Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)!

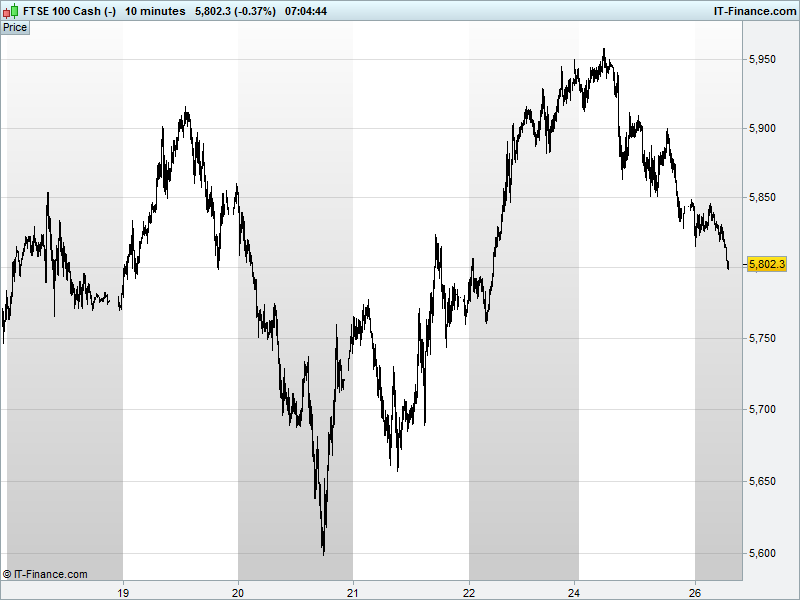

UK 100 Index called to open -75pts at 5800 with the 2-day rebound having already turned over, close to retracing 50% of its gains from 5600 3yr-lows. The failure at 5950 maintains shallow falling highs from 7 Jan and keeps the 2016 downtrend intact. Note Bulls still pinning hopes on a 2-week complex inverse Head & Shoulders reversal. Bullish 5860, Bearish 5785.

The negative opening call comes after Asian equities went into reverse following a weak US close on poor manufacturing data and central bank policy uncertainty. Also fuelling weakness was Oil breaking back below the now key $30/barrel ahead of US stockpile data which rekindled global growth concerns as major producers refuse to cut output..

After the recent rally, anxiety on the rise regarding the outcome of Fed and BoJ meetings this week (Weds & Friday) with much debate about whether the former hiked too early. Note ECB President Draghi forced to remain defiant on policy choices amid claims of lost credibility on inflation targets before it meets on 7 March.

Stocks in China have plunged to 13-month lows on capital outflow concerns from its transitioning economy and despite the PBOC flooding the system with cash to keep borrowing costs in check ahead of the Lunar Holiday.

US markets returned to red territory on Monday with the usual suspects - er, energy - leading declines on the back of tanking oil prices, which had previously enjoyed a strong rebound from multi-year lows helped by short covering. Note market bellwether Caterpillar sinking after Goldman Sachs downgraded the heavy machinery company to "Sell." CAT reports on Thursday.

The US Fed begins a two-day meeting today, but no change in rates is expected. Nonetheless, note post-meeting rhetoric coming out tomorrow for commentary on current market conditions.

In focus today amid a quiet macro line-up, we have US Housing Price data this afternoon seen delivering continued stable growth, although US PMI Services and the Richmond Fed Manufacturing may have ticked back in January, adding to the weak Dallas Fed that spooked US markets yesterday. Consensus expects flat US Consumer Confidence in January.

Keep an eye on GBP, the UK banks and property related stocks today with BoE Governor Carney testifying on the Financial Stability Report before the Treasury Select Committee. Note results out tonight from big hitters Apple , AT&T, J&J and P&G.

The catalyst for yesterday’s slippery crude sell-off that took the commodity back below $30 was put down to continued global oversupply as US supply is seen expanding the glut. Note also a delighted Iraqi oil minister said the country had pumped record output in December and expects to ramp it up even further this year. Well done you!

Gold’s uptrend continues with a good break above $1110 - that level now support - and the ceiling of a 10-day rising channel looking like the next target around $1123 or $1125. Global uncertainty & mainstream media fear mongering are doing good things for the yellow metal.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – it’s all part of the service.

UK Company Headlines: (Source: Reuters/DJ Newswires)

- Lamprell signs MoU over potential shipbuilding complex in Saudi Arabia

- easyJet says Q1 revenue per seat lower on Paris attacks

- Card Factory like – for – like store sales growth of 2.8 pct in 11 months to Dec.31

- Dixons Carphone edges up profit forecast on strong Christmas

- CMC Markets says London IPO priced at 235 – 275p/shr

- Carpetright says full – year profit expectations unchanged

- Builder Crest Nicholson says on track for further growth as profits rise

- Oil extends slide below $30 on oversupply, weak China data

- UK pub operator Marston's posts record Christmas sales

- PZ Cussons posts flat operating profit

- Savills Appoints Sky's Nick Ferguson Chairman From May; Peter Smith to Retire

- Norwegian Air Renews Flight Contracts With TUI, Thomas Cook, Nazar

- Greencore First Quarter Revenue Up; Reiterates Fiscal 2016 Expectations