Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

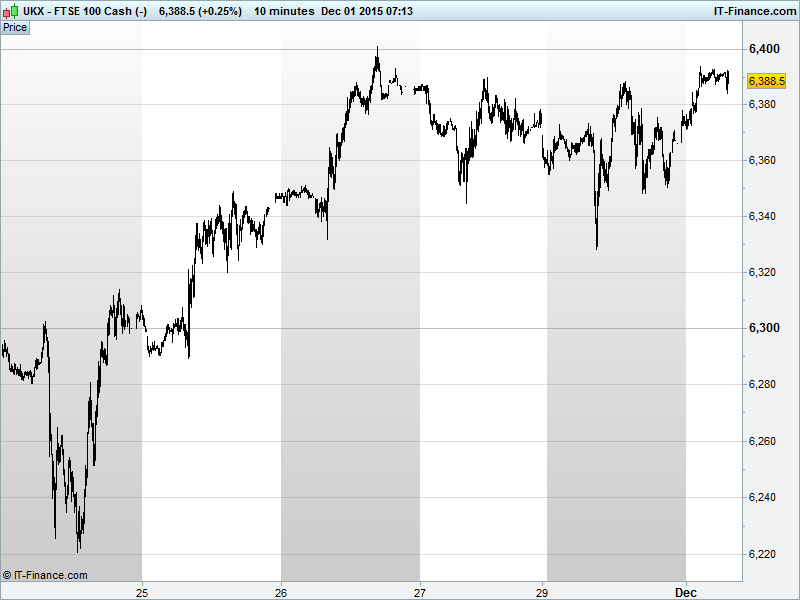

UK 100 Index called to open +30pts at 6385, having rallied off 6350 support in another attempt to better recent 6400 highs overnight. This keeps the November uptrend in motion but a decisive break above 6400 required before the otherwise dominant downtrend from October and May highs can be ignored. Further gains from the 100-day MA are positive. Watch levels: Bullish 6405, Bearish 6340.

A front foot open for equities comes after gains in Asia overnight as investors focused on the positive elements within mixed China PMI data and potential for more stimulus. While official data for Manufacturing disappointed (lowest in 3 years) the increasingly important Services saw growth improve. The Caixin private sector survey, however, showed Manufacturing contraction lessen.

A USD off its highs before a widely anticipated mid-month Fed rate hike is also helping commodities, with Copper and Oil finding support and Gold rallying to test declining 3-week resistance. Inclusion of the Chinese currency by the IMF is adding some faith in the world’s #2 economy that a hard landing is not on the cards.

In Asia, Japan’s Nikkei up for the first time in 3 days after Capital Spending data beat expectations quite considerably offsetting a stronger JPY and slight pullback in Manufacturing PMI. Australia’s ASX outperforming thanks to the commodity bounce, much better Building Approvals and Manufacturing PMI data, focus on China PMI positives as well as the RBA maintaining scope for further easing.

US markets closed negative yesterday with futures seeing somewhat of a recovery this morning. Little in the driving seat bar more talk of Fed monetary policy - now pretty much all about the path of tightening rather than ‘will they, won’t they?’ Goldman Sachs this morning repeating the ‘slow and steady’ mantra on US interest rates while expecting further easing from the ECB this week.

Divergent monetary policy is sure to keep USD buoyant while applying an almost Newtonian opposing force to commodity prices (that’s DOWNWARDS, to be clear), but the potential is always there for markets to simply move on after the Fed pushes the button. With the Dollar set to remain strong, there could be little alternative but for the basic materials sector to look at production.

The BoE UK bank stress test results suggest the central bank will ease capital pressures on the sector after years of post-crisis reform. While RBS and STAN failed aspects of the balance sheet analysis exercise, they already have plans in place to hit targets. Keep an eye on the reaction in UK bank shares this morning.

In focus today we have Eurozone and US final PMI data seen confirmed, while the UK figure is expected to show a pullback and. Elsewhere, US ISM data seen improving. After the UK Bank stress tests, BoE Governor Carney is speaking at 9am.

Oil prices are recovering after selling off yesterday afternoon - something often seen after an aggressive move but this time coinciding with a slight pullback in the USD Basket, which nonetheless remains at record high levels north of 100. Drivers remain unchanged though - oversupply, stubbornness and demand issues making for trade opportunities on near pure technicals.

Gold has recovered slightly too, now back at 5-year lows (phew!). Short covering seen to be the catalyst for the most recent up move (rather than jubilant bargain hunters going long) ahead of more important macro data from the US this Friday, which is sure to pump up an already muscular Dollar and make the yellow metal even more of a bargain.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – it’s all part of the service.

UK Company Headlines: (Source: Reuters/DJ Newswires)

- AIM says trading in Globo shares cancelled

- WH Ireland Non–exec Chairman Rupert Lowe leaves

- Shanks says to sell non-core Wallonia business

- Fitbug names Donald Stewart as chairman with immediate effect

- St. Modwen sees FY pretax profit likely in line with market expectations

- RBS says no need to alter current capital plan after UK banking 'stress test'

- Safecharge International Group CFO resigns