Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

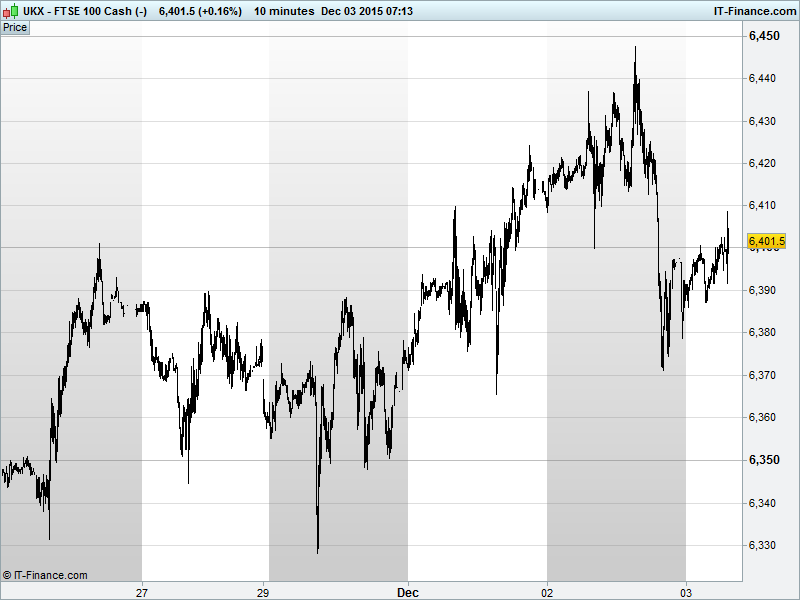

UK 100 Index called to open -15pts at 6405 after an about turn from yesterday’s 6450 highs maintained October’s resistance ceiling and a sharp decline sent us back below 6400 overnight. Following a teasing 6400 breakout yesterday that took us above 6-month falling highs resistance, the current uptrend now has an additional hurdle at 6450 before we can look to Oct highs 6490 and Jun falling highs 6500. Nonetheless, rising support from overnight 6370 lows offers potential for a second attempt at 6450. Watch levels: Bullish 6420, Bearish 6385.

The negative opening call comes after a cautious Asian session in the wake of a negative US close engineered by Fed Chair Yellen who added to USD strength by reinforcing expectations of a December rate hike sending commodities lower, notably oil ahead of the OPEC meeting at which it is speculated that Saudi Arabia could propose output reduction to boost the price of the black stuff. An S&P downgrade for major US banks (less government aid in times of crisis) also added to the fray.

US markets closed in the red on Wednesday, led lower by energy stocks. Crude Oil prices tumbled on continuing oversupply concerns (US inventories posted their 10th weekly gain) and a strong US Dollar which came on the back of Janet Yellen’s musings on the economy. That in turn did little to tempt opinion away from an imminent tightening of US monetary policy - incoming data seen consistent with continued improvement in the labour markets strengthening confidence in the outlook for inflation.

Not much inflation seen yet though, while Yellen seemed worried about an uncontrollable inflation explosion should the Fed hold off for too long. How long is too long? Why are we worried about inflation when it’s virtually non-existent?! Williams echoed the latter question in his comments - while still hawkish, he wants to see real evidence of inflation, rather than assume it will pick up, before tightening.

In Europe, note that unnamed sources suggested ECB macro-economic projections due today will be largely unchanged, prompting an overnight Euro rally. Expectations had been for growth and inflation forecasts to be cut, making the case for more stimulus. However, that may not now be necessary since the USD has done much of the hard work for Mario Draghi.

In focus today, the main event will be the ECB policy update where markets hope that President Super Mario Draghi delivers a hat-trick of stimulus measures to foster inflation and growth, both expanding and extending the current QE programme and taking deposit rates further into negative territory. Policy update at 12.45, but main event will be 1.30pm press conference.

Elsewhere, Eurozone PMI Services figures are seen confirmed as far healthier than their manufacturing counterparts earlier in the week, and Retail Sales for the region rebounding October. In the US PMI and IMS Services strong, in contrast to weak IMS Manufacturing this week, while Factory Goods Orders should have rebounded. Beware US Durable Goods Orders being very volatile and further Fed chat with Chair Yellen up again today along with Mester and Fischer.

Gold has bounced overnight from yet another visit to multi-year lows sub-$1050. Falling highs since yesterday evening though, as markets remain convinced the US will hike rates this month. So much so in fact, that tomorrow’s Non-Farm Payrolls report is seen as irrelevant with traders clearly not waiting around for it. As we said yesterday, Non-Farms will have to seriously disappoint in order to affect the Fed’s decision.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – it’s all part of the service.

UK Company Headlines: (Source: Reuters/DJ Newswires)

- Booker names Guy Farrant as chief operating officer

- Ex-South African fin-min Manuel joins Old Mutual

- Purplebricks conditionally raises 58.1 mln stg via placing, to list on AIM

- Russia's Polymetal proposes special dividend of $0.30/share

- Go-Ahead says London Midland awarded new contract

- Speedy hire appoints interim finance director

- DS Smith's H1 pretax profit down 26 pct to 91 mln stg

- Acacia Mining sees workforce down 27 pct on organisational recast

- Wood Group to Buy Infinity Group

- A.G. Barr Sees FY on Track