Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

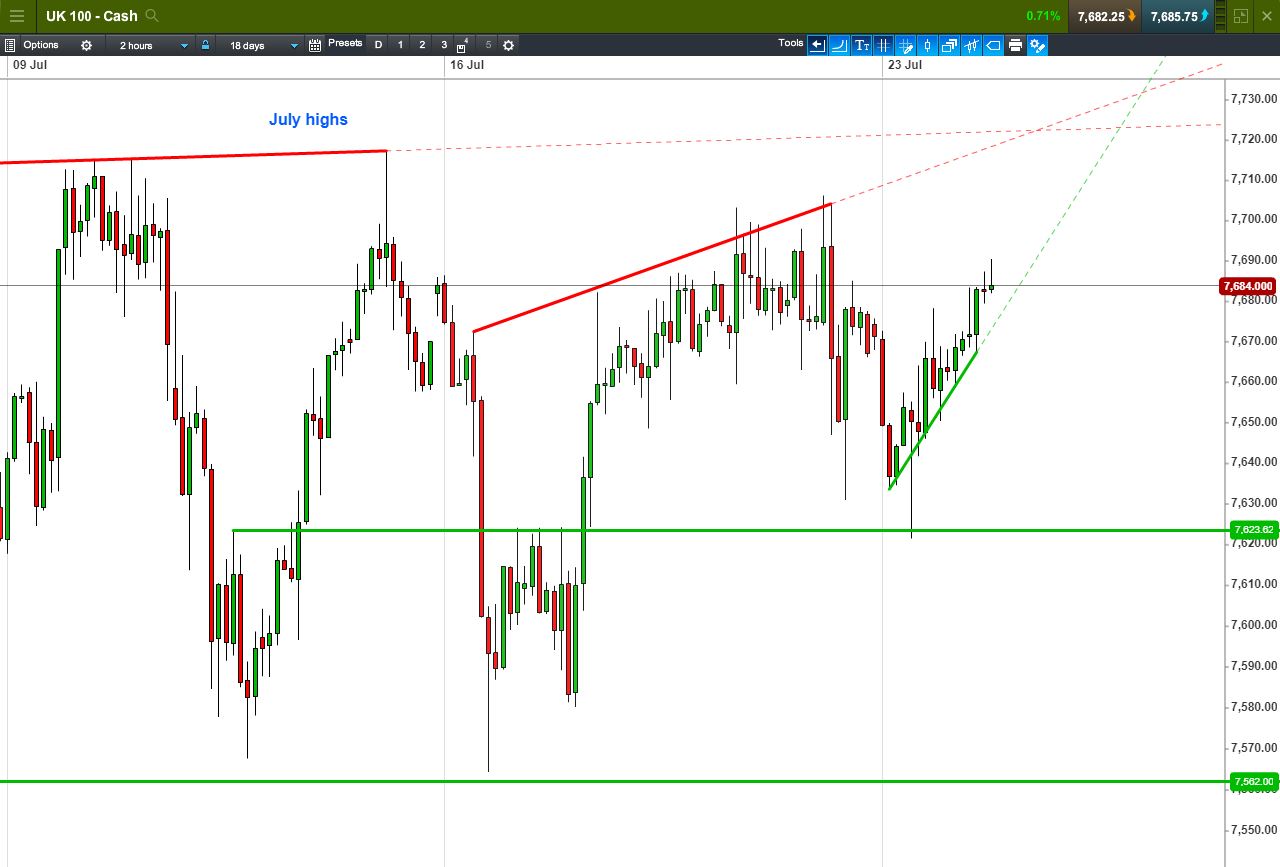

UK 100 Index called to open +30pts at 7685, extending yesterday’s rebound towards Friday’s 7708 highs and July’s 7718 peak. Bulls need a break above 7690 while Bears likely require a breach of 7670. Watch levels: Bullish 7690, Bearish 7670

Calls for a positive open come after Asia extended Wall St gains. Surging government bond yields (US, Japan), supported by Fed monetary policy tightening and BoJ tweaking are boosting Banks & Financials, while expectations of an upcoming meeting between US President Trump and European Commission President Juncker is smoothing some of the trade war concerns. That said, China (and its currency) remains under pressure.

Expectations of a strong Fed rate-hiking pace and US Treasury Secretary Mnuchin’s confirmation that the White House will respect Fed independence, is boosting USD versus peer currencies, with corresponding GBP weakness flattering the UK Index ’s many internationally-exposed contributors.

Oil prices are lower on concerns of increased global crude supply (extra volume from Libya and Saudi Arabia), while the Trump-Iran war of words is yet to produce a tangible follow-through (merely a distraction from Russia?) to move energy markets. Gold is lower, extending a 3-month downtrend, amid USD strength and lack of demand for safe-havens.

Corporate news this morning Sky News reports that Tesco may be set to challenge German discounters Aldi and Lidl with a new retail format called Jack’s. Banks may be sensitive to UBS Q2 pre-tax profit +12% (adj. +8%), beating forecasts, thanks to investment banking strength (equities, fixed income) and despite weakness in net interest income and wealth management outflows.

BT says Openreach will deliver supplementary wholesale broadband discounts (in return for volume commitments) to incentivise UK upgrade of broadband network over next 3 to 5 years. Britvic Q3 revenues +3.4% YoY (-0.6% excl. soft drink levy), UK +1.9% ex levy (carbonated -2.9%); International +8.7% (IRE +6.6% ex SDIL, FR -15% due to weather); reiterates FY expectations.

Hammerson H1 net rental income -3%, adj. profit +0.5%, div +3.7%; launches £300m buyback; new disposal target of £1.1bn by end-2019 (£300m completed; 2018 target raised to £600m), plans to exit retail parks over medium term. Ashtead increases planned debt issue for refinancing to $600m.

ConvaTec gets US FDA clearance for AQUACEL Ag Advantage dressing for wound management. PZ Cussons FY revenues -2.3% YoY like-for-like, adj. op profit -15.9% due to poor performance in Nigeria, dividend unchanged; expects another challenging in most markets with costs & FX volatile.

Superdry co-founder sells 6.7% stake for £71m. Drax H1 EBITDA -15.7% YoY after unplanned outages, operating cash flow -43%, dividends +14.3%. Spectris adj. sales +5% like-for-like, op profit +15%, dividend +8%; continues to expect growth to ease a little in H2; FY expectations unchanged. Astrazeneca sells EU commercial rights for Atacand for $200m, no impact to 2018 guidance.

IG full year net trading revenue +16%, op. profit +32%, dividend +34%; expects to freeze pay-out level while it adapts to new regulations; expects FY19 revenues lower but costs flat after regulatory changes in UK and EU, before returning to growth in FY20. IQE FY guidance unchanged; wireless business unit renews major contract with tier 1 customer.

In focus today will be preliminary July Manufacturing & Services PMI figures from France, Germany and the Eurozone (8-9am). While all are expected to keep above the key 50 level separating expansion from contraction all are expected to have given up a little ground since June. Watch the EUR and European shares/equity indices for potential moves.

Across the pond, preliminary July US PMIs (2:45pm) are projected unchanged for both Manufacturing and Services, holding their slowest pace of growth in 4 months. Watch USD and stateside shares/equity markets.

This evening, weekly API Oil Inventories (9:30pm) could move crude oil prices with analysts expecting the report to show another drawdown, reversing the small uptick last week which bucked a six week trend of declines. Keep an eye on oil prices and energy-sensitive equities.

In terms of speakers, UK Brexit secretary Dominic Raab is expected to deliver a statement (2pm) in the House of Commons (a day before the summer Parliament recess) outlining the government’s white paper for implementation of the EU Withdrawal Bill.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – it’s all part of the service.