Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

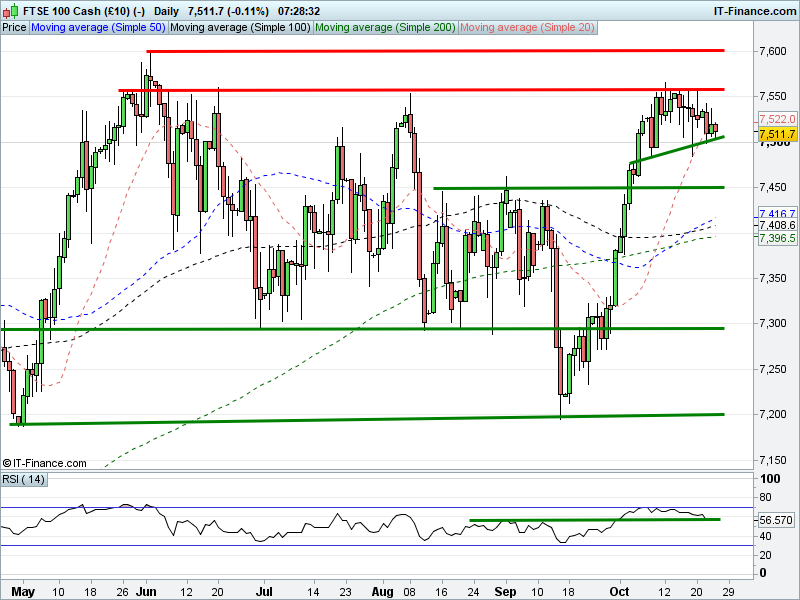

UK 100 Index called to open -15pts at 7510 after easing further from yesterday’s highs, to maintain the trend of falling highs since Friday, but stopping short of testing round number 7500. Bulls need a break above falling highs resistance at 7530. Bears will be hoping for a test of support at 7500. Watch levels: Bullish 7530, Bearish 7500.

Calls for a negative open come a mixed session for Asia overshadowed yet another positive close and more records on Wall St fuelled by another hitherto supportive earnings season from the other side of Atlantic. European sentiment may also be more hesitant as we approach tomorrow’s ECB policy update, unsure as to what Draghi will say about QE (big cut and stop sooner, or small cut and prolong?),

Japan’s Nikkei underperforms, breaking its winning run as a result of the US dollar coming off its highs to send the Yen higher. Chinese stocks outperform amid hopes of Xi Jinping staying in power for another decade. Australia’s ASX shows small gains, helped by materials and Energy, although both oil and metals prices are now off their highs.

In corporate news; Lloyds Banking 9M profits +50% YoY, no new PPI provisions, improved 2017 financial targets, but loan impairments almost doubled. Antofagasta 3Q Copper Production +3% QoQ, net cash costs below guidance, reiterates FY views. Fresnillo Q3 silver production +24% YoY, gold +6.1%, backs 2017 views. British American Tobacco expects 6.5% FX tailwind for profits.

Faroe Petroleum started drilling on Tambar development project in the producing Tambar field in Norway (Faroe owns 45%). Victoria Oil & Gas confirms $20-29m fundraising. Metro Bank customers +33% YoY, deposits +10%, lending +11%, profits +77%, CFO to retire in 2018.

US equity markets returned to winning ways yesterday as earnings propelled the Dow Jones to a fresh record closing high. Strong Q3 results from 3M and Caterpillar lifted the 30-stock index 0.7% higher, with the former contributing over half of total gains. Meanwhile, both the S&P 500 and Nasdaq climbed by 0.2%, with the S&P Financial sector climbing to its highest level in 10 years.

Crude Oil prices are trading higher this morning after Saudi Arabia pledged to end the global oil glut late yesterday afternoon. Brent and US crude, having climbed to a 4-week and a 1-week high respectively, have since retreated on profit taking and after API reported a 500k barrel build in US inventories last week against expectations of a 2.5m barrel draw. This afternoon’s EIA inventories will therefore be closely watched oil traders.

Gold has continued to retreat from falling highs resistance around $1281 as investors await crucial central bank updates. Expectations that the ECB will reduce the amount of bond purchases it undertakes to €30bn from €60bn have dampened demand for the non-yielding safe haven asset. The policy update and subsequent presser from ECB chief Draghi are likely to drive sentiment for the precious metal today.

Data today comprises UK Q3 preliminary GDP (9.30am; same growth as Q2), German IFO (10am; unchanged) and US Durable Goods (1:30pm; slower headline growth, solid ex-transport), US House Prices (2pm; growth accelerated) and US New Home Sales (3pm; a touch fewer than prior month).

This afternoon’s EIA Oil inventories (3.30pm) may excite after last night’s API report highlighted a 500K Crude build but significant 5m drawdowns for both Gasoline and Distillates. Analysts polled by S&P Global Platts expect EIA to show a 425,000 barrel drop for crude and declines of cira 2m for gasoline and distillates. After a 1m barrel production increase last week, this metric could have more impact than inventory levels themselves.

Having been a starkly Brexit-free week so far, Brexit minister David Davis (9.15am) will provide an update on proceedings at 9:15am amidst claims from both Europeans and Tory rebels accusing him of stalling. Finally, Dow components reporting before the US open today include Boeing, Coca-Cola and Visa, carrying a total weight of just over 9%.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – it’s all part of the service.