Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

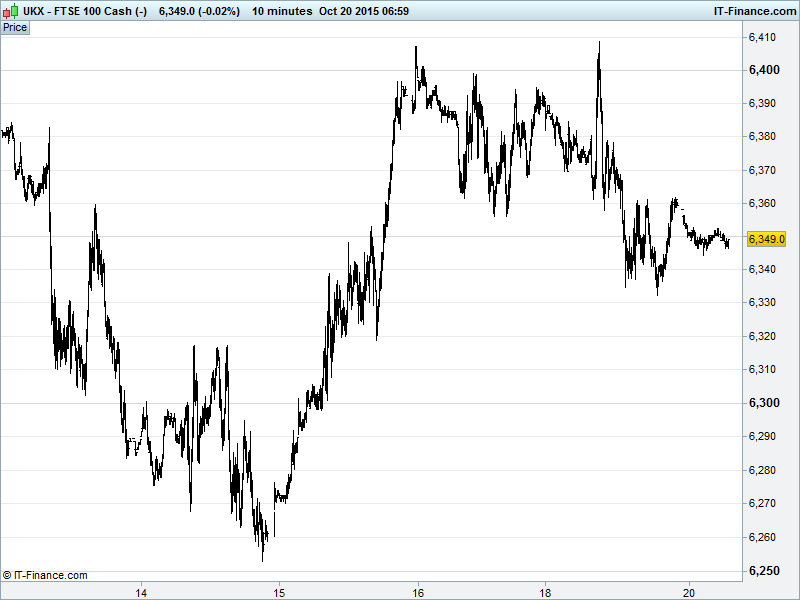

UK 100 Index called to open flat at 6348. Note daily RSI testing hitherto strong rising support line, still not showing overbought though which could still indicate consolidation rather than imminent correction. 6400 remains key level for the index. Updated watch levels: Bullish 6460, Bearish 6220.

The flat opening call for European equities comes after a volatile start to the week as Chinese macro-data rumbled the UK 100 – mining stocks dominating declines as per usual in these situations – with the data not seen quite bad enough to warrant further aggressive stimulus measures by the Chinese government, the upshot of that being that nothing much has changed (or is likely to any time soon). Commodities still downtrodden, UK miners back on the bears’ books, UK 100 still in consolidation.

Asian bourses mostly lower this morning with that Chinese sluggishness putting a dampener on investiors’ risk sentiment. Note the amount of money being pulled from Chinese markets has topped $500bn for the year to date according to US treasury calculations.

In Australia, the RBA released meeting minutes today, with nothing new announced save a progress update on the fallout from 2 interest rate cuts this year, seen to be providing enough support for economic rebalancing so as not to require a third just yet. Aussie Dollar still depreciating in value.

US stocks just off flat yesterday (DOW +0.09%, S&P +0.03%, NASDAQ +0.38%) with energy sector declines holding US indices back (oil dropped on Iran production data).

Corporate-wise, Morgan Stanley nursed heavy losses following disappointing Q3 earnings with trading revenues -15%. IBM also suffered after its own Q3 report, shares -4%. Be aware of ripple effect in UK banking and tech sectors. (LLOY, RBS, BARC, ARM...)

Fed chat saw Williams declining to pin down an exact timetable of US fiscal policy normalisation, repeating the need to rely upon data (I think if that carries on, we may never see a rate hike). That combined with the usual side order of ‘we should do it slowly and carefully.’ Boring, but cheap money for longer is good for everyone.

Note European Central Bank’s Noyer going a bit more hawkish than has been customary of late, arguing that Eurozone QE is right on the money.

Crude oil lost steam yesterday and stabilised overnight following Iran production figures that saw concerns about market oversupply from the nuclear deal with the US re-surface. UK oil stocks bound to feel the pinch today…

Gold still in a downtrend on Fed rate hike uncertainty (certain uncertainty), extending losses to four days, not helped by China concerns.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – it’s all part of the service.

UK Company Headlines: (Source: Reuters/DJ Newswires)

- Costa Coffee owner Whitbread posts higher profit

- ASOS year profit edges higher

- Petropavlovsk says Q3 gold output down 24% YoY

- John Wood Group wins $31mn coalbed methane contract in US

- Sirius Minerals plans construction of York potash project in 2016

- Photobox receives buyout offer from Exponent Private Equity and Electra Partners

- Grainger appoints Vanessa Simms as new finance director

- Genel cuts 2015 production guidance

- Go – Ahead maintains FY expectations

- Polymetal says Q3 output up 10%

- InterContinental confident in outlook for the year

- Informa reaffirms FY outlook

- Taste Holdings says legal proceedings against co and Domino's Pizza Intl withdrawn

- Stagecoach announces early redemption of bonds due 2016