Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

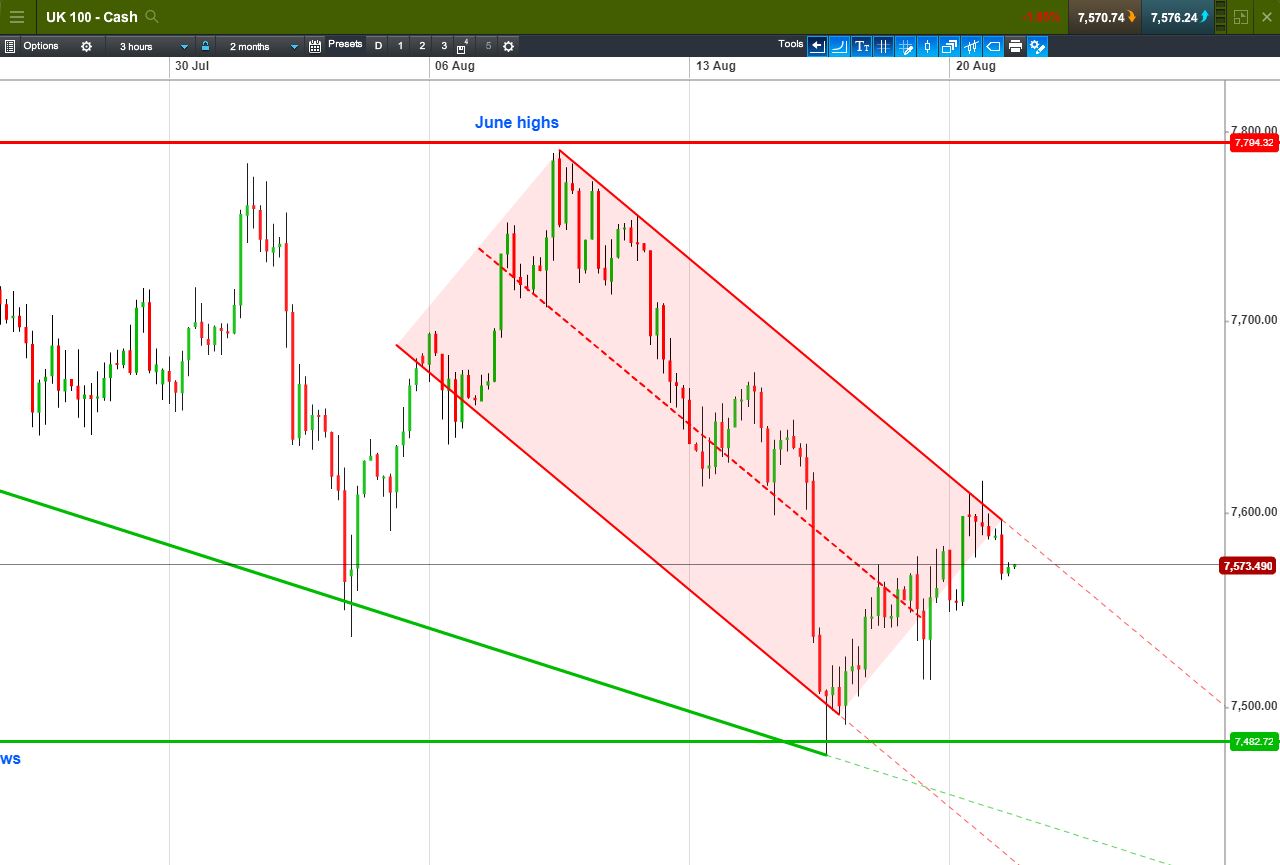

UK 100 Index called to open -18pts at 7573, slowing down its week-long uptrend and still maintaining the 3-week falling channel. Bulls need a break above 7600 overnight highs for another test of channel ceiling. Bears require a breach 7550 Monday’s lows. Watch levels: Bullish 7617, Bearish 7535

Calls for a negative open come in spite of upbeat trading on Wall St and in Asia, where markets were hopeful for an easing in Sino-US trade tensions, and after China’s banking regulator called for local banks to increase infrastructure lending amid a slight pullback of Chinese economy.

Most of the UK Index negativity is generated by USD losses after President Trump criticised the Fed Chair Powell’s interest-rate hiking policy in an interview with Reuters. The Fed is independent in setting monetary policy and markets were spooked by yet another comment from Donald Trump criticising higher interest rates (his property magnate background seeping through?).

GBP strength this morning is pressuring the UK Index , though there is silver lining to this cloud, as the corresponding Greenback weakness is proving beneficial to USD-denominated commodities, as oil, copper and gold prices are higher this morning. That said, dual-listed Miners are lower in Australia overnight on the back of BHP Billiton results missing expectations.

In corporate news this morning BHP Billiton FY net profit -37% YoY due to $5.2bn one-time impairment charges (sale of US assets to BP and Samarco dam failure), with results missing expectations. Net cash flow +10%, dividend +42%, average commodity prices helping revenues (oil +26%, copper +23%, coal +9%, iron -3%). Reiterates plans to use proceeds from asset sales for dividends or share buyback when completed.

Persimmon H1 group revenue +5% YoY, pre-tax profit +13% YoY, new home sales +4%, average home selling price +1%, forward sales are 6% ahead of last year. Housing market conditions are still supportive and company expects cash generation to remain strong.

AstraZeneca announced that lung cancer drug Tagrisso has been approved for initial patient treatment in Japan. Polymetal H1 revenue +16% YoY, adj. EBITDA +19%, avg. gold price +6%, avg. silver price -4%, net earnings +46%, net debt +16%, dividend +67%. Remains on track to meet FY production and cost guidance, contingent on RUB/USD FX rate (which impacts operating costs).

John Wood Group H1 total revenue +13.4% YoY, EBITA -1.5% (upper end of guidance range), earnings margin -80bps, interim dividend +2%. Expects to deliver >$50m in FY cost synergies from integration. Confident in stronger H2 due to revenue visibility, cost synergies. FY outlook unchanged.

In focus today, on yet another macro-light day, will be UK’s public finances, with Public Sector Net Borrowing (9:30am) forecast to decline in July and register a £2.2bn surplus after 3 months of borrowing deficits. Meanwhile, CBI Industrial Trend Order Balance (11am) is expected to further decline by 2 points.

In the evening, oil market watchers will be following API Oil Inventories (9:30pm). After an unexpected large build-up in official government stocks last week sent oil prices and UK Index Energy shares lower, markets are paying ever closer attention to inventory numbers. Economists are currently forecasting oil inventories in the US to remain unchanged.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – it’s all part of the service.