Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

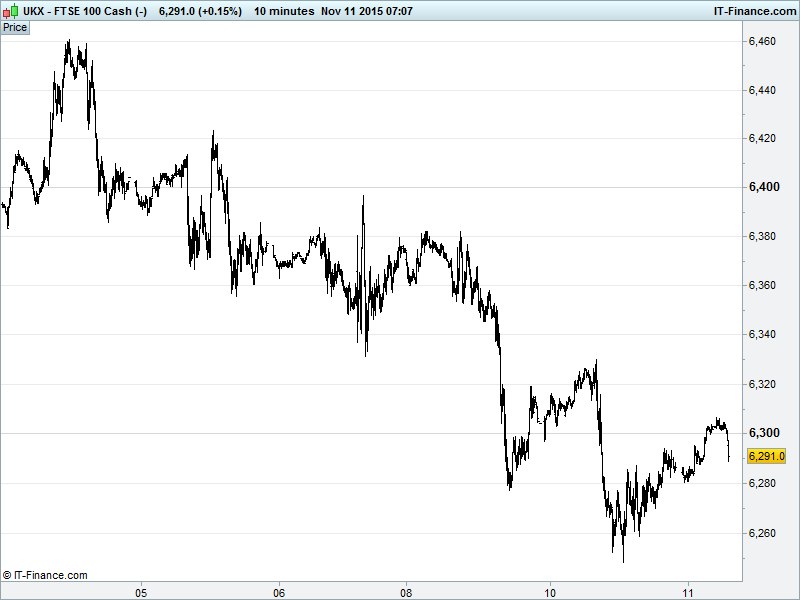

UK 100 Index called to open +20pts at 6295, still within a 1-week falling channel from 6460 highs. While an overnight rally was turned back at 6300 this morning, support at 6250 yesterday could keep the index above a 2015 intersecting trendline and keep the 1-month sideways shift intact. If we do get a rebound, however, upside could be capped at 6400 where we find falling highs dating back to late May. Watch levels: Bullish 6315, Bearish 6275.

The positive opening call comes despite more disappointing macro data from China, with Industrial Production growth matching its weakest since 2008, although Retail Sales improved. Coupled with on-line seller Alibaba looking like it's on track for a new ‘singles-day’ record we have further evidence of the nation’s shift from export-led to consumer economy.

Asian stocks mixed but muted, echoing the EU and US yesterday, with markets continuing to factor in divergent central bank policy and what it means for global growth and risk assets. While equities may still be correcting from recent highs, digesting strong rallies since late September, global sentiment remains bolstered by expectations of further stimulus from the PBOC, ECB and BoJ to offset a potential rate hike by the Fed in December.

China stocks down on increased worries about a deepening of the economic slowdown. Australia’s ASX buoyed by hopes of more China stimulus and despite commodities remaining under the cosh from a stronger USD and slower global growth. However the flip-side of that stronger USD sees it keeping the yen at depressed levels benefiting exporters on Japan’s Nikkei.

US equities were mostly higher on Tuesday, most notably the S&P500 which managed to pull out of a 4-day losing streak, although declines in tech stocks (incl. Apple on a cautious Credit Suisse note) muted the gains somewhat - Nasdaq naturally the underperformer there.

In Fed news, former US treasury official Neel Kashkari is to take over from Kocherlakota as Minneapolis Fed chief, from January and sure to bring a fresh plethora of commentary about interest rates! Dovish Charles Evans commented that there’s no point in hiking rates if a prompt U-turn might follow. Or a not very prompt U-turn - Evans is concerned about a potential return to the zero bound over the next 10 years following a December hike, if it happens.

In focus today will be UK unemployment even if inflation is the real bugbear for the BoE, preventing it from a rate hike. Wages growth may have accelerated, while joblessness should remain low. Elsewhere, it's all about those pesky central bank speakers providing their mixed messages about paths to rate normalization and/or more stimulus as may be the case today with the long list of ECB members on an agenda which includes President Draghi and his BoE peer Carney.

Both Oil and Gold remain under pressure this morning, despite slight upticks in Asian trade overnight, with a strong USD keeping commodities downtrodden. Continuing global supply glut worries adding pressure to both Brent and US Light crude which remain well within a $40-$50 sideways trading range. Note also ‘China slowdown’ making a fresh appearance on the wires with a focus on a weak copper price, languishing as it is near 6 year lows, and its implications for the global mining sector.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – it’s all part of the service.

UK Company Headlines: (Source: Reuters/DJ Newswires)

- Sainsbury's first half profit hit by deflation

- Tullow lowers 2016 capex by a third to weather weak crude

- Ophir says FY 2015 production is expected to be above previous guidance

- Barratt says performance on track as forward sales rise

- British Land secures 11 new lettings at Meadowhal

- Ultra Electronics says FY performance remains in line with expectations

- eSure says Q3 gross written premiums rise to 431 mln stg

- Flybe Group swings to H1 profit

- SSE profits rise as wet and windy weather boosts green power output

- TalkTalk says cyber attack will cost it 30 – 35 mln stg

- ICAP says H1 pretax profit 83 mln stg versus 36 mln stg year ago

- Tullett Prebon says to buy ICAP's global hybrid voice broking and information biz

- Fenner says FY revenue down 9%