Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

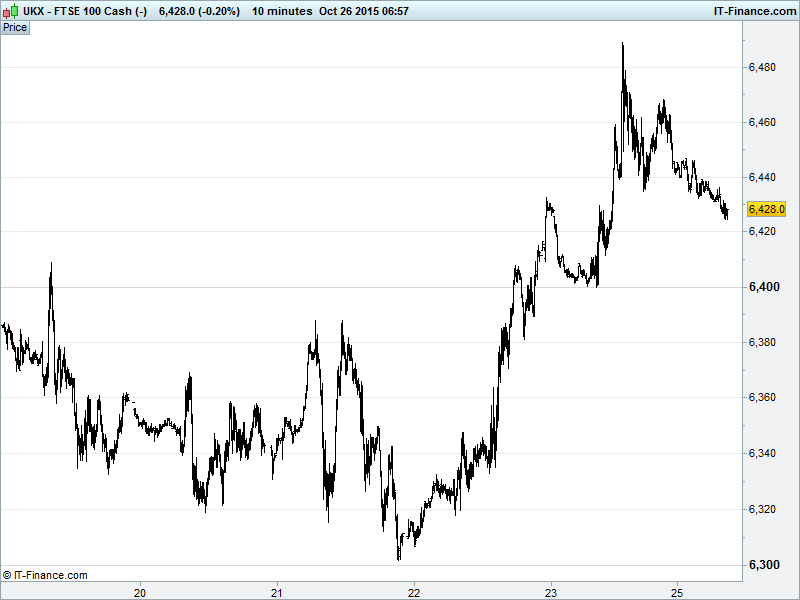

UK 100 Index called to open -15pts at 6430, back from last week’s late test near 6500 but still above 6400 highs of mid-month which keeps the index in its strong uptrend for October. Note the index still testing the 100-day moving average which maintains a sideways shift since early October. This could ultimately prove a bullish flag ‘pause’ before another 400pt rally taking it back to Jul/Aug highs of 6800. Updated watch levels: Bullish 6450, Bearish 6390.

The negative opening call comes as the excitement of last week’s ‘more stimulus’ (ECB, PBOC) rally runs out of steam, likely to allow the index to consolidate further after the 600pt/10% advance from end-September lows. Markets clearly still eager for cheap money to stick around for longer to cushion growth slowdown and happy to rally on any additional help/stimulus that central banks are prepared to dish out.

This follows a mixed Asian session, with China and Japan continuing to push higher (China 2-month highs) on stimulus hopes (China mulling more at 5yr plan meeting? Japan to deliver too?) and a decent US earnings season, but Australia flat after Chinese rate cuts strengthened the AUD and the ECB hints drove the EUR lower and USD higher at the expense of commodities and thus miners.

US equities posted moderate gains into Friday’s close following a week of dovishness (ECB hinting at continuation of QE beyond what is now tipped to be just the first round; Chinese interest rate/RRR cut) in Europe and Asia-Pacific. NASDAQ outperformed with positive reports from Microsoft (MSFT), Amazon (AMZN) and Alphabet (GOOGL) boosting sentiment in the tech sector both stateside and here in London (see ARM Holdings (ARM)).

Markets now widely betting against a Fed rate hike, with talk of timing being discouraged by commentators like Michael Ivanovitch (writing for CNBC) in favour of simply looking at the Fed’s books. We look ahead to this week’s Fed meeting under a shadow of global economic sluggishness after China’s ghastly GDP figure last Monday, Japan’s dismal trade balance and ECB talk of more stimulus.

In focus today: German IFO Business surveys are expected to have given up a little ground in October while UK BBA Home Loans will be eyed for UK housing market signals (note BoE Governor Carney’s warning to homeowners about higher interest rates) and UK CBI Trends data for what’s going on in terms of export orders deterioration.

In the afternoon, watch out for US New Home Sales seen falling a touch in September while a negative Dallas Fed Manufacturing index improves as the Kansas City Fed did last Thursday. Don't forget European clocks may have gone back an hour, but the US doesn't for another week so stateside data timings will be an hour earlier than usual.

This week note we also have the Fed policy update on Wednesday which is sure to generate much excitement while the UK banks kick off Q3 earnings season (Lloyds Wednesday, Barclays Thurs, RBS Friday).

Recent risk-on market behaviour has weighed on Gold with the yellow metal back below $1170 this morning on a firmer USD following confirmed Chinese stimulus measures & expectations for more of the same in Europe. This weakening the Yuan and the Euro while the USD strengthened, encouraged by some good macro data supposedly bolstering the case for a US rate rise (this bound to be temporary, as we’ve seen time and time again). Note, however, that CTFC data suggests net long positions in Gold futures have risen to the highest level since Feb.

Crude Oil still struggling with global oversupply since 2014. Speculators cutting bullish bets on the commodity which should keep prices muted and highly unlikely to make it above $60 for any length of time. Both Brent and WTI suffering under nearly 2 weeks of falling highs.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – it’s all part of the service.

UK Company Headlines: (Source: Reuters/DJ Newswires/Bloomberg)

- Randgold says Tongon mine paid off shareholders' loans

- Alent says Q3 NSV -3.5% to £100.7m

- Anglo Pacific Group says not aware of reason for share price decline

- Georgia Healthcare sees IPO priced at 215 – 315 pence per share

- Net sales growth accelerates at Britain's WPP

- Low costs keep IndiGo flying high in India's cut – throat airline market

- Escher Group Holdings CFO steps down