Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

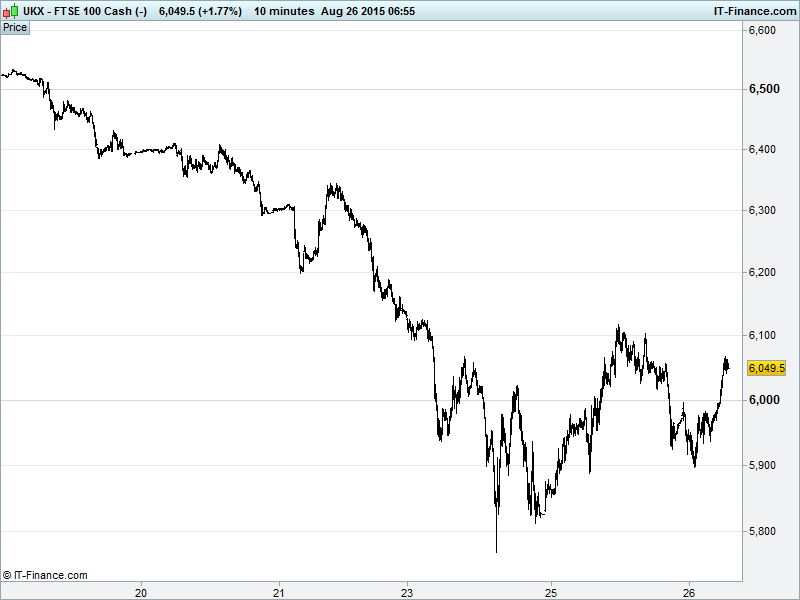

UK 100 Index called to open -60pts at 6020 having made it back above 6000 Tuesday. Daily RSI still indicating upside appetite while we note yesterday's bounce lost considerable momentum at 6100, pulling back 156 pts, and the index remaining under pressure in pre-market futures trading. Bulls looking for 6000 to hold and 2 short hops above 6080 and 6125 while Bears will look to yesterday's bearish looking candle to spook the markets one more time. Watch levels: Bullish 6100, Bearish 5900.

The negative opening call comes as Tuesday’s recovery on bargain hunting consolidated late yesterday with volatility well and truly still alive in the markets this week. This despite what should have been a heart-warming symphony from Beijing as the PBoC announced its latest round of interest rate and reserve requirement ratio (RRR) cuts, which should add much needed liquidity to the markets. And encourage banks to lend lots of money to vulnerable retail investors so they can trade the stock market.

US stocks stayed in positive territory for much of Tuesday, collapsing in the final hour of trading with Dow Jones in particular going from +440pts mid-session to -200pts at close, contributing to a sixth straight day of losses for US markets.

In Fed news, October is now being suggested as the next opportunity to raise US interest rates from record lows. Presumably, we’ll see either the current or some other big picture issue push back lift-off yet again unless the Fed changes the way it assesses the economy’s readiness. You’d need some big cojones to set the rate rise ball rolling right now, but consensus appears to favour getting on with it. Watch this space…

Asian stock markets traded mostly higher overnight in volatile trade as the region digests the PBoC cutting the RRR and benchmark rates. The exception to the rule, of course, being China’s very own Shanghai Composite, currently -3%. Note, of course, lower rates and RRR take effect from today.

With the Greek debt crisis at one stage putting the future of the Euro in doubt, the European single currency looks like it’s providing a port in a storm for haggard investors seeking a safe haven as the USD weakens on doubts that the U.S. Federal Reserve will raise interest rates this year has given the euro a boost, climbing as it has 10% against the global reserve currency since March this year.

In focus today we have US MBA Mortgage applications and Durable Goods Orders coming out at lunchtime while all eyes will surely remain on the tentative situation in the markets as a whole. The only bit of ‘good’ macro-news thus far having been the artificial shoring up of China’s economy by its government.

Gold ($1137) now back in 2-day downtrend following yesterday’s swift move back into equities as bargain hunters showed that appetite for risk was not totally destroyed on Monday. $1140 this morning’s key watch level on the upside while $1130 a target for those pleased with China’s moves to inject liquidity into its stock market.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – it’s all part of the service.

UK Company Headlines: (Source: Reuters/DJ Newswires)

- WPP reports sharp upturn in July trading

- Stagecoach on track to meet expectations for the year

- Carillion says on track to meet full – year expectations

- Gambling firms Betfair and Paddy Power in merger talks

- Paddy Power H1 operating profit up 33% despite new taxes

- Optimal Payments H1 revenue rises 40.2%to $223m

- IGas names Tullow's Julian Tedder as CFO

- Crawshaw appoints Alan Richardson as chief financial officer

- APR Energy first-half revenue falls 52%

- Fastjet signs letter of intent to buy an Airbus A319 aircraft

- Anglo Pacific Group says H1 operating profit doubles