Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

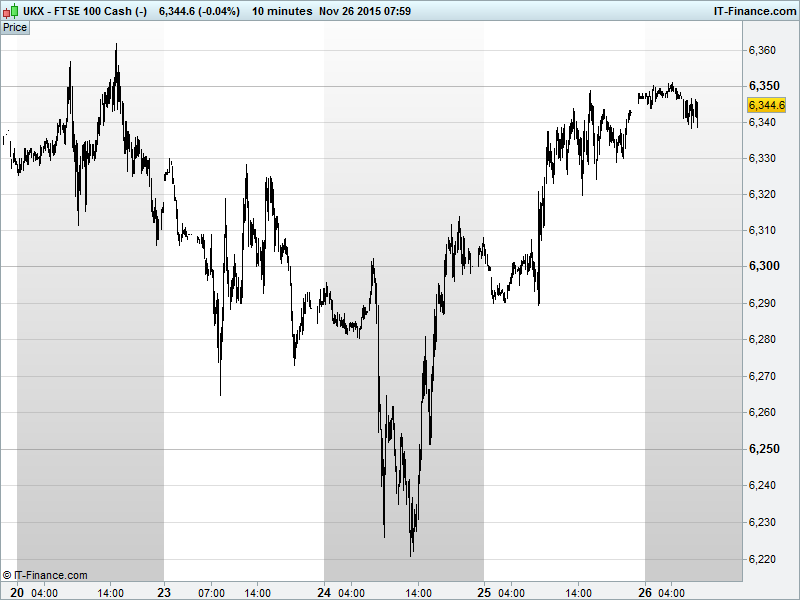

UK 100 Index called to open +5pts at 6340, having retreated from a fresh test of 6350 overnight and another flirt with the 100-day MA which has been a hurdle since late October. While the uptrend from Tuesday’s lows, and indeed those of 6000 last Monday, continues, significant resistance in the form of May falling highs looms large around 6380. Watch levels: Bullish 6390, Bearish 6315.

The tepidly positive opening call comes after a largely positive Asian session as industrial metals rallied and Oil prices held their gains following a flat US close ahead of the Thanksgiving holiday. While geopolitical concerns simmer (Brussels in lockdown, Turkey-Russia still trading accusations, US accusing Syria of buying oil from ISIS) investor sentiment buoyed by hopes of ECB stimulus next week ahead of a potential Fed rate rise mid-month.

Asian stocks show Japan's Nikkei higher as the JPY gives up some of its recent gains to help exporters. Australia’s ASX boosted by an AUD pullback as business investment contraction worsened sharply, adding to hopes of more economic stimulus, although plans for future spending grew healthily. Miners and Energy still in the doldrums.

Chinese equities bucking the positive trend in Asia-Pacific with expected changes to bond collateral rules seen as a warning against an overheating debt market, offsetting optimism about sales of state-owned companies such as PetroChina. Copper rallied as Chinese smelters said they would convene on Saturday to discuss what to do with prices at 6yr lows.

The last full trading day of the week for US markets saw them little changed at close, with waning volumes ahead of Thanksgiving. Healthcare stocks battled their counterparts in the Energy sector, presumably on hopes that a bumper year for pharma M&A windfalls will continue well into 2016. Macro data was largely positive, leaving everything in place (bar inflation, but who even cares about that?) for a December Fed rate hike. Or not.

In focus today, amid a quiet US holiday session, we have Spanish final Q3 GDP seen confirmed at a nice clip, although German GFK Consumer Confidence is seen unchanged. Thereafter with an absence of US data, we have ECB chat from Linde and then Japanese inflation very late.

Crude prices staged a nice bounce overnight to regain yesterday morning’s levels after US inventories increased by less than expected. Off those levels this morning, however, with many contracts having been settled pre-Thanksgiving holiday. Levels to watch on oil: Brent $45.50, $44.90; WTI $42.50, $42.25 (if volume allows…)

Gold is heading towards the apex of a 10 day narrowing pattern with an eventual break to the downside the more probable of the two outcomes given the lack of US activity, USD strength and resistance at $1071.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – it’s all part of the service.

UK Company Headlines: (Source: Reuters/DJ Newswires)

- John Wood Group wins $90m contract in Iraq

- Alliance Pharma says buys Sinclair IS Pharma's dermatology unit

- SSP Group says FY operating profit rises 10%

- McColl's CEO named non–executive chairman

- Daily Mail sells Wowcher, buys UK and Ireland units of LivingSocial

- Marston's full – year profit rises 10%

- Paypoint says H1 results in line with expectation

- Aker Solutions Gets NOK3.2bn Contract From BP in Norway

- Tesco Reaches $12M Pact To Settle US Income Overstatement Lawsuit

- Severn Trent Cuts Dividend to 32.26p Vs 33.96p