Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

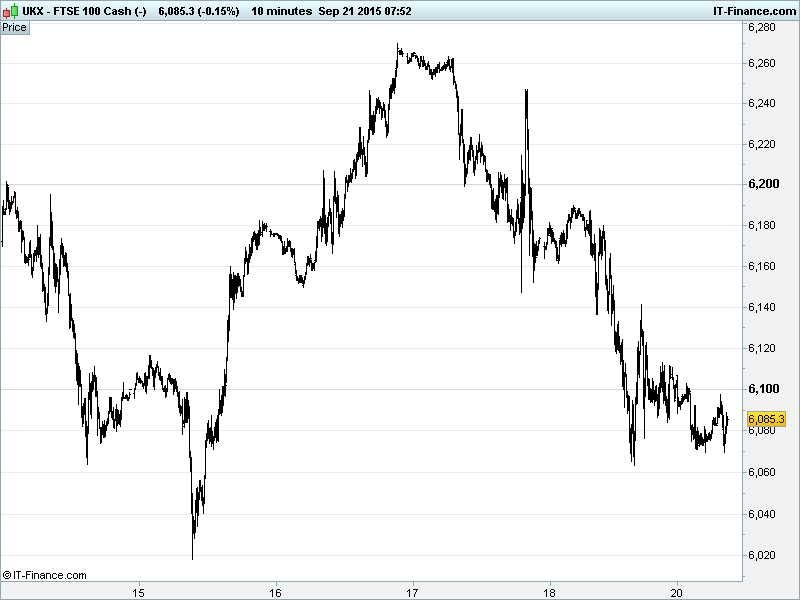

UK 100 Index called to open -20pts at 6085 having broken down from a 3-day bearish head and shoulders top pattern, approaching its target of 6050 and the trendline of rising support dating back to Aug 26. Bulls looking for a bounce from 6050 to keep August's uptrend alive while bears are looking for the retreat to continue towards 6000. Updated watch levels: Bullish 6115, Bearish 6040.

The negative opening call comes as Asian stocks underperform US bourses which had already delivered a weak session on Friday. The drivers for this poor start to the week come from renewed concern about China & global growth following last week’s Dovish Fed update, the Moody’s downgrade of France and China’s MNI Business Indicator posting a bleak future, dropping 8% in September.

Chinese stocks are outperforming (intervention?), with Japan’s Nikkei hindered by the stronger JPY and China growth concerns. The latter continues to weigh on major trade partner Australia which has also suffered from a stronger AUD post the USD-weakening Fed update.

Note the Greek electorate’s third trip to the polls in 9 months has seen PM Tsipras’ Syriza coalition embraced (35.5% vs 28.2 for New Democracy) despite having reneged on promises, given up much ground on a 3rd bailout and taking the nation to the brink of a euro-exit. This should at least provide some stability in terms of keeping to the terms of the bailout before the first progress review.

US stocks closed with slight losses on Friday as a risk-off mentality prevailed into the weekend after concerns regarding the health of the global economy were cited in the FOMC’s decision to leave US rates unchanged. Increasing support for a 2015 hike was evident over the weekend, however, with the Fed’s Bullard saying he voted against Thursday’s decision and Williams talking of a close call in the vote, adding that the next logical step should be a slow series of rate rises likely beginning before the end of the year. Bad data deemed transient with both inflation and employment expected to move towards target levels in the near future.

The Fed update continues to be digested with much debate about whether a rate hike is still warranted by end-2015 (thank Fed FOMC members for kindly adding fuel to the fire this weekend), in-line with Yellen’s promise (which is of course made to be broken). Are market forces too great outside the US? Can Fed not see it is responsible for much of the volatility it is complaining about?

Note a report in The Telegraph talking of Bank of England’s Haldane suggesting that negative interest rates and an increased inflation target for the UK could be appropriate to stave off another recession.

After the M&A train gained steam last week, the decision by Zurich Insurance (ZURN) to abandon its £5.6bn bid for London-listed RSA Insurance (RSA) after going over its accounts may dent sentiment a touch.

In focus today we have only US Existing Home Sales at 3pm, which are seen weaker in August. Bar that data, we have the fallout from the Greek election, continued debate about the Fed rate hike as well as ECB and Fed speakers all afternoon.

Crude prices took a tumble on Friday with traders fearing a bearish global economic outlook that would see the world’s biggest producers continue to flood the market simply to maintain market share. The Baker Hughes rig count sunk in over the weekend, however, posting a 3rd straight fall in US operational drilling rigs and helping prices off their lows allowing Brent to hit $48 and US Light Crude $45 this morning.

Gold ($1139) flattened out after regaining early Sept levels around $1142. Post-FOMC safe haven demand held into the weekend on global uncertainty. Note US Dollar basket staged an impressive recovery from Friday/early weekend lows, putting the brakes on Gold’s gains.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – it’s all part of the service.

UK Company Headlines: (Source: Reuters/DJ Newswires)

- AO World sees 20% - 21% revenue rise for Sept quarter

- French Connection says H1 revenue down 9.8%

- Stobart Group signs long – term biomass supply deal

- RSA says Zurich ends deal discussions, July, August trading has been positive

- PureCircle says FY15 sales up 26 pct

- UK Commercial Property Trust completes asset swap with Segro

- Shire receives European Commission's approval for Intuniv

- Inmarsat partners Deutsche Telekom and Lufthansa in aviation broadband

- Balfour Beatty says Carillion JV selected for £292m A14 scheme