Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

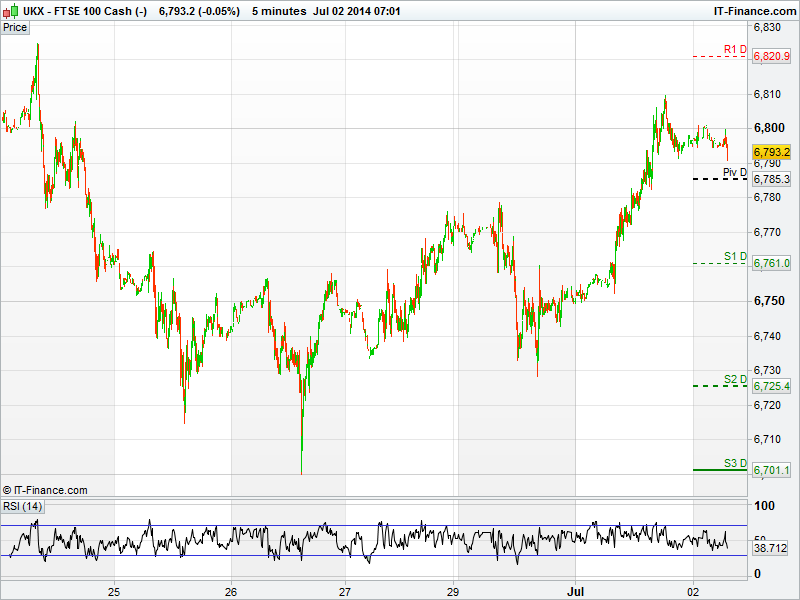

UK 100 called to open flat at 6800, after a solid session yesterday which saw the UK 100 put on 58pts and test the 6800 level again for the first time in a week.

Commodity stocks led the UK Index higher as strong Chinese PMI data reassured traders the world's second largest economy is in good shape, and a cheaper US dollar made purchasing commodities more attractive.

Anglo American (AAL.L) topped the UK Index with a 4% advance, closely followed by Rio Tinto (RIO.L) up 3%, and BHP Billiton (BLT.L) up 2.9%.

The price of gold firmed to almost $1330 on reports of escalating violence in Iraq, this ensured Fresnillo (FRES.L) up 3%, and Randgold Resources (RRS.L) up 2.2% made the top 10 performing stocks of session.

House builder stocks finished the day in positive territory as traders gambled on a positive trading update from Persimmon (PSN.L) this morning. Hopefully they'll be rewarded - as I type Persimmon's first half numbers have come in. Headlines read well - CEO cites a "strong six months" with revenues up 33% and completions up 28% year on year.

NEWS JUST IN from Nationwide Building Society - Its latest survey found that the annual rise in house prices jumped from 11.1% to 11.8% in June, with all regions across the UK seeing an increase.

The foot of the table was littered with supermarket stocks as market research company Kantar said the discount retailers where continuing to pinch market share and suggested the 'big four' need to invest in expanding and perfecting their online shopping processes.

Morrisons (MRW.L), Sainsburys (SBRY.L) and Tesco (TSCO.L) were among the 22 stocks to decline on the day.

US stocks enjoyed a memorable session. The Dow Jones recorded a level of 16,999pts, a record high. The S&P 500 also registered a record closing level of 1,973. The strong Chinese PMI data combined with better than expected manufacturing data from the US propelled US indices to new heights.

Asian equity markets followed suit to register gains across the board. The MSCI Asia Pacific Index rose to a six year high - the Australians witnessed the biggest move, the ASX200 adding 1.48%.

In focus today we have UK Construction PMI released at 9:30am, however the focal point will be US ADP data released at 13:15pm, expected to come in at 205k, a pre-cursor to Non-Farm Payrolls released tomorrow. We also have Yellen’s delivering a speech in Washington at 16:00pm. Looking at UK equities, Mothercare has rejected a takeover from Destination Maternity, Tullow Oil has written of $415M after poor drills and Blinkx has issued a profits warning.

In commodities, Gold steadied from a three-month high at $1325, as assets in the SPDR Gold Trust posted it largest two-day gain since 2011. Traders were also hesitant as Fed Chair Yellen is due to give a speech at the IMF. In industrial metals copper continued to rise to a 16-week high as manufacturing expanded at the fastest pace this year in China. WTI fell to a three-week low of $105.3 ahead of stockpile data while Brent steadied at $112.3.

In FX, the dollar traded at a six-week low versus the euro as US manufacturing data rose less than expected.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – all part of the service.

Key Overnight Macro Data: (Source: Reuters/DJ Newswires)

See Live Macro calendar for full details

UK Company Headlines: (Source: Reuters/DJ Newswires)

- Petards wins 4.5 mln stg contract with UK defence ministry

- Topps Tiles Q3 like-for-like sales up 6.3 pct, remains optimistic

- Carillion says on track to meet FY expectations

- Kier Group sees good earnings visibility in 2015

- Blinkx warns on first-half earnings, effects of disparaging blog linger

- Shelf drilling cancels London listing in challenging market

- Sirius minerals signs MoU with Tanzanian ministry of agriculture

- Purecircle expects H2 FY14 sales at $66 mln

- Salamander Energy announces spud of North Kendang-2 exploration well

- Persimmon Group's strong first half lifts revenue 33 pct

- Spirent Communications to buy Radvision's technology business unit for $25 mln

- Anite FY pretax profit falls to 15 mln stg

- Tullow Oil books $415 mln exploration write-off after poor drilling

- UK's Mothercare rejects Destination Maternity bid proposals

- Anite profit halves on weak handset-testing demand

- Premier Oil starts gas deliveries to Indonesia, Singapore