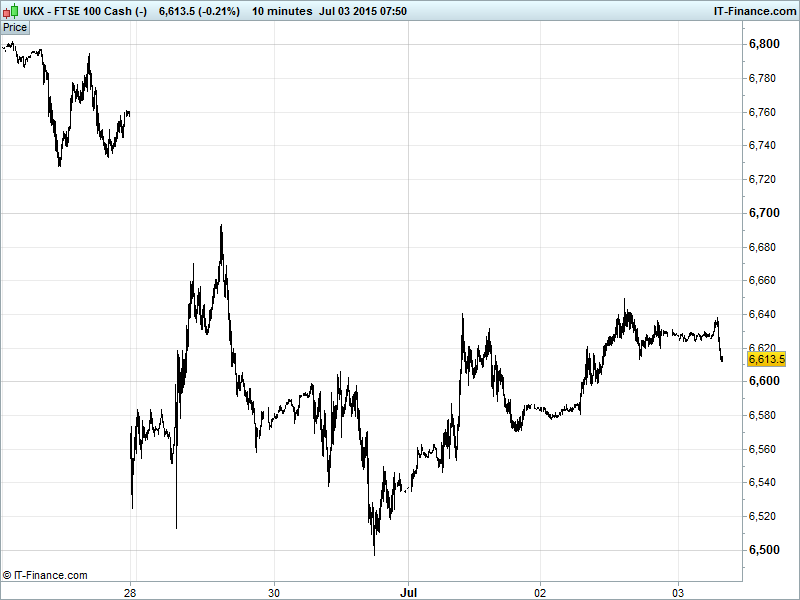

UK 100 Index called to open -15pts at 6815, having traded largely sideways overnight. The short-term uptrend from Wednesday’s 5.5-month lows 6495 remains intact, although 6650 has proved a hurdle. While holding above 6600 is positive, downtrend from 7050 at end-May holds firm. Bulls still hoping to challenge Monday’s 6695 highs and close the gap, while Bears want 6650 to stay troublesome and deliver a retrace to 6500. Watch levels: Bullish 6660, Bearish 6560.

The negative opening call comes with continued uncertainty on Greece and despite a slightly softer than expected US non-farms report that poured cool water on the likelihood of an imminent rise in US interest rates, the news not being welcomed by markets here in the UK, whose own central bank (the BoE) is sure to follow suit when the Fed does eventually decide to hike. Bigger fish to fry in Europe, clearly.

Fed hawks still looking at September or December for lift-off, with irritable-sounding commentary that a rate rise should now be ‘gotten on with, even if the data doesn’t support it’ while many traders (us included) betting on a further delay until 2016.

US bourses (shut today for Independence Day) themselves closed negative with Greece also eclipsing non-farms on the other side of the pond ahead of Sunday’s planned and closely-called ‘Greferendum.’ In an important change of tune, the IMF has now come out in favour of giving Greece some leeway, indicating to fellow creditors that it would not be willing to enter into a third bailout programme without demands for economic reform being accompanied by some debt relief for Athens.

With creditors still refusing to engage with Tsipras & Co. until after the referendum, the Greek PM continues to urge the people to vote ‘no,’ assuring them that he will get them a better deal in Brussels on Monday if they do so. Finance Minister Varoufakis has staked his job on it saying he will resign in the case of yes vote.

Asian markets mixed and swinging with investors very much on edge after what is now considered a weak US jobs report (in-line but downward revisions, low wage growth, low participation) and ahead of Sunday’s Greek bailout referendum; a ‘No’ vote seen hurting markets, a ‘Yes’ vote delivering a Grelief rally. Greek banks closer to collapse with allegedly only €500m left in vaults.

China’s volatile equity rout continues after the HSBC Services PMI fell to 5-month low adding to fears of economic slowdown. While off their worst levels (-7%) Shanghai Composite still -25% from mid-June peak (tech-heavy ChiNext -40%). So much for regulator moves to stem deflation of bubble they pumped up. Now suggestions/conspiracy of institutional short selling. Short-selling ban anyone? Always worked in Europe…

Japan’s Nikkei flat with a stronger JPY (thanks to US jobs report taking USD off highs) and mixed PMI data (Services up, Composite down, despite Wednesday’s Manufacturing improvement). Australia’s ASX down as Chinese markets continue to bleed, and retail sales disappoint, and despite an improvement in Aussie Services PMI to growth and a weaker AUD.

It’s PMI Friday today with prints from Spain, Italy, France, Germany, the Eurozone (+ retail sales) and UK, all before, 10am. Speeches from the EU’s Juncker this morning (11.30am) and Merkel this afternoon (1.30pm) complete the bill for this week. Keep an eye on the live Macro-Calendar for a full rundown with expectations.

Gold bounced from fresh 3.5month lows of $1157 but remains in downtrend from mid-May. Getting back above $1165 is positive, but work to do to offset falling trend of last 4 days. Strong USD still hurting along with demand for alternative better performing safehavens.

US Crude production has indeed increased with yesterday’s Baker Hughes rig count supporting Wednesdays inventory data, posting as it did the first rise in the number of operational drilling platforms since 5 December as the price of oil stabilises around key the $60 level. Brent $62 this morning while WTI currently $56.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – it’s all part of the service.

UK Company Headlines: (Source: Reuters/DJ Newswires/Bloomberg)

- Optimal Payments' trading to end of June in line with market expectations

- Ferrexpo first – half pellet production rises 8.3 pct

- Kenmare Resources says Moma Titanium Minerals project is now working normally

- Eckoh says not to proceed with offer for Netcall

- Gulf Keystone says Non – Executive Director V Uthaya Kumar resigns