Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

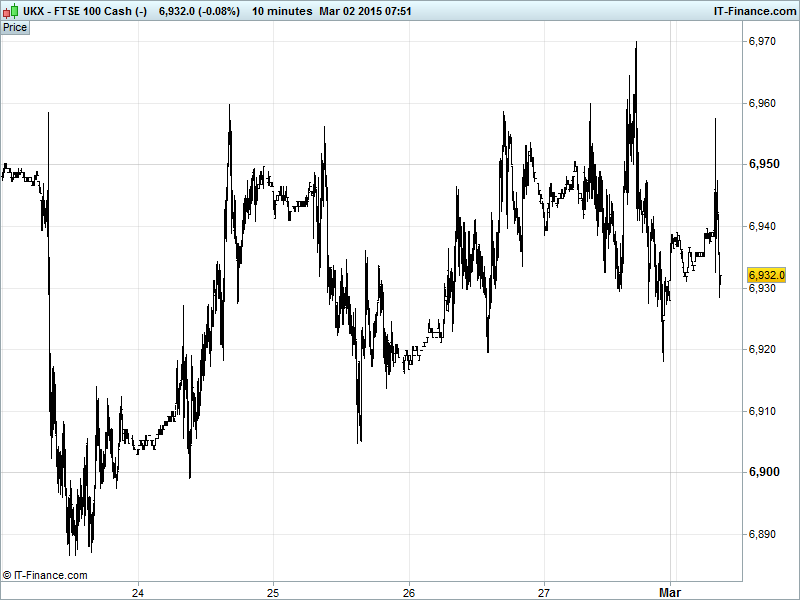

UK 100 called to open -15pts at 6930, with the February up-trend still holding strong. More interesting, however, is the 7-session trend of rising lows and recent resistance around 6960 which looks very much like a bullish ascending triangle ready to break to the upside, especially after a new all-time high of 6970 was registered on Friday. Still awaiting a decisive break into fresh all-time high territory. Watch levels: Bullish 6980, Bearish 6875.

The negative open comes despite Asian markets benefiting from news of China’s PBOC cutting interest rates at the weekend to counter deflation, widely anticipated albeit sooner than expected, demonstrating Beijing’s willingness to boost growth in the world’s #2 economy via further stimulus. The move offset China’s PMI Manufacturing contracting for a second straight month and while HSBC’s reading showed growth improving to a 7-month high, the detail suggested stimulus still required with exports shrinking and deflation hurting.

US markets closed with small losses as the month ended on a cautious note with focus shifting from Greek concerns to global monetary policy divergence with Fed talk being taken as implying a rate hike in the next few months and the ECB moving towards the start of its new QE programme in March. The Fed’s Fischer said QE success shows monetary policy can work even with rates at zero, and sees fed close to rate rise helping the USD higher. Note US caution ahead of Jobs data on Friday (Non-Farm Payrolls – NFP) and after another drop in the Baker Hughes Rig count.

Asian markets reacting positively to the China’s rate cut with Japan’s Nikkei higher boosted by a weaker JPY following last week’s USD rally offsetting slower capital expenditure spending Manufacturing PMI. Note Australia’s ASX in the green thanks to the additional stimulus move by its biggest trading partner, offsetting disappointing macro data down-under (AIG Manufacturing, Company operating profits, Commodity Index). Resilience suggesting expectation of another rate cut by the RBA too?

In focus in Europe today we have PMI Manufacturing with expectations for growth or at least improvement which along with ECB QE launch this month could boost sentiment based on fortuitous timing. Eurozone unemployment seen unchanged and CPI still in deflation. In the afternoon, US Personal Income and Spending seen offering mixed messages in terms of improvement along with US PMI and ISM Manufacturing.

US Light crude down to $49 having posted gains on Friday before the Baker Hughes rig count (down for a 12th week) halted proceedings. Brent crude fell to $62 with it widely thought that Crude prices have bottomed out and due for recovery, albeit likely volatile, this year citing growing demand in China and a shrinking excess of the commodity, although bearish wagers remain with many Hedge funds believing oil has further to fall. Note Brent maintains its February uptrend with rising support, while US Light Crude is back near $48 lows.

Gold rallied on the Chinese news but levelled off this morning with a heavy dollar basket weighing after a jump in US durable-goods orders and higher US price inflation, which makes the case for the US Fed to raise interest rates sooner rather than later. The calming of Greece-Eurogroup tensions doesn’t seem to have dented safe haven demand, which maintains a 1-week uptrend within a longer term downwards channel.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – it’s all part of the service.

Key Overnight Macro Data: (Source: Reuters/DJ Newswires)

- China Manufacturing PMI Better, Improved

- China Non-Manufacturing PMI Improved

- Aussie AIG Manufacturing Deteriorated

- Japan Capital Spending Growth slowed

- Aussie Company Operating Profits More contraction

- Japan PMI Manufacturing Improved

- China HSBC PMI Manufacturing Better, Improved

- Aussie Commodity Index Contraction accelerated

See Live Macro Calendar for full data line-up, incl. consensus expectations

UK Company Headlines: (Source: Reuters/DJ Newswires)

- Insurer Hiscox profit falls 5.5 pct as rates fall

- Gemfields posts revenue of $14.5 mln from emerald and beryl auction

- Connect group names Gary Kennedy its chairman – designate

- Alent's full – year adjusted profit rises on electronics, auto demand

- Keller says full-year adjusted pretax profit up 15 percent

- Max Petroleum suspends shares pending outcome of financing talks

- Trinity Mirror pays first dividend since 2008

- Hiscox says FY pretax profit fell to 231.1 mln stg

- Aircraft parts maker Senior's full – year profit rises