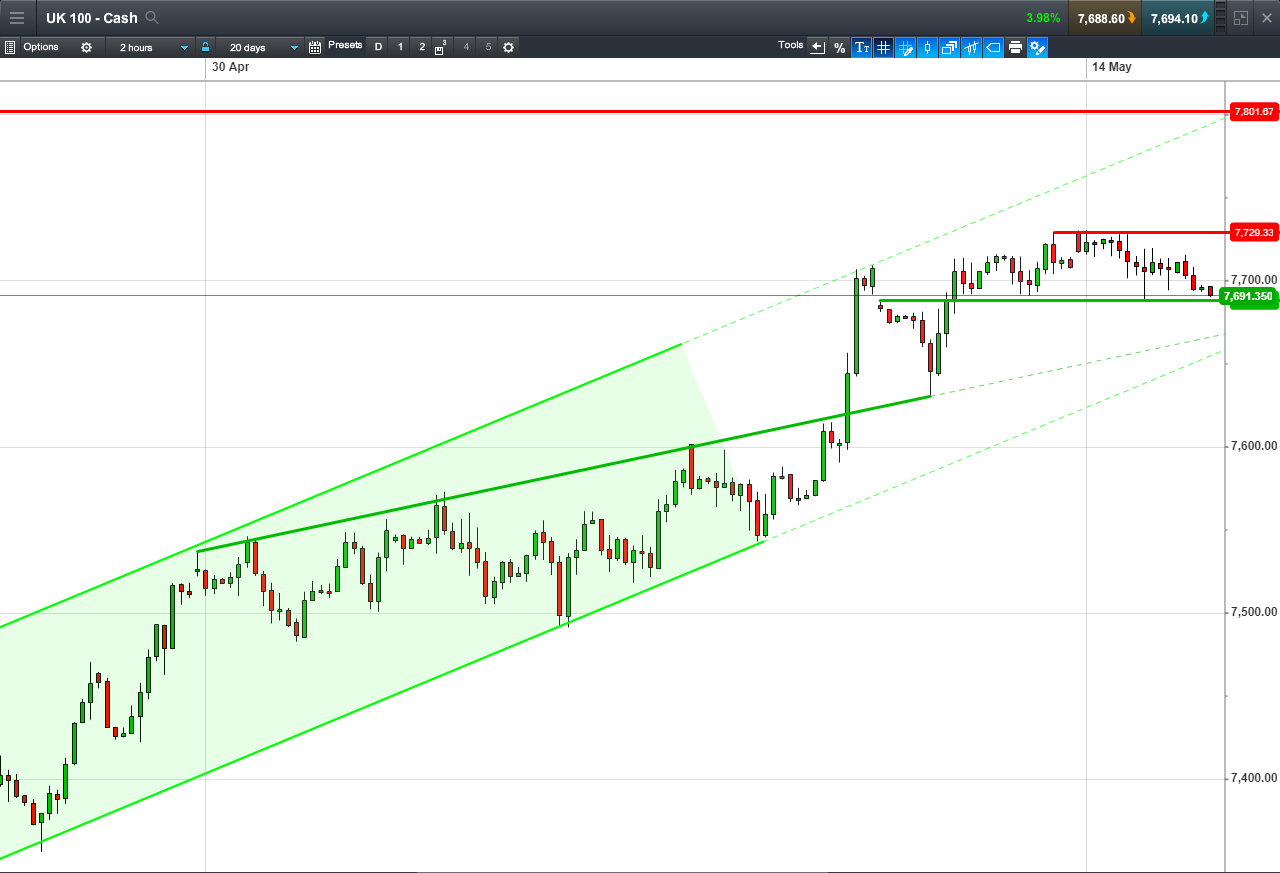

UK 100 Index called to open -20pts at 7690, back around yesterday’s lows but holding its 7-week up-channel, keeping 7800 Jan highs within sight. Bulls need a break above falling highs at for another attempt to crack 7730. Bears require a breach of 7690 for a retest of the 7660 channel floor. Watch levels: Bullish 7710, Bearish 7690

Calls for a negative open are supported by losses in Asian overnight and in spite of small gains on Wall St (Energy and Healthcare leading the way), perhaps spooked by mixed China data overnight (Retail Sales and Fixed Asset Inv. growth slow more than expected, Industrial Production accelerates more) which could have read-across for UK Index Miners.

Supply concerns continue to keep oil prices around 3.5yr highs, supporting Energy names. Fresh USD strength (treasury yields >3%) is keeping Gold and Copper under pressure, offsetting the corresponding benefit of GBP weakness for UK Index Miners, even if it assist other internationally exposed names.

Middle East tensions (Iran/Israel/Jerusalem) and Sino-US trade negotiations have provided mixed signals, the White House promising conciliation vis-a-vis China’s ZTE Telecom fate, then indicating that some form of punishment is still in the cards.

In corporate news this morning, UK bookmakers may react further to news late yesterday that the US Supreme Court has struck down a federal ban on lucrative sports betting. Vodafone revenues -2.2%, operating profit +15.4%, back to net profit, free cash flow +22%, net debt +1%, dividend +2%; expect to sustain our profit growth.

Hargreaves Lansdown AUM +3.1% in 4M to April 30, net new business +£3.3bn, clients +60K, net revs +15%. Land Securities FY revenues +6.3%, pre-tax loss £251m, NAV -2.7%, dividend +14.7%, “navigating uncertain waters in near term”, Cressida Hogg appointed non-exec Chair.

easyJet FY total rev per seat +10.9% (8.3% at constant FX), cost per seat +2.2%, passengers +8.8% on capacity +7.8%, back to pre-tax profit (ex=Tegel acquisition), headline loss narrows. CYBG H1 underlying pre-tax profit +28% (net loss), £350m extra provision for PPI, Net interest margin falls, UK operating environment remains challenging

Taylor Wimpey new strategy and updates goals; enhanced ordinary dividend, 7.5% of net assets, up from 5%, >£250m/year up from £150m; special div £350m increases total div by 20%.

DCC Revenues +12.6%, adj. Op. profit +11.1%, EPS +10.8%, Div +10%, Free cash flow -21%; Expects another year of profit growth and development. The CMA is investigating if the Lonmin/Sibanye tie-up will hit competition for platinum in the UK. Cairn Energy CEO confident of position in India Tax Dispute.

In focus today will be UK Wages growth (9.30am), for its inflationary read-across and potential influence on market expectations for the Bank of England’s next interest rate rise. Strong wage growth could push GBP higher, hurting the UK Index , the reverse being true if wage growth slows.

The second estimate for Eurozone Q1 GDP (10am) is expected to, again, show slower growth in Q1 versus Q4. This could keep pressure on the Euro although a rebound in March Industrial Production (despite the cold weather) could help offset any negative reaction.

This afternoon, US Retail Sales (1.30pm) are forecast mixed (slower headline, faster core), adding to the fun and games of interpreting consumer confidence and US inflation, but unlikely to deliver anything that sway the Fed from another pending rate hike. Other signals could come from the US Housing Index (3pm; expected flat ) and Q1 results from Home Depot (2pm).

Speakers today include the Fed’s Kaplan (1pm) and Williams (6pm), with Trump’s nominees Clarida and Bowman sandwiched in between. The two will be testifying to the Senate Panel, their answers having potential to alter expectations on the balance of voting intentions.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – it’s all part of the service.