Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

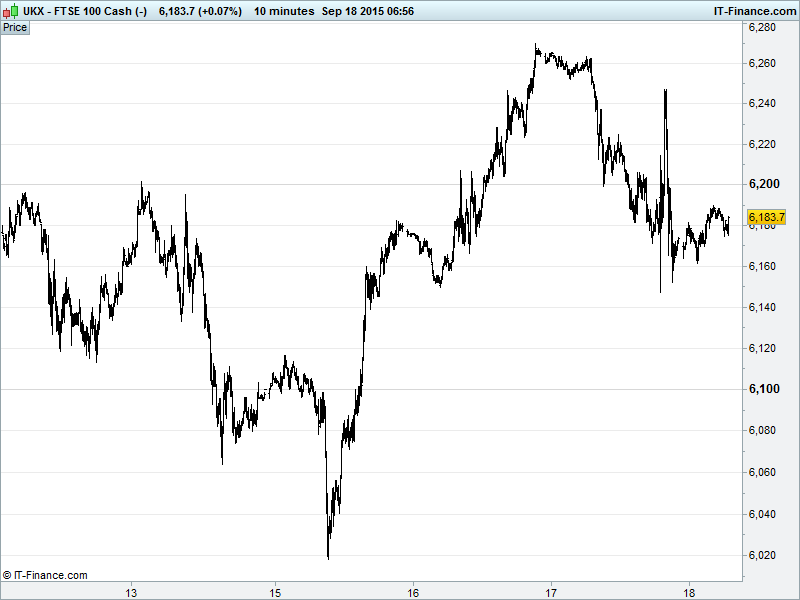

UK 100 Index called to open -10pts at 6175 having continued yesterday’s risk-off retreat from highs of 6265 (although not without Fed-induced volatility). The mid-week rise and fall hints at a bearish head & shoulders top reversal pattern; a breach of 6150 neckline could see downside to shallow rising support around 6050. A bounce from 6050 would keep uptrend from end-Aug alive and kicking, while recovery from current levels would probably find a hurdle in recent highs 6250-6275. Updated watch levels: Bullish 6205, Bearish 6140.

The mildly negative opening call comes after the US Fed FOMC surprised markets not so much by leaving interest rates on hold but with a much more dovish tone than expected. Markets had anticipated either a dovish hike (easy does it) or a hawkish hold (be prepared), but the potential ‘surprise’ (we remain concerned) we had discussed was duly delivered. While markets had desired clarity, it appears that uncertainty (and volatility) may be here to stay (December hike, Jan, later?).

The Fed’s surprise decision to hold pat shows external factors clearly outweighing domestic progress where Labour markets have improved markedly and growth is at least present, even if inflation remains suspiciously absent. The Fed Chair’s warning about global market developments (read market volatility), and China in particular, potentially derailing US growth and supressing already low/no-flation shows how pivotal the decision to hike is/will be.

Rate hike estimates by FOMC members being pushed out yet further, coupled with reduced growth and inflation forecasts and a continued monitoring of external risks is likely to keep markets and investors guessing through year end. Could continued Fed hike delays mean the BoE is first to hike next year? Could the ECB be pushed to boost stimulus (more, longer)?

Asian markets mixed overnight, echoing the US close, with concerns about growth raised by the Fed’ cautiousness. With one lot of uncertainty out of the way (kind of) it’s time to look back to Greece where the weekend election (2nd this year) is an equally close call and could have ramifications on bailout. On a brighter note, China Property Price weakness fell in August.

US markets took a round trip – good gains followed by a full retracement in pretty quick succession after the FOMC decision to keep US interest rates unchanged in September. Resultant USD weakness saw Gold ($1129) rally, with demand for the yellow metal seemingly boosted by Yellen’s reasoning: While risks to the US economy are balanced, rumblings in China and general global uncertainty are weighing heavily on the domestic inflation outlook. To that end, October remains a live meeting, but many now seeing rate lift-off pushed back until 2016.

In focus today will, of course, be Fed decision digestion (or indigestion) and in the absence of major data bar the US Leading Index in the afternoon (rebound expected) we have the ECB’s Coeure speaking late-morning and China’s Chief Economist speaking mid-afternoon.

US Light ($46) and Brent Crude ($48) weakening this morning (yet still headed for week-long gains) after traders saw the FOMC decision as reflecting lower perceived demand from emerging markets. Growing stockpiles indicating global oversupply and a USD rising off overnight lows adding to downwards pressure.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – it’s all part of the service.

UK Company Headlines: (Source: Reuters/DJ Newswires)

- Poundland plans to complete 99p Stores deal by September end

- APR Energy commissions new Botswana project

- Pace says Arris deal on track, cuts 2015 revenue outlook

- Petra Diamonds FY revenue falls 10%

- Ferrexpo says its operations not yet impacted by Bank F&C woes