Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

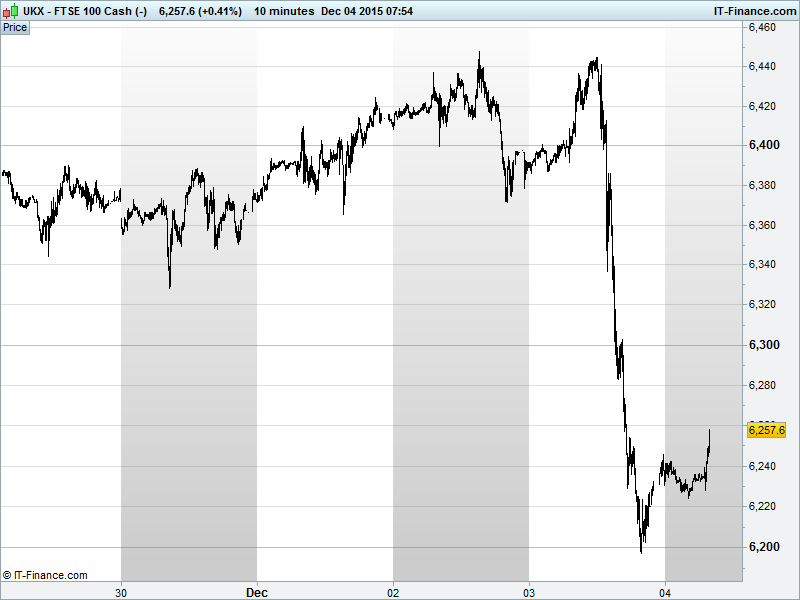

UK 100 Index called to open -20pts at 6255 with yesterday's strong sell-off from 6450 finding support at 6200 via the helpful combination of round number and intersecting resistance-turned-support from 9 September. The retreat reinforces both the recent ceiling at 6450 and the trend of falling highs since April. Rebound after over-reaction, or further to correct?Watch levels: Bullish 6255, Bearish 6215.

The negative opening call comes as markets continue to digest an underwhelming ECB policy update due to internal committee disagreements on what was required to foster regional growth. While deposit rates went further into negative territory and the quantitative easing (QE) stimulus programme was extended, there was no QE expansion as markets were expecting to help deliver a boost to Eurozone growth and counter deflationary risks.

With so much expectation going into the meeting, the resulting disappointment saw a rapid unwinding of very crowded trades which had been banking on further EUR weakness and USD strength and equities to march on north on the premise that an ECB stimulus boost would go some way to offsetting a Fed rate hike on 16 Dec.

However, could this suggest Draghi and Co a little more optimistic on the Eurozone outlook after recent data (German Factory Orders this morning, PMI data of late) a bit more like Fed Chair Yellen and her gang's view on the US? Should and could markets turn more bullish on Europe?

Asian stocks followed European and US bourses lower as hopes of looser Eurozone monetary policy were dashed. Despite being ready for a US rate rise, markets are still addicted to cheap money and loose monetary policy. The hope was that the required looser Eurozone policy would to some extent offset tighter warranted US policy based on divergent growth profiles on either side of the pond.

The US was certainly not spared the global market tantrum yesterday, ahead of a very important data print that could hammer the final nail into the coffin of easy policy. With such a massive, potentially overdone downturn experienced yesterday, could today present a bargain buying opportunity on Wall St indices? Remember, Non-farms will have to seriously disappoint in order to throw the Fed off its current path, while a half decent number will compound a positive outlook for the US economy and bring some certainty to the markets.

In focus today we have the US jobs report, expected to show further healthy Non-Farm Payroll (NFP) job additions in November and thus employment market progress allowing the US Fed to hike rates this month. The data, however, can be volatile, especially revisions, and October’s figure was very strong so could be marked down, offsetting a November beat. However, in our view a very poor report (jobs + wage growth) would be needed to derail the Fed’s well communicated plan to hike.

The OPEC meeting will also garner much attention with suggestions that the Saudis might be closer to agreeing to output cuts to boost the a depressed oil price resulting from a supply glut. After the ECB fiasco yesterday (erroneous early press comment, policy disappointment) it will be interesting to see what Draghi has to say this afternoon, along with Fed speakers Bullard and Kocherlakota.

Crude Oil prices ticked up overnight on a weaker dollar after currency traders piled into the Euro (ignoring Goldman Sachs’ bold but incorrect call) and Saudi Arabia talked of production cuts, with one caveat: that EVERYONE must cut production, not just OPEC. That likely to be the subject of discussion today at the OPEC meeting, while oil remains under pressure in the interim as players look to gain a competitive edge in hard times. This is about market share, but we’re wondering what the size of the market as a whole has to do with the portion of it that you control. Percentages are just that...

Gold is surely set for another leg down after benefiting yesterday from spoilt equity markets throwing their toys out of the pram and bringing the USD Index back from its lofty highs. Note falling highs overnight while gold is currently looking to test $1060 for the second time this morning.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – it’s all part of the service.

UK Company Headlines: (Source: Reuters/DJ Newswires)

- BAE Systems in bond issue totalling $1.5bn

- UKFI extends Lloyds Banking Group trading plan

- J D Wetherspoon says taking action after data breach of old website

- easyJet passenger numbers rise 9.6% in November

- IG Group interim CEO Hetherington assumes post permanently

- UK's IG Group appoints Peter Hetherington CEO

- Arbuthnot says unit Secure Trust to sell non – standard consumer lending business

- Builder Berkeley says on course to meet profit target

- Berkeley Group 1H Sales Up; Announces Enhanced Dividend Return Plan

- GVC says net gaming rev for 2–months to Nov. 30 +11.7%

- Go-Ahead Group sees impact of IAS19 in year to July 2 of about £37.8m