Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

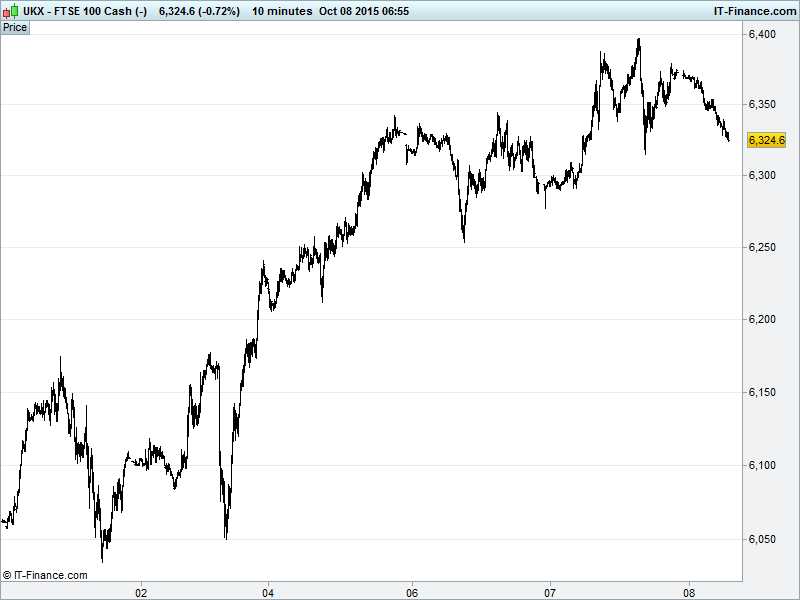

UK 100 Index called to open -10pts at 6325, still holding above 6300, but retreating towards yesterday’s late session lows 6315. This follows an evening rally and another attempt at 6400 which turned back at 6380. Of concern is the break below 3-day rising support at 6325 which, if followed by a break below 6300 would put us back in September’s sideways channel. However, so long as 6300 holds up potential exists for this to be consolidation (normal after 9% bounce) before another push towards 6600 June falling highs. Unchanged watch levels: Bullish 6360, Bearish 6290.

The negative opening call comes after a largely negative Asian session, with the exception of China which was playing bullish catch-up after a week’s holiday for Golden Week, but perhaps less than many had anticipated in light of stimulus hopes. The losses in Asia are in contrast to decent gains by US bourses (S&P at 7-week high; Biotech rebound, Energy extends rise thanks to commodities bounce) which themselves compare to European bourses having closed near session lows.

Overnight sentiment hurt by a surprise announcement by German banking giant Deutsche Bank (DBK) which unveiled the firm’s biggest quarterly loss (€6bn) in more than 10 years due to major impairments related to higher regulatory capital requirements and the disposal of Postbank which may result in a cut to its dividend as it tries to avoid a dilutive cash call.

Japan’s Nikkei in the red as a plunge in Machine Orders adds to a raft of recent data supporting the need for stimulus intervention to bolster growth and inflation. Mixed contractionary surveys added to the uncertainty but raises expectations of the BoJ acting at month-end. Maybe even in addition to the government in the interim. For those worried about global growth, the IMF’s Vinals warned that he expects the Fed to hold a little longer, but sees no financial crisis in China.

Concerns about US earnings season, which kicks off with Alcoa (AA) today, continue to rise with fears that revenues growth among the major banks will have halted in Q3 after the summer financial market rout which hindered key bond trading revenues, while commodities names could announce need for more painful measures. This was countered to some extent by PC giant Dell’s potential combo with cloud-computing EMC.

The ugly head of geopolitical risk remains very much raised with Russia adding to its airstrikes with warships firing cruise missiles at Syrian rebels all the time Putin saying he wants to form an ISIS-fighting coalition. What is he up to? Really.

In focus today we have the UK’s BoE rate decision which will surely be a non-event but is accompanied by key meeting minutes which will be important for updated views on reasoning for holding pat; what are its concerns? Has voting shifted? The same is true for the even more important ECB and Fed minutes later in the day. In the afternoon, US jobless Claims seen very flat. While the calendar may be data-light, the line-up for speakers is choca, with the Fed’s Bullard, Kocherlakota, Williams and the IMF’s Lagarde and BoE’s Carney.

The Oil price is off its recent highs as expected, with US inventory increases capping gains and production unexpectedly increased. The pullback follows a strong rebound on price rise/spike concerns as the supply glut slowly corrects via lowered investment.

Gold has also pulled back from a near re-visit of late September highs. This sees the bullish flag pattern fail to complete and brings the price of the yellow metal back below the 8-month trend of falling resistance at $1150.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – it’s all part of the service.

UK Company Headlines: (Source: Reuters/DJ Newswires/Bloomberg)

- Tullow Oil reached agreement with Gabon govt for license extensions in Onal complex fields until 2034

- Tullow Oil maintains full year production guidance for West Africa at 66-70,000 bopd

- Tate & Lyle reaffirms FY outlook

- Mondi Q3 underlying operating profit +27%

- Fastjet signs sales and distribution contract with Emirates

- Dunelm reports "strong" trading, like--for-like sales +5.5%

- Centamin maintains FY production guidance

- Electra calls on investors to reject Bramson bid to join board

- GVC says "highly confident" of outlook for rest of 2015

- Hays Q1 fees grow, warns on adverse currency moves

- DFS says FY revenues +7.5%

- Victrex Performance in Line With Expectations