Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

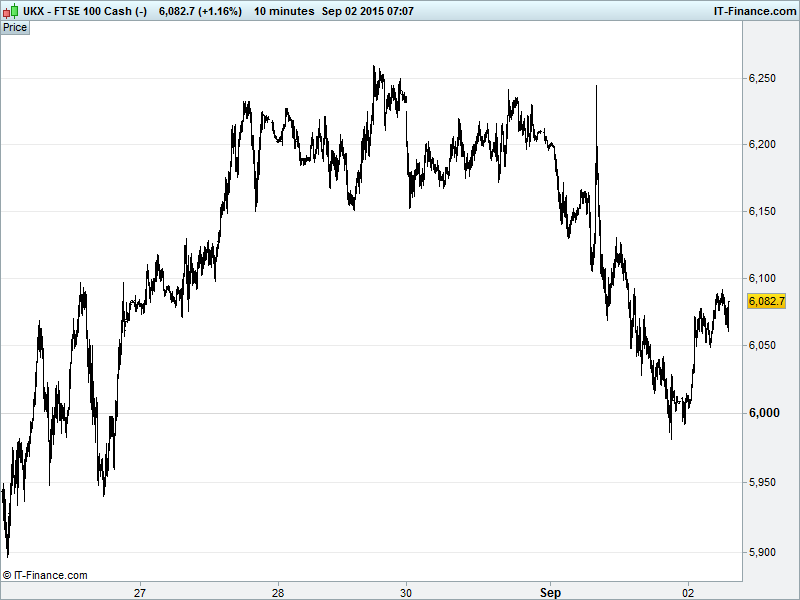

UK 100 Index called to open +15pts at 6075 having found support and bounced from 6000 overnight. Still wrestling with downtrend from early August highs 6775 which leaves 6200 as major hurdle. Note 6150 breached neckline of yesterday’s highlighted H&S top pattern could also become resistance, forcing another move south towards 5800 Aug lows. Watch levels: Bullish 6105, Bearish 6035.

The positive opening call is despite a heavy 3% sell-off by US stocks last night and a rather volatile session in Asia overnight as uncertainty reigns supreme regarding growth in the US and China. This follows disappointing/mixed manufacturing data from both yesterday which sapped risk appetite and saw Oil prices reverse some of their recent rebound on a perceived demand drop, compounded by higher US API Crude stockpile data amid a global supply glut.

Note China equities down but recovering from heavy declines ahead of a 2-day holiday while Morgan Stanley has issued its first ‘full-house’ Buy alert for stocks since early 2009, suggesting the worst may be over for global equities after the recent sell-off. Concerns persist on Greece with creditors expecting delays to inspection of new bailout program after snap elections even if polls suggest Syriza still retains a lead.

Turmoil returned to Wall Street on Tuesday after a short respite, with renewed concerns about China's economy dragging major US indices down nearly 3% and seemingly compounding fears of a long-term selloff. S&P500 now -10% from May all-time highs that themselves topped a 200% recovery after the financial crisis. Some way to go, then, before that index re-visits those levels and we wonder whether the prevailing bearishness of late will continue after Morgan Stanley this morning issued a ‘full house’ buy alert on global equities, effectively calling the bottom of this summer’s equity rout.

The US Fed's Rosengren cited China, Europe and Japanese economic weakness as weighing on US inflation (it’s everyone else’s fault, of course), adding that a persistently missed inflation target makes the case for maintaining US interest rates at a reasonably low level. ‘Reasonably low’ presumably being a bit higher than ‘near zero.’

After US GDP was revised up last week and China data disappointed yesterday along with Canadian GDP, we had Aussie GDP miss overnight suggesting knock-on from China slowdown and commodities price declines. This adds to the muddy picture over global growth and thus monetary policy direction, notably on the other side of the pond. Note also the IMF’s Lagarde warning about financial market volatility and risks spilling over from one economy to the next with China rebalancing, US rates rise, Japan slowing and commodity price falls all representing headwinds.

In focus today we have Eurozone Producer Prices Inflation data which is forecast to highlight continued deflation in July. Then it’s over to the US in the afternoon for ADP Employment Change which is expected to show 200K job adds in August - similar to the expectations for the key US Non-Farm Payrolls update on Friday. While US Non-Farm Productivity is seen improving in Q2, Labour Costs may have declined while Factory Orders may have delivered slower growth in July.

Both WTI ($44) and Brent Crude futures ($48) gave up 2% on Wednesday as the latest weekly US stockpiles report revealed a much bigger than expected increase of 7.6m barrels (analysts had forecast a rise of just 32K). Poor manufacturing data from China and the rubbishing of reports that OPEC is looking to negotiate prices higher by oil bears have brought crude prices back to earth. All oil eyes on more closely watched EIA data later today where consensus is for a 700K barrel increase. If the print misses by anything like as much as yesterday’s, expect some big moves.

Gold ($1140) failed to break resistance $1142 this morning, despite weak performances by Asian, European and US equities with investors preferring to err on the side of caution amid talk of an impending US interest rate rise and accompanying dollar strength. ‘Caution’ this time driving buyers away from the traditional safe haven metal and into others as currency volatility ceases to rock the boat as significantly as it has of late.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – it’s all part of the service.

UK Company Headlines: (Source: Reuters/DJ Newswires/Bloomberg)

- DCC obtains clearance for acquisition of Butagaz

- Ashtead says confident on outlook after Q1 profit rise

- Aggreko acquires Canadian temperature firm ICS Group for £18m

- EMED Mining Public updates on progress towards re – start of its Rio Tinto Copper Project

- Johnson Service sees FY results slightly ahead of market expectations

- Diploma expects full-year revenues to rise about 9%

- Ryanair says August traffic +10%