Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

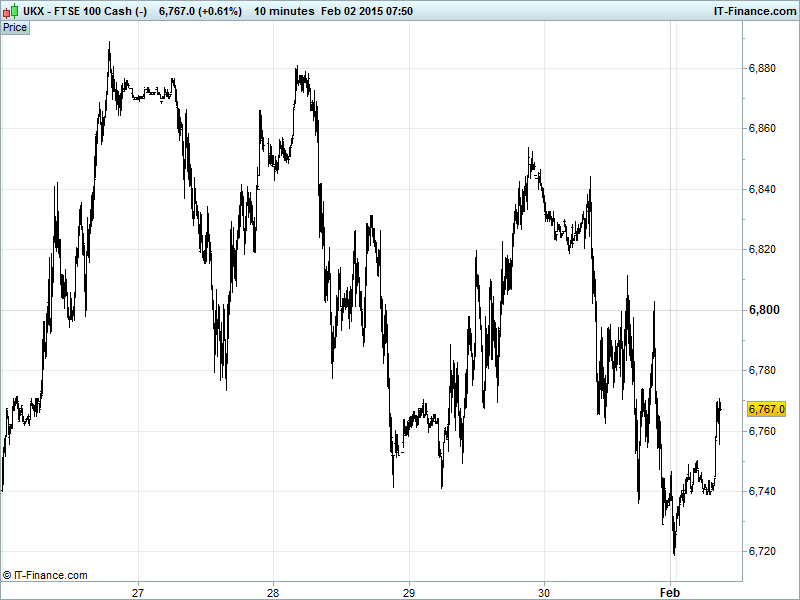

UK 100 Index called to open +5pts at 6755, having tested below 6750 support again after Friday’s close, and broken below the trendline of intersecting support dating back to 6 Jan. This adds to the trend of falling highs from mid last week and to the possibility of the index remaining under pressure into the new month. Updated Watch levels: Bullish 6820, Bearish 6705.

The positive open comes despite data from China showing the manufacturing sector falling into contraction over the weekend and a worsening in the HSBC reading this morning, although the official print for Services sector shows growth, albeit slower. Overall the data is likely to stoke hopes of a hard landing and need for additional stimulus for the world’s #2 economy.

US bourses closed lower amid choppy trading, dented by worse than expected Q4 GDP, a surge in the oil price as well as the raft of mixed corporate results throughout the week. Concerns also high about Greece refusing to cooperate with the Troika and not seeking an extension to its bailout setting itself for a cash crunch in March. Individual Fed comments in favour of a rate rise this year also hurt sentiment.

Over the weekend, data for China Manufacturing PMI disappointed with its first contraction since September 2012 although the reading for Non-Manufacturing (Services) did make a recovery back closer to growth and the official services reading remained in growth territory. This morning Japanese PMI Manufacturing showed a steady pace of expansion while the Aussie commodities price index remains understandably under pressure from the stronger USD and global growth concerns.

Asian bourses mixed after the China data with Japan’s Nikkei showing similar losses to Europe on Friday, but less than the US, weighed by US GDP slowing and mixed corporate results. Australia’s ASX positive after the improvement in its PMI Manufacturing, back closer to growth as well as hopes for more China stimulus and a rate cut by the RBA.

In focus today we have Eurozone, German and UK PMI Manufacturing which are all expected to be confirmed in growth, while France remains in contraction. In the afternoon, US Personal Income and Spending is forecast mixed, with the former slowing and the latter into contraction, adding to the concerns from slowing GDP on Friday. US PMI and ISM Manufacturing should stay solidly in growth, while Construction spending rebounds.

Gold still struggling with a falling trend from recent $1305 highs, although holding up around $1280, despite a stronger USD as investors and speculators weigh up the future of monetary policy in the US and indeed around the world. Greek concerns helping out via safehaven demand.

Oil benefited from a drop in the Baker Hughes oil rig count on Friday, offsetting some global supply glut worries and taking it well off its recent lows but US light Crude still unable to make progress above $48 while its Brent cousin tested $53. Note the stronger USD from rate rise fears still a hindrance.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – it’s all part of the service.

Key Overnight Macro Data: (Source: Reuters/DJ Newswires)

- China Manufacturing PMI Miss, deteriorated

- China Non-Manufacturing PMI Improved

- China HSBC Non-Manufacturing PMI Miss, deteriorated

- Aussie Commodity Price Index Slightly Improved

- Japan PMI manufacturing Slightly Improved

See Live Macro Calendar for full data line-up, incl. consensus expectations

UK Company Headlines: (Source: Reuters/DJ Newswires)

- Balfour Beatty joint venture signs 5-year contract with Thames Water

- Rockhopper to start 2015 Falkland drilling work in March

- CRH announces underwritten placing

- CRH says 6.5 bln eur deal makes it Europe's no.1 building materials group

- Shire says Vyvanse approved for binge eating treatment in U.S.

- EnQuest exits Tunisia after disappointing oil production outlook