Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

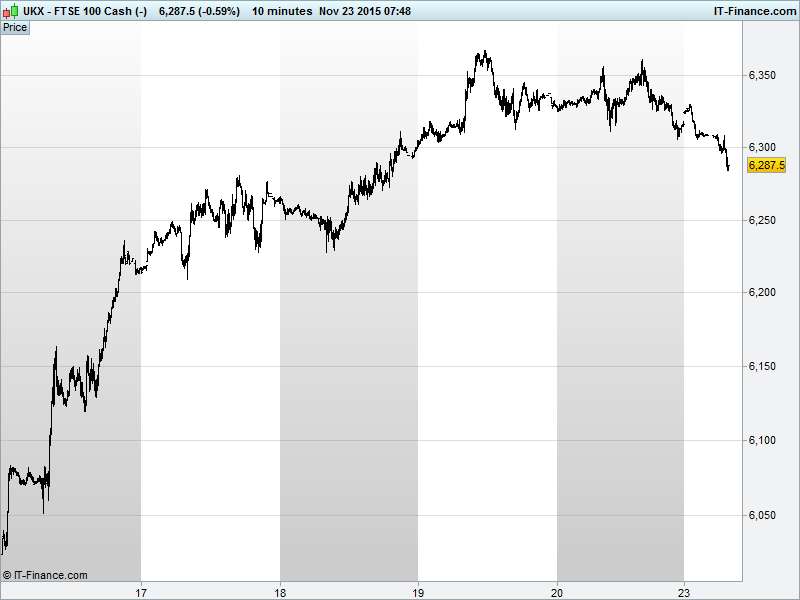

UK 100 Index called to open -50pts at 6285 having broken back below the intersecting trendline since 3 Nov lows and the neckline of a bearish double-top reversal that could complete at 6250. While still in an uptrend from August lows, the correction from last week’s highs continues after resistance at the 100-day MA following a strong 6.1% rally. Watch levels: Bullish 6315, Bearish 6275.

The negative opening call comes as the commodity rout continues (copper has gapped down), sending metals and oil lower as the USD creeps north on expectations of EUR-weakening ECB stimulus next week and a US rate rise mid-month. After the Parisian atrocities, note Brussels in lockdown for a third day on fears of an imminent attack while French President Hollande tries to rally a coalition to tackle ISIS and UK PM Cameron pledges £12bn extra military spending as part of his commitment to fight terrorism.

Asian stocks starting the week mixed (Japan closed) but optimistic. Chinese equities down despite a ban on IPOs being lifted with problems at a large brokerage leading to investor fears in the slowing debt-fuelled economy and its stock market. Regional sentiment hindered by pain in the commodity space after Venezuela said it sees oil at mid-$20’s if OPEC refuses to intervene to counter the global supply glut, however, Australia's ASX in the green as consumer stock strength offsets raw material weakness.

US bourses finished higher Friday while the Dollar held firm, supported by comments from New York Fed Governor Dudley who continued the trend of December rate hike expectancy. Williams, meanwhile, said there is a strong case for a rate rise assuming good data continues to flow and inflation picks up. The usual.

In corporate news, Pfizer and Allergan agreed on a $150bn merger deal that will create the world’s biggest drug maker, allowing the US behemoth to re-locate to Allergan’s home in Ireland and avoid costly US corporate tax rates.

In focus today we have Eurozone PMI Manufacturing & Services (regional and component) seen solidly above breakeven. In the afternoon, US Manufacturing PMI also expected unchanged but US Existing Home Sales may have cooled a touch.

Fighting talk from Iran’s oil minister sent crude prices tumbling over the weekend after he said the soon to be sanction-free state would do whatever it liked with regard to production. "...we don't need permission from OPEC or any other organization,” apparently, while USD strength and continued global oversupply are doing nothing to support oil. Note Venezuela seeing $20/bl if ‘action’ is not taken soon...

Gold has been flitting between a multitude of technical support levels around $1065. It’s still suffering, however, under a trend of falling highs that are basically mirroring the USD’s rising lows. Precious metals demand is seen lower also, with jewellery sales in China expected to slow significantly and an uncertain future for the Diesel engine putting added pressure on platinum.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – it’s all part of the service.

UK Company Headlines: (Source: Reuters/DJ Newswires)

- Mitie posts fall in first – half operating profit

- Just Retirement, Partnership Assurance deal completion seen in Jan 2016

- Segro acquires €93m Netherlands logistics portfolio

- AstraZeneca sells U.S. drug rights to Perrigo for $380m