Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

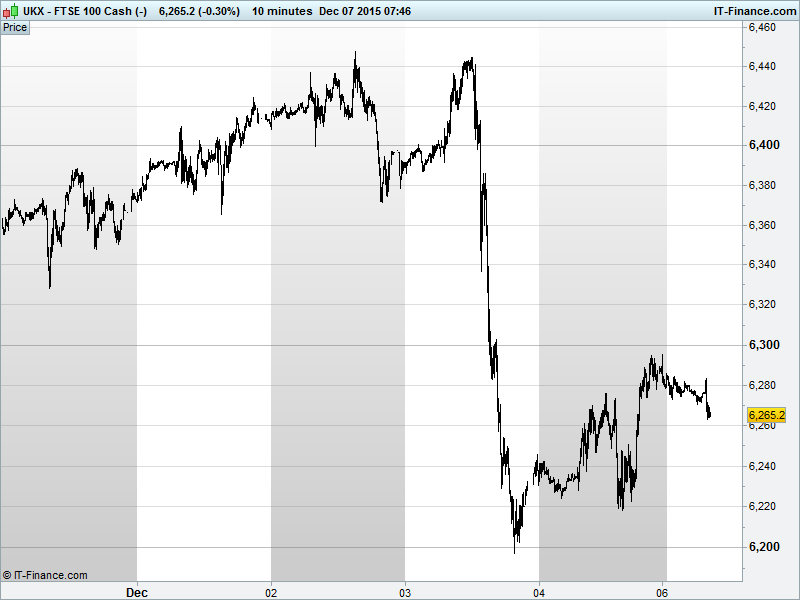

UK 100 Index called to open +25pts at 6265, still in an uptrend from 6200 lows of last Thursday but back from last Friday’s highs just shy of 6300. While the Bulls are looking for a break above 6300 to take us back to the 6450 ceiling, Bears are hoping the 6200-6300 bounce represents the flag within a bearish flag pattern, potentially taking us back towards 6100 rising support from end-August. Watch levels: Bullish 6290, Bearish 6235

The positive opening call comes thanks to Asian stocks rebounding into the new week after a strong US jobs report raised market-implied odds of a December Fed rate hike to 80% and gave the USD a leg up. Metals prices unperturbed by the stronger USD, buoyed by a more optimistic global growth outlook and increased Fed certainty, in stark contrast to oil which remains hindered by OPEC electing not to cut output.

Japan is the region’s outperformer with China, Hong Kong and Australia closer to breakeven as the stronger USD helped Nikkei exporters via a weaker JPY (despite the BoJ’s Kuroda saying no to negative rates) but the ASX held back by a stronger AUD and still depressed oil price even if the all-important metals prices are nicely off their lows to the benefit of the miners.

US markets rallied on Friday as confidence in the economy was bolstered after a jobs report that all but confirmed a December move away from record low interest rates. Note however the OPEC meeting failing to mention any form of output ceiling, further depressing the oil price and surely denting the Fed’s confidence in its outlook for inflation.

After the ECB underwhelmed last week with market expectations proven too high (markets’ fault or ECB’s? Likely a combo of the two), we feel it prudent to highlight that 80% market-implied odds of a December Fed rate hike also represents the chance that 80% of market participants are surprised/disappointed if Yellen & Co hold fire. And we now know how quickly crowded trades can unwind.

In focus today, amid a quiet macro line-up, will be the Eurozone Sentix Investor Confidence seen improving in December, and with the odds of a fed rate hike having risen, the US Labour Market Conditions survey. While many Jobs market conditions have hit Fed expectations, it can’t be said that all have (participation, people giving up looking), meaning heightened focus on all US data points ahead of next week's’ policy update. Watch what the Fed’s Bullard has to say after the European close.

Crude oil prices trading around fresh lows this morning with US Light dipping back below $40. Although there will no doubt be bottom pickers operating in the $30s, we’ve less reason now to expect a stay there to be necessarily short lived. OPEC seems to be fragmenting now, with an air of ‘every member for itself’ prevailing. without the protection of big producers like Saudi Arabia, smaller exporters will have little choice but to ramp up production, even if to do so would be counter-productive for the oil price.

Gold off its highs after the Friday US jobs report initiated a risk-on boost to equity markets, while commodity traders squared short positions in the yellow metal after it looked to have bottomed out around historic low levels. Since Friday’s impressive rally looks to have been the result of a short squeeze, a bullish pennant pattern on the 15-min chart should be viewed with caution.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – it’s all part of the service.

UK Company Headlines: (Source: Reuters/DJ Newswires)

- Serco warns on lower revenue, trading profit in 2016

- Meggitt forecasts 2016 revenue growth in low – single digits

- Prudential likely first UK insurer to announce Solvency II ratios

- Avanti Communications Wins New Contract with BT

- RBoS Selling Portfolio to Unit Of Cairn Homes for £360M