Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

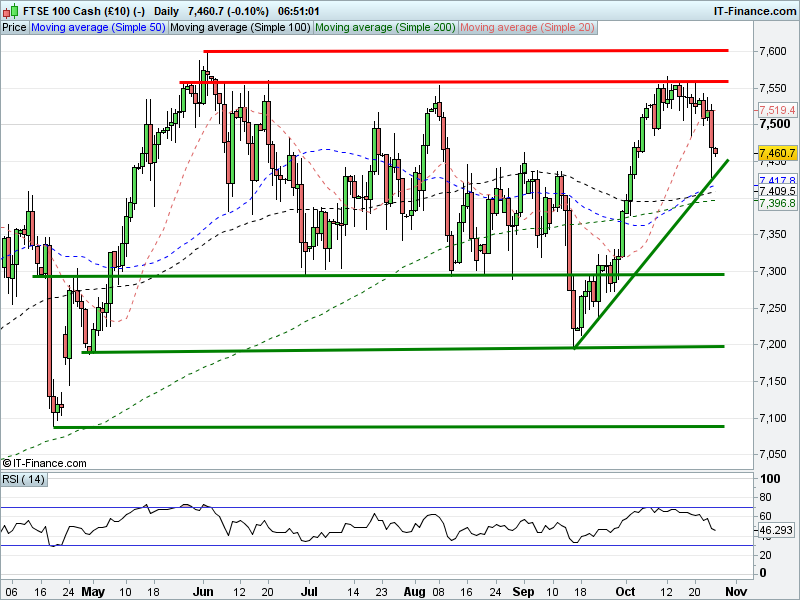

UK 100 Index called to open +10pts at 7455 thanks to a strong bounce from a weak European close (7425 lows; Sept rising support), albeit having eased back from overnight highs of 7470. Bulls need 7470 overnight highs to be bettered for another leg higher. Bears need a break back below 7450 if they want to retest rising support. Watch levels: Bullish 7470, Bearish 7450.

Calls for a positive open come in spite of losses on Wall St that have inspired a mixed session in Asia overnight, driven by disappointing earnings from across the pond, questions mount about the validity of Trump’s tax plan, and perhaps some hesitation ahead of the ECB policy update this afternoon.

Japan’s Nikkei is positive, but held back by a dollar retreat sending the Yen higher. Australia’s ASX is up to a similar degree despite Telecoms and Materials giving up ground, and while airline Qantas fell up to 7% (expected tougher conditions) it has recovered to -1.5%. Hong Kong’s Hang Seng is negative as IT and consumer discretionary slid as China’s Communist Party gathering closed.

In corporate news; Barclays Q3 pre-tax profits look to have missed consensus while other metrics are also light. KAZ Minerals has reported Copper production +14% and increased FY guidance. Debenhams has reported group profits -17% and says the environment remains uncertain. RELX announces 9-month underlying revenues +2% and an unchanged customer environment.

US equity markets closed sharply lower on Wednesday as a batch of disappointing Q3 earnings dampened sentiment. The Dow Jones suffered its largest one day drop since early September as Boeing weighed on the index, the S&P 500 saw Telecoms and Industrials underperform, while Chipotle fell 14.6%, and the Nasdaq dropped 0.5%.

Crude Oil prices are trading close to 1-month highs overnight as investors weigh the possibility of an extension to OPEC-led production cuts. Global benchmark Brent crude remains within touching distance of yesterday’s EIA-inspired highs of $58.75, with its price diverging from its US counterpart which is holding above $52 despite trending lower overnight.

Gold has trended higher overnight as the US dollar retreats, touching an overnight high of $1282.5, to test 2-week falling highs resistance. The precious metal will likely be influenced by the ECB’s monetary policy update later today as the central bank is expected to announce a sharp reduction is its QE asset purchasing.

In focus today will the ECB monetary policy update (12:45pm) and subsequent press conference from President Mario Draghi (1:30pm). Economists expect the European Central Bank’s to announce a reduction in QE asset purchases from €60bn to €30bn/month (€20-40bn consensus), whilst extending the programme by a further 6 months.

Draghi has, however, previously indicated an openness to even lengthier extensions which would allow for an even bigger QE taper to maintain a similar level of accommodative stance, something alluded to as more dovish than a simple cut with no extension. Will he once again surprise consensus or will the governing council stick to consensus? The Euro, DAX and Gold will all likely be on the receiving end of traders’ reactions.

In terms of data, UK CBI Sales (11am) are seen retreating significantly in October, US Wholesale Inventories (1:30pm) look to build on August’s 9-month high, US Pending Home Sales (3pm) are expected to swing to growth in September (New Home Sales were very strong yesterday) and the Kansas City Fed Manufacturing Index (4pm) looks to replicate Tuesday’s US Manufacturing PMI beat.

Microsoft is the lone Dow Jones component (2.3% weighting) reporting today after US market close, however a host of notable bellwethers for US industry report throughout the day. These include American Airlines, Ford and UPS before the market open and tech trio Amazon, Alphabet (Google) and Expedia all after the close.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – it’s all part of the service.