Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

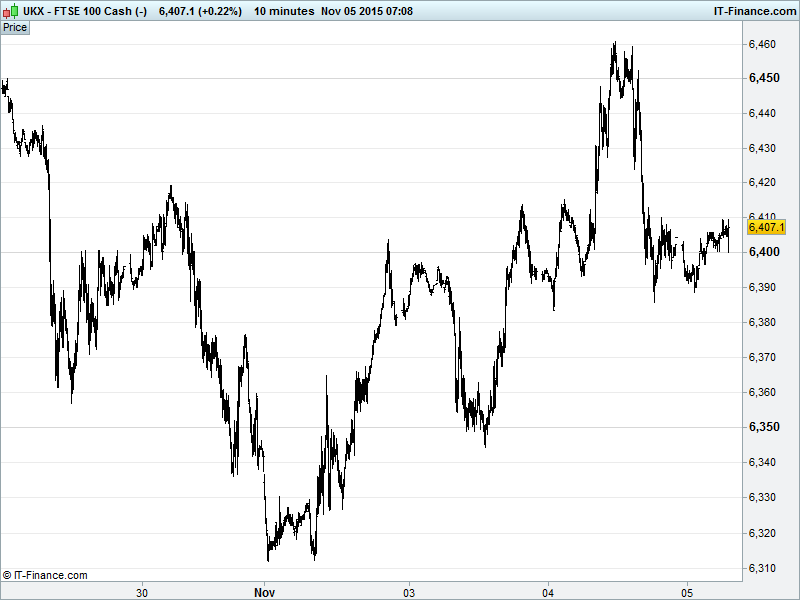

UK 100 Index called to open -5pts at 6405 having backtracked from 6460 to November rising support 6400 and the middle of what has developed into a bullish ascending triangle pattern. Potential for a breakout to see a revisit of 6700, backed up by the target corresponding with that for the Aug-Sept double bottom. As mentioned yesterday though, we have yet to trouble May falling highs. Watch levels: Bullish 6470, Bearish 6380.

The muted opening call derives from the US Fed staying on message suggesting potential for a December rate hike, citing further improvement in Labour and Inflation data as enough to act. This saw the USD move back towards summer highs and bets for an early Christmas Fed Present rise beyond 50%. A steady oil price, in the middle of its 2-month range, is also helping.

Asian stocks largely positive with the exception of Australia, where a stronger USD is weighing on the commodities space and RBA Governor’s comments about accommodative policy likely staying for some time, maybe even getting easier, suggesting sustained economic weakness. More gains in China see it flirting with bull market territory thanks to government support underpinning recovery from the summer rout.

Equities in Japan helped by the Fed strengthened USD seeing the JPY pull back to the benefit of exporters, while corporate results please (Toyota share buyback, Japan tobacco ups dividend) and despite there being no hints from the Bank of Japan’s latest minutes, despite calls for further assistance ringing loudly.

US bourses lower yesterday on Fed Chair Yellen’s hawkish rhetoric reminding us all that December is still a live meeting and that a 2015 interest rate rise remains a possibility. Bullard and Dudley in ‘complete agreement’ with Janet, and all of this amid tepid US data and still in contrast to hints of more QE in the Eurozone and, overnight, Sweden.

In focus today will be comments from ECB President Draghi at 10.45am given the hopes of more stimulus (mixed regional data of late) while the BoE (Bank of England) minutes and inflation reports at midday will be eyed for clues about the timing of policy tightening and a UK interest rate rise. After all the Fed speakers yesterday, we have Yellen, Dudley, Harker, Fischer and Lockhart all vying to keep us on our December toes this afternoon. Thoughts also likely to move towards the US jobs report tomorrow.

EIA data showed US crude inventories up by 2.8m barrels as forecast (not ‘to the barrel,’ surely!) despite a fall in imports. Rig count? What rig count? Brent and US Light both still trending sideways in 2 month channels. Oil may have bottomed, as Kuwait’s oil minister helpfully mentioned yesterday, but is still languishing near that bottom albeit it volatile fashion. Plenty of opportunities to trade it.

Gold has continued to retreat towards October lows $1105 amid talk of a ‘live December’ in the US and a resultant stronger USD. While unlikely from a macro point of view, a retracement in the Dollar Basket could indicate a bearish double top reversal which could bring buyers back to gold or even provide a trading opportunity in itself today.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – it’s all part of the service.

UK Company Headlines: (Source: Reuters/DJ Newswires)

- Schroders says Q3 assets under management fall 4.9%

- AstraZeneca lifts full-year forecast after in-line Q3

- Tate & Lyle posts higher profit for first half

- Just Retirement total sales rise 41%

- Cobham sees 2015 earnings at lower end of forecast range

- Coca Cola HBC net sales decline 2.7% in third quarter

- Cable & Wireless Comms first – half core earnings rise 4%

- Lancashire Hldgs books special dividend, Q3 net loss ratio falls

- RSA underlying 9mth premium income rises 1% to $6.8bn

- Sales dip again at UK grocer Morrisons

- easyJet's October passengers rise 9.7%

- Supergroup confident of delivering FY profits in line with guidance

- Randgold says Q3 profit falls to $48.8mn

- Howden Joinery says well positioned to achieve FY expectations

- Hilton Food says trading has been slightly above its expectations

- Amec Foster Wheeler raises cost – cut target, halves dividend

- Rentokil says FY guidance unchanged