Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

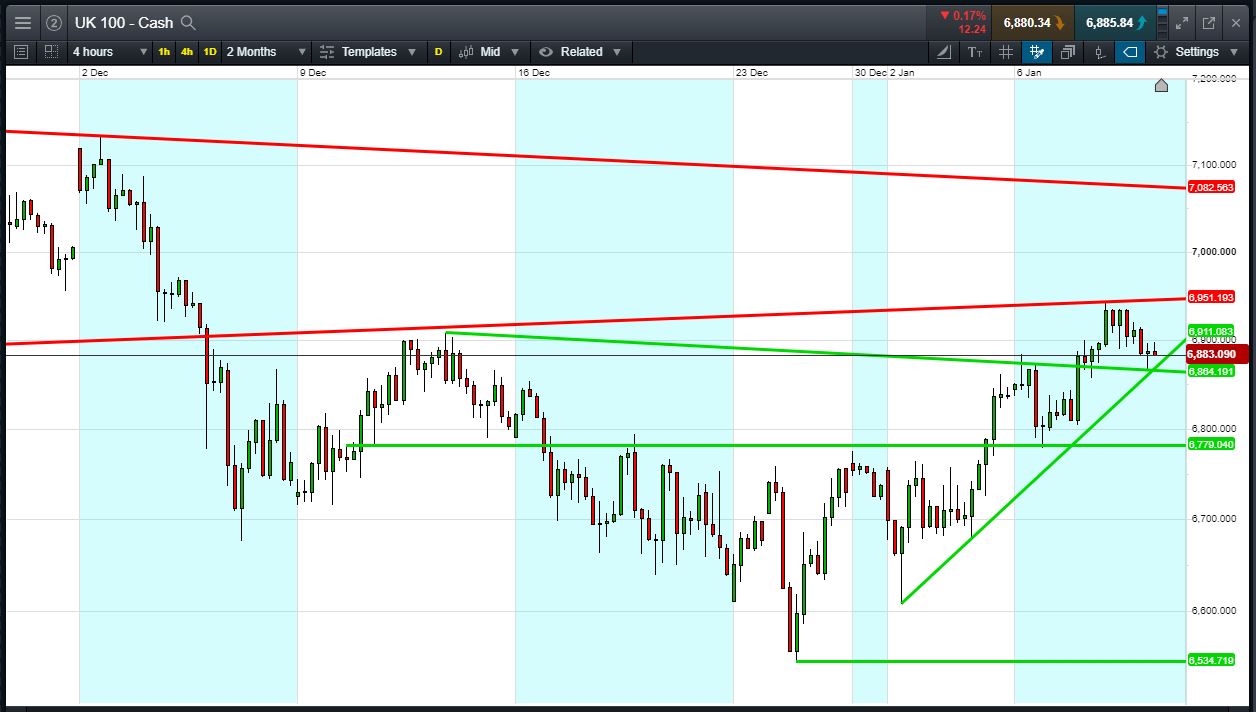

UK 100 called to open -20pts at 6885, back from overnight highs of 6900 but holding late Dec rising support. Bulls need a break above 6900 to revive the uptrend. Bears require a break below rising support at 6880, and intersecting support at 6865, to extend the retrace. Watch levels: Bullish 6900, Bearish 6865

Calls for a negative open come despite Wall St extending its longest winning streak in months. Asia more mixed after disappointing Chinese inflation added to worries about growth (although it will support expectations of more stimulus) and came hot on the heels of a US-China trade talk statement which lacked any details on a resolution of the current dispute.

Dovish Fed minutes have put pressure on the USD, with reciprocal GBP strength hampering the UK Index . Miserable UK BRC Retail Sales numbers may also heighten UK Index Retailer worries, after contracting -0.7% YoY in December for the worst Christmas snapshot in a decade.

Oil prices are retreating from overnight highs, though Brent is still above $60, after a strong Wednesday rally as Saudi Arabia pledged to “stabilise” the oil market and speculation swirled that they were targeting $80/barrel oil price (more OPEC/non-OPEC cuts in the air?).

In corporate news this morning Marks & Spencer Q3 Group Sales -3.9% YoY; UK -2.7% (-2.2% like-for-like), Int -15.1% (-1.4% ex-HK sale); Clothing & Home -4.8% misses -4.6%e (online +14%), -2.4% like-for-like misses 1.7% est; Food -1.2% (-2.1% like-for-like beats -2.5%e); Steady in difficult markets; transformation on-track; Guidance unchanged,

Tesco 19-week (Q3+Christmas) like-for-like sales +0.8% YoY (Q3: +0.5%, much slower than Q2 and Q1; Christmas +1.5%). UK +1.2%, outperforming market in all key categories over Christmas (+2.2%), but Central Europe and Asia weaker. Ireland flat after tough comparable. Booker Q3 strong (+11%), but slowed over Christmas (+6.7%). FY guidance unchanged.

Mitchells & Butlers Q1 like-for-like sales +4.7% YoY (3 week festive: +9.8%; Core Christmas fortnight +12.3%), evenly spread over Food and Drink. Enters “toughest quarter” and expects “quiet” trade until next payday.

Debenhams like-for-like 6-week Christmas sales -3.4% (online +6%); 18wk sales -5.7% like-for-like; warns H1 margins to be eroded by discounting; continues to generate cash; reiterates FY guidance; in talks with lenders about refinancing; further asset sales on hold.

B&M European Value Retail Q3 like-for-like sales +12.1% YoY, with growth in Germany and France, but UK -1.6% after a tough comparable (+3.9% last year). Gross margin held back in Nov, but improved in Dec. FY guidance unchanged after January trading started well.

Prudential extends strategic bancassurance alliance in Asia with United Overseas Bank to 2034. DNO claims 72.8% stake/acceptances for Faroe Petroleum takeover.

Card Factory 11-month like-for-like sales flat YTD, opened 51 net new UK stores. FY EBITDA £89-91m (broadly flat) guidance unchanged, but anticipates 2020 to be another difficult year. Expects £5-6m additional costs from higher National Living Wage and electricity wholesale prices.

Premier Oil expects year-end net debt below guidance; full year production expected +7% after Nov-Dec rates average above forecast (as communicated 7 Dec); strong production base, well hedged, prioritising debt reduction.

Halfords blames mild weather and weak consumer confidence; cuts FY19 pre-tax profit guidance to £58-62m; Q3 group revenues -1.7% like-for-like (YTD +1.0%); Retail -2.2% (+0.7%), Motoring -3.4% (+0.9%), Cycling -0.3% (+0.5%), Autocentres +1.4% (+2.6%); expects weak consumer confidence into FY20, profits flat on revised FY19 guidance. Confident in cash flow for divs.

Hilton Food FY trading in-line, strong sales growth driven by Seachill and Australian operations. UK/Ireland turnover higher. Outlook positive.

In focus today will be digestion of yesterday’s US-China trade negotiations (brief statement merely highlighting topics covered), disappointing China inflation which vindicates Beijing’s fresh stimulus to counter slowing growth, as well as dovish Fed Minutes.

For the rest of the day, much of the attention will be on the Fed Chair Powell (5:45pm), who participates in a discussion at the Economic Club of Washington. Following very dovish FOMC meeting minutes, highlighting “patience” with regards to further interest rate hikes, amidst financial market volatility, traders will be looking for further elaboration on the Fed’s policy path for 2019.

Elsewhere, ECB Dec meeting minutes (12:30pm) will be scrutinised for monetary policy hints. Especially with QE having ended on 31 Dec with growth and inflation still slowing.

In terms of speakers, we have several more Fed officials (we had a trio yesterday), including Barkin (1:35pm, voter, centrist), Bullard (5:30pm, non-voter, dovish) and Evans (6pm, non-voter, hawkish), all speaking on US economic outlook and monetary policy.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – it’s all part of the service.