Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

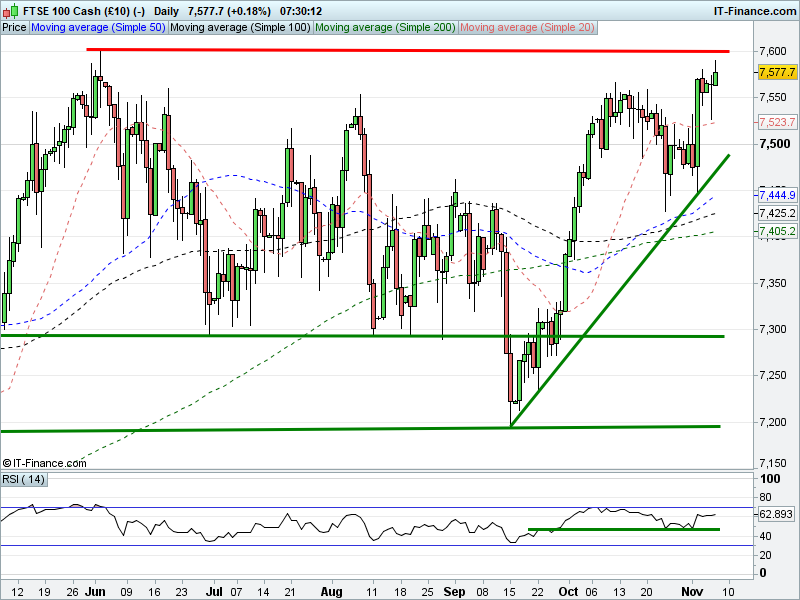

UK 100 Index called to open +15pts at 7575, back from an overnight foray as high as 7590, within touching distance of June 2’s 7598 intra-day record high. Bulls will be looking for 7573 to hold up (yesterday afternoon’s high, Monday rising support) to keep the new rising channel alive towards a fresh record. Bears need for 7575 to give way for a retrace towards 7525 or lower. Watch levels: Bullish 7580, Bearish 7570.

Calls for a positive start stem from another positive close on Wall St, with more record highs to boot, and gains across the board for major Asian bourses overnight. The energy sector benefits from further gains for Oil amid Saudi geopolitical uncertainty, likely to help the UK Index given the Oil majors’ heavy weighting (13%). Miners were also higher in Australia after China drove metals prices higher, something that could also help the UK Index .

Corporate news: Direct Line Insurance sees trading in-line with views, but warns of possible impairment charge. Imperial Brands constant FX results impacted by increased Investment and tough trading; targets revenue and EPS growth within medium-term guidance. AB Foods retail expansion to continue, margins in-line, but Sugar impacted by lower EU prices; dividend +12%.

G4S: 9M trading in line. Org rev growth 4.4%, all regions growing ex ME & India; expects FY organic revs +3-4% & good profit growth. DCC LPG makes first acquisition in large US LPG for £150m. UK retailers may see an impact from overnight BRC data suggesting a weak October, especially in non-Food which posted its weakest growth in five years.

US equity markets started the week as they left off, with all three major indices closing at fresh record highs as a spate of proposed M&A deals lifted stocks. Once more, the Tech-focused Nasdaq outperformed peers as investors digest the Broadcom/Qualcomm merger talks, while the reporting of a potential Disney/21st Century Fox led to the former helping the Dow Jones while the latter limbed 10%, aiding the S&P 500.

Crude Oil benchmarks eked out fresh 2-year highs yesterday evening as investors reacted to the Saudi Arabian corruption arrests over the weekend, although have retreated from their highest levels. Brent Crude rocketed through the $64 mark, reaching a high of $64.45 before falling back to the round mark, while US Crude has remained above $57 a barrel after trading overnight highs of $57.6.

Gold has trended lower overnight having rallied sharply yesterday evening on rising tensions in the Middle East and the Korean Peninsula. After reaching a high of $1283 yesterday evening, the precious metal has since fallen back below the $1280 mark as the US dollar gains in early European trading. Traders will be keeping an eye on Donald Trump’s visit to Seoul today for any provocation against the unpredictable North Korean state.

In focus today will be a pair of speeches from outgoing Fed Chair Janet Yellen. The head of the world’s largest central bank, having not been nominated to a second term by the President in a clear break with tradition, will now be scrutinised by markets for the state in which she is leaving the Fed for the incoming Chair Jay Powell. After finally reversing some of the accommodative policy enacted in the immediate aftermath of the financial crisis, Yellen has left Powell the keys in a much more attractive position than when she took over. Will she provide some words of wisdom for him this afternoon?

Datawise, UK Halifax House Prices (8:30am) are expected to slow in October however accelerate on a yearly basis, Eurozone Retail Sales (10am) are seen returning to growth in September after two months of contraction, US IBD/TIPP Economic Optimism is expected to rebound to around its 1-year average after a disappointing October and JOLTS Job Openings (3pm) attempt to return to 6.1m.

Other speakers today include the first major address from new Fed Governor Randall Quarles (5:35pm), speaking at a clearing house conference, the BoE’s Taylor (6:30pm) speaks at the Institute of International Monetary Research and BoC Governor Poloz (7pm) discusses central banks’ ability to understand inflation.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – it’s all part of the service.