Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

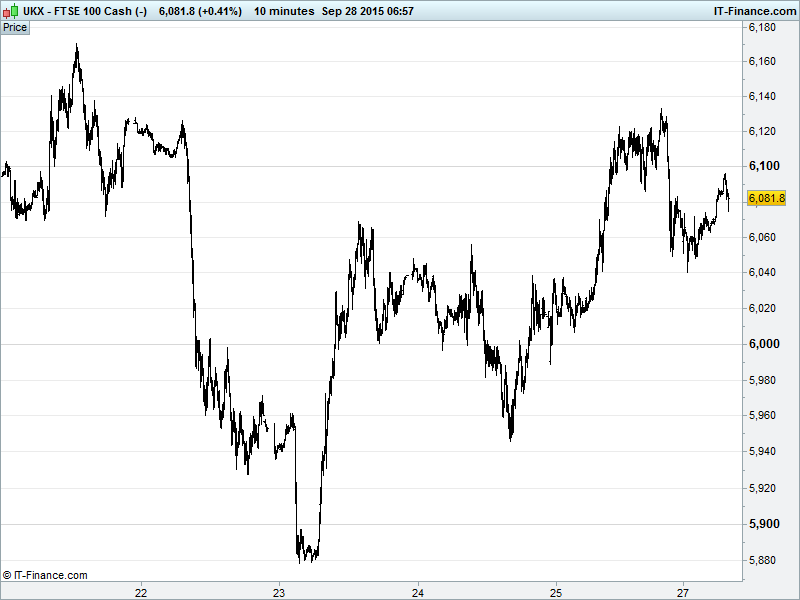

UK 100 Index called to open -25pts at 6085, trading back from Friday’s 6135 highs but finding support at 6050 overnight. This maintains last week’s uptrend from 5878 lows and keeps the index in a 5880-6270 channel from 25 Aug. While a short-term breakout was delivered Thurs/Fri, until channel highs of 6270 are tested the over-riding downtrends from 6770 in mid-Aug and 7135 in April remain. Updated watch levels: Bullish 6140, Bearish 6030.

The negative opening call comes after August Chinese Industrial Profits declined at their fastest annual pace since records began four years ago, with growth hurt by currency devaluation and financial market volatility, which just adds to the growing slowdown worries overshadowing the world’s #2 economy and impacting the commodities space.

A pro-independence win for the Catalonia electorate also adds to Eurozone political risk, showing desire for the key state to break away from Spain and means the likelihood of an official Scottish like ‘Yes or No’ vote in the next 18-months.

Asian bourses echoing the mixed US close with Chinese equities at 1-month lows following yet another macro data disappointment which is weighing on Japan’s Nikkei, the regional underperformer despite a JPY trading back from Friday’s highs and hindered by many equities going ex-dividend.

Australia’s ASX is the regional winner this morning despite China woes and commodities still under pressure from a strong US dollar, with M&A riding to the rescue in the telecoms sectors (Vocus Communications agreed to buy M2 Group for A$1.9bn).

On the topic of M&A note the Sunday Times reporting that AB Inbev could be just days from submitting a £70bn bid for UK Index -listed SAB Miller (SAB), while Vodafone (VOD) says Liberty Global has ended talks over a deal to exchange assets. Too add to the mix Chief Lagarde says the IMF is likely to cut global growth forecasts for 2015-2016 which are unrealistic.

US markets closed mixed Friday with (now overvalued?) biotech stocks dragging on stateside indices amid accusations of profiteering – that leading to net losses for the week. Fed chatter again hawkish, citing a US economy that’s in good health and ‘rate rise ready’ as Kansas Fed’s Esther George sought to play down fears sparked by the FOMC’s decision to keep rates unchanged earlier in September. After Yellen was herself more Hawkish last Thursday, the question remains: if they’re so adamant it’ll happen in 2015, why are they waiting?

In focus today, in the wake of a stronger US Q2 GDP revision than expected, we have US Personal Income and Spending and Pending Home Sales which are all expected to show more solid growth. Thereafter, the Dallas Fed Manufacturing Index is forecast to improve, in contrast to surprise misses by Richmond and Chicago last week. To keep the Fed uncertainty alive we have Dudley, Evans and Williams all speaking this afternoon/evening.

Crude prices fell in Monday Asian trade with a drop in the Baker Hughes Rig Count for the fourth week in a row putting up little resistance in the face of broad global growth concerns. Focus will be on US production figures this week as China gears up for a 7 day public holiday beginning on 1 Oct – so that a sharp drop in trading volume (China) should be weighed against any changes in production (US) in order to forecast price direction. Brent currently $48 while US Light Crude trading around $45.

Gold ($1144) holding its value in a tight range, as is the USD Basket this morning, with investors still trying to gauge the likelihood of a US Fed rate hike. The question at the moment being “what does the Fed know that we don’t?” since there’s much hawkish talk of the US economy being ready, yet no move to raise rates. The outlook for Gold is highly dependent on this.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – it’s all part of the service.

UK Company Headlines: (Source: Reuters/DJ Newswires/Bloomberg)

- Vodafone says Liberty Global tie-up talks ended

- Shell to cease further exploration in Alaska

- Regus names Dominik de Daniel as CFO

- Bowleven says strikes hydrocarbons in Moambe well

- Speedy Hire sees profitability materially below current market expectations

- Shanks says full-year expectations remain unchanged

- Pennon on track to meet management expectations for 2015 – 16

- Fastjet expects "a material increase in the loss expected for 2015"

- Glencore to Sell Nickel Project in Brazil to Horizonte Minerals for $8m

- Royal Dutch Shell to Cease Exploration Activity Offshore Alaska