Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)!

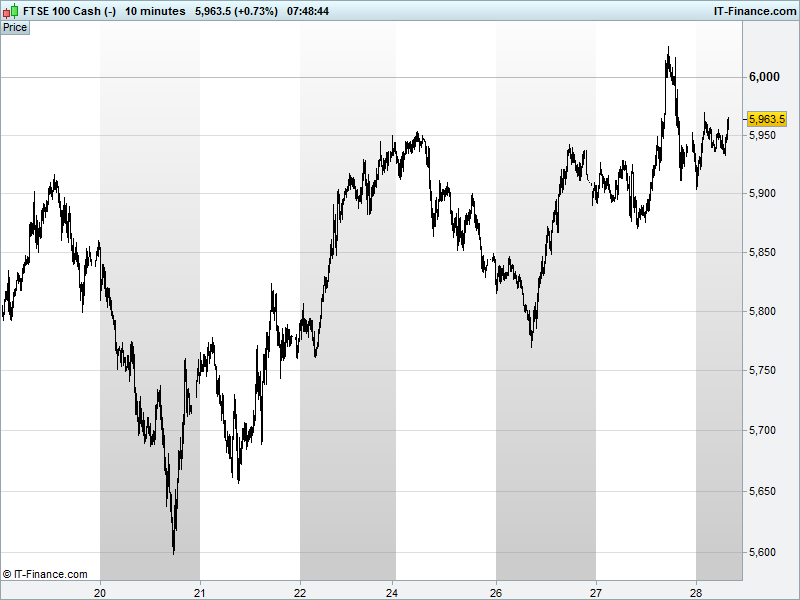

UK 100 Index called to open -25pts at 5965 having backtracked from last night’s test above 6000 which completed our bullish flag pattern. The index’s rising lows keep it in recovery mode from recent 5600 lows with potential for further gains should 5900 hold up and serve as a springboard for the complex inverse Head & Shoulders reversal to 6300 recently discussed. However, long-term downtrend intact with falling resistance at 6200. Bullish 5980, Bearish 5920.

The negative opening call comes after Asian equities followed US counterparts lower, although to a lesser degree, after the US Fed flagged risks to the US economy from financial market turmoil and despite indicating future rate rises will be gradual. Not as explicit a mea culpa as we hoped for but probably the best we can hope for, suggesting room to hold back on future hikes versus previous suggestions of a whopping four by end-2016 (markets still expect one at best).

China again weakest in Asia, heading for their longest losing streak in 3 weeks, as the price of oil retreats from its best levels on record US stockpiles, taking other commodities with it, and economic slowdown fears remain prevalent. Japan’s Nikkei is next weakest as investors get anxious ahead of the Bank of Japan’s 2-day meeting from which more stimulus is desired but not widely anticipated.

US bourses closed red yesterday after the Dow engaged in some extreme volatility around the Fed announcement - rates unchanged amid concerns about economic growth. Inflation still seen being walked all over by low oil prices, however note some fresh rhetoric from one of the world’s biggest producers, Russia, seeking to communicate with OPEC on action to bring crude prices back up

This month’s Fed assessment was somewhat darker than December’s (obviously) - risks no longer ‘nearly’ balanced with global economic developments to be watched closely. Message is largely unchanged regarding interest rates with gradual, small increases (blah blah blah) favoured, though the path the Fed laid out in December is likely to have both narrowed and lengthened. Don’t worry about March.

Corporate wise, in the key banking sector note Deutsche Bank confirming last week’s profit warning and 2015 net loss of €6.8bn as writedowns and restructuring bite hard. After all the worries about the Apple ship finally beginning to slow, note Facebook reporting record and consensus beating revenues, with 80% from mobile advertising via 1.6bn monthly users.

In focus today, look out for UK GDP seen accelerating to 0.5% in Q4, but slowing to 1.9% on an annual basis, this despite faster November growth in the dominant services sector. European Business Confidence figures are seen largely unchanged, although a worsening in German Consumer Price Inflation may prove a headache for ECB President Draghi.

In the afternoon, US Durable Goods Orders (notoriously volatile) are seen taking a dive in December although Pending Home Sales may back up the strong New Home Sales print yesterday. Results season sees the likes of Alibaba, Amazon, Baker Hughes, Caterpillar, Ford, Microsoft and Visa update on the latest quarter. While headlines figures (EPS, Revenues) tend to beat, thanks to management subtly reducing guidance in the run-up to the report, remember outlook is key.

Crude oil prices are flat this morning after benefiting yesterday with the above mentioned Russia/OPEC chat eclipsing record US stockpiles (which absolutely smashed forecasts). Both Brent and WTI are in misleading ascending triangle patterns, trading around the $32 level. Misleading because it seems unlikely that any form of cooperation between producers will happen. No one is currently up for forfeiting their market share first.

Gold is back testing rising support again having come back from a test of $1127 yesterday. We’re still looking for a decisive break above $1123. Note a 3-month bullish rounding (‘saucer’) bottom reversal taking form with potential for upside to $1160.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – it’s all part of the service.

UK Company Headlines: (Source: Reuters/DJ Newswires)

- Anglo American boosts annual iron ore output on Minas – Rio ramp up

- Anglo American Reports Lower Diamond Production Amid Weaker Prices

- FirstGroup warns on profit after flooding, driver shortages

- Lonmin keeps FY capital expenditure guidance of around $132m

- SSE loses 300,000 customers as users leave big suppliers

- SSE to Cut UK Domestic Gas Prices by 5.3%; Backs FY16 Guidance

- Diageo posts 1.8% rise in first – half sales

- Kaz Minerals says 2015 copper cathode output falls 3%

- AstraZeneca says US FDA grants Lynparza BTD for prostate cancer

- Babcock chief executive Peter Rogers to retire in August

- Babcock Intnl Names Archie Bethel CEO

- Daily Mail keeps FY revenue, profit outlook

- Coca Cola HBC appoints Anastassis G. David chairman

- AB InBev says partial cancellation of $75bln committed senior acquisition facilities

- Euromoney Quarterly Revenue Falls Amid Tough Conditions

- Mitchells & Butlers 17-Weeks Comparable Sales Down

- Cranswick 3Q16 Revenue +5%; Says Remains Competitive for FY

- Jimmy Choo 2015 Revenue +7%; Confident to Outpace the Market

- 3i Group Posts Higher Third-Quarter NAV Per Share