Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

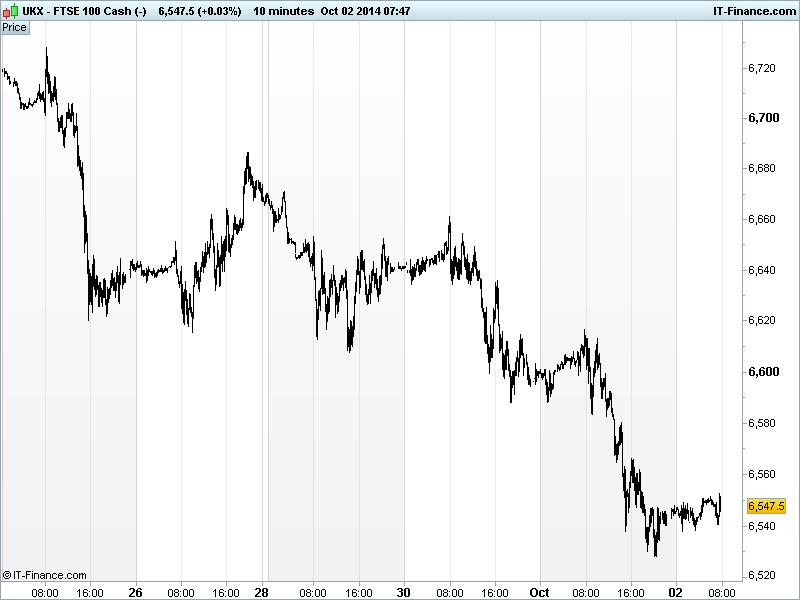

UK 100 called to open -15pts at 6545, with the index futures having made it, as discussed, as far as August’s low 6527 by the time US markets closed as risk aversion stayed in the driving seat, even pressing the accelerator on intensification of market worries before finding a smidgen of support overnight.

US stocks closed sharply lower last night, weaker than European counterparts (-1.5% vs -1.0%), weighed by poor Eurozone manufacturing data, confirmation of the first US Ebola case, speculation of a hedge fund liquidating positions and a prominent Bond player saying markets were taking for granted the ECB buying government bonds. Note the US Russell 2000 Index now down 10% from March highs – correction.

Even if US ADP Employment Change (Non-Farm Payrolls warm-up) surprised to the upside and Oil inventories fell, there was also a rekindling of worries about the US recovery after US PMI manufacturing missed the flat September flash reading, ISM Manufacturing missed forecasts and gave up ground and Construction Spending unexpectedly fell. The USD Index pulled back on speculation it had strengthened too much too fast.

Major Asian markets are in the red, taking the lead from the US with Japan’s Nikkei the standout loser due to the weaker US data and resulting weaker USD seeing the JPY strengthen and thus hinder exporters despite data showing monetary base growth and existence of extra-accommodative policy.

Australia’s ASX in negative territory (less than JP and US) despite positive macro data (trade balance, building approvals), with global worries dominating. Ongoing Pro-democracy unrest in Hong Kong is still a valid geopolitical concern with talk of protesters escalating actions. Hong Kong and China closed for holidays.

In focus today, Eurozone Producer Price Inflation (PPI) which is seen negative in August emphasising the risk of Eurozone deflation to the ECB after yesterday’s poor PMI Manufacturing prints for the region where supposed industrial powerhouse Germany actually moved into contraction (albeit only just).

In the afternoon, the main event will be the ECB policy update and President Draghi’s press conference with markets looking for more information on the central bank’s next move in terms of stimulus - likely modest given recent TLTRO launch and rates unchanged.. Later it’s back to the US to see whether ISM New York and Factory Orders can boost stateside and thus global sentiment.

The UK 100 index has fallen as far as August lows 6527, and while markets remain worried, and the imperfect bearish flagpole pattern we had identified from highs of 6900 has not quite completed, the grouping of support around 6500 dating back to mid-March may hinder any major downside. Bulls are still expecting a recovery with all the bad news out there, but the Bears are not hibernating just yet.

In commodities, Gold is up for a second having got as high as $1222 overnight thanks to risk aversion on global recovery fears and geopolitical risk, the Ebola news as well as the weaker USD. Peers Silver, platinum and palladium all climbed too. Support at $1205 with resistance around $1230.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – it’s all part of the service.

Key Overnight Macro Data: (Source: Reuters/DJ Newswires)

- JP Monetary Base Grew, but less quickly

- NZ Commodity Prices Weak, but less so

- AU Trade Balance Beat, improved

- AU Building Approvals Beat, accelerated

See Live Macro Calendar for full data line-up, incl. consensus expectations

UK Company Headlines: (Source: Reuters/DJ Newswires)

- Carillion says Q3 trading in line with board's expectations

- Electrocomponents sees an impact of about 4 mln stg on H1 operating profit

- Ted Baker posts 24 pct rise in first half profit

- SIG says refinanced 250 mln stg revolving credit facility

- Loomis wins order from Tesco in the UK

- Afren expects to resume ops at Kurdish Badra Rash oilfield by Oct end

- UK's Domino's Pizza sees sales surge continue

- Virgin Money aims to raise 150 mln stg in London IPO

- TUI Travel in line to deliver full-year profit target

- Balfour Beatty to dispose of public partnership asset for 61.5 mln pounds

- Ophir, BG Group find more gas in Tanzania

- Ryanair Holdings PLC - RYANAIR SEPT TRAFFIC GROWS 5%

- Xaar to cut staff numbers after lowering forecasts again