Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

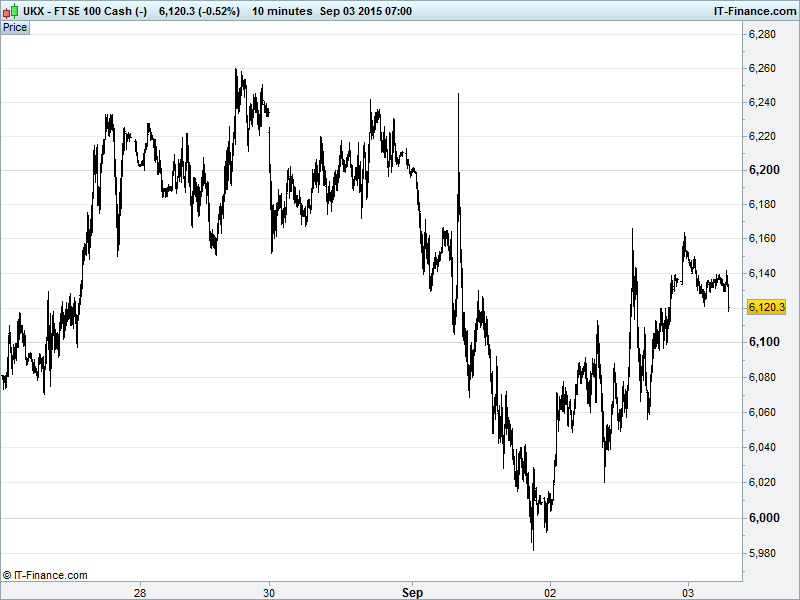

UK 100 Index called to open +70pts at 6150 but still struggling under the weight of falling highs from 10 August, compounded by the breached neckline of the 27-31 Aug H&S top pattern becoming resistance. A breakout above 6165 likely required to tempt adventurous bulls and a bettering of late Aug highs 6260 before convincing the masses. Watch levels: Bullish 6180, Bearish 6090.

The positive opening call comes after Asian stocks posted gains thanks to a 2-day Victory Day National (and thankfully financial markets) Chinese Holiday provided some much desired respite from the economy and market that has been at the heart of the elevated global volatility of late. Hopes also rising that ECB President Draghi may signal QE extension.

With markets still worried about the Fed raising interest rates this month, US markets (led by Tech) built on positive jobs data and Beige book thanks to comments from Bill Gross that even if the Fed does hike (no guarantee), it is likely to wait a couple of quarters before doing so again even if markets are factoring in a 12-month wait.

Japan’s Nikkei benefiting from Chinese calm, a stronger USD and thus weaker JPY as well as improvements in both PMI Services and Composite. Note Bloomberg highlighting bearishness via options data with the cost of bets for a 10% Nikkei decline at their highest versus those for a 10% rally since 2011 and the ratio of bearish to bullish contracts is at its highest in 5 years. Australia’s ASX in the red despite China closure as the AUD weakens toward a 6-yr low after retail sales unexpectedly fell and despite a smaller and reduced trade deficit.

US stocks bounced on Wednesday (NASDAQ out of correction territory, +ve for the year; S&P and Dow both still –ve) in a continuation of recent volatility with bargain hunting traders racing to get in on Morgan Stanley’s market bottom call. Mixed macro data included a kind of good ADP report that showed an increase in private sector employment that nonetheless fell short of expectations. A similar story for factory orders.

The latest chapter in the Fed’s rather long magnum opus – The Beige Book - showed economic activity continued to expand across most regions and sectors during through July and mid-August, with most districts reporting growth in labour demand and tightening labour markets pushing wages up slightly in a few sectors. A tough read, this one.

In focus today we have Eurozone Aug Services PMI data in Europe with slight deteriorations expected in France, Germany and Spain but the regional print improving thanks to gains by the likes of Italy while the UK’s own reading is seen gaining on existing strength. Eurozone Retail Sales forecast to rebound in July.

In the afternoon, it’s all about the ECB policy update, not for any changes in rates rather the press conference and the outlook/economic projections for the region in light of recent market volatility and global growth uncertainty with lacking still inflation further hindered by lower commodity prices. Draghi to talk down the Euro again? Extend QE beyond next summer? US PMI Services seen flat although the ISM version may have given up some ground from a very strong July print.

Gold ($1132) traders wary of taking up fresh positions ahead of US non-farm payrolls, that report potentially bringing more clarity on the likelihood of a US interest rate hike this month (that meeting taking place on 16 & 17 Sept). Volume also hit by the Chinese markets being shut Thursday and Friday for public holidays, while a stronger USD is also keeping demand for the yellow metal subdued.

Oil supply glut worries dominating crude markets again after a 4.7m barrel increase in US stockpiles reported by the EIA (biggest one-week increase since 17 April), smashing forecasts of just 444,000. This came after a similarly huge US API inventory report on Tuesday. Volume again hit by China public holidays. WTI $46 and Brent $50 currently off their overnight highs after yesterday’s rebound.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – it’s all part of the service.

UK Company Headlines: (Source: Reuters/DJ Newswires)

- EASYJET Strong summer trading delivers higher profit expectations the year

- Barclays announces further Non-Core disposals

- WIZZ AIR grows August passenger numbers by 19%

- GO–AHEAD year profit up 11.1 pct

- Mosman Oil & Gas inks deal for assets in New Zealand

- Booker Group says CMA clears acquisition of Londis and Budgens

- Oil prices fall on surprise US inventory build; equity rally aids

- GLENCORE - S&P cut its outlook for the miner to 'negative'

- RIO TINTO - The miner predicted global iron ore demand will grow by 2 percent a year

- UK SUPERMARKETS - South African billionaire Christo Wiese, who recently bought Virgin Active and New Look, is now training his sights on Britain's struggling supermarket industry

- ARM HOLDINGS - The UK chip designer will collaborate with IBM