Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

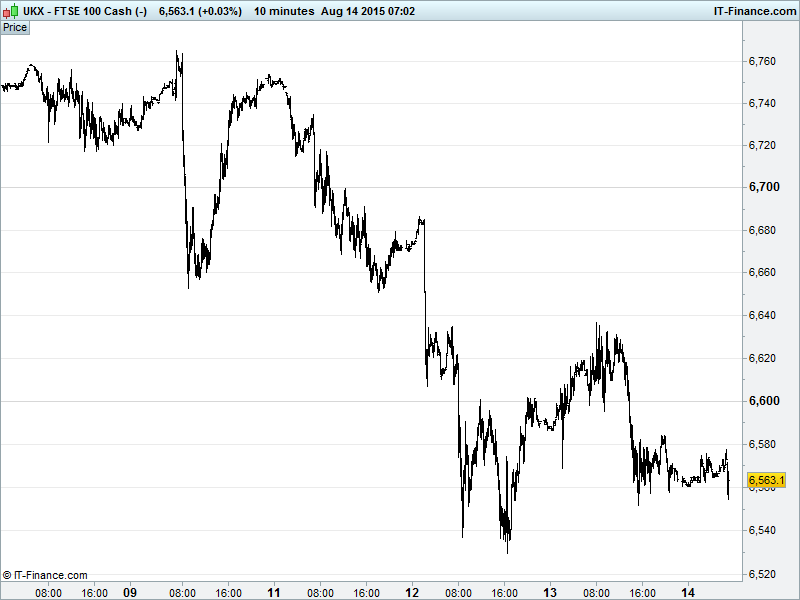

UK 100 Index called to open flat at 6570 with July rising support 6650 still valid, keeping 6-week narrowing pattern alive. However, we’re concerned that yesterday’s bounce failed just shy of 6650, potentially reinforcing the level as support-turned-resistance. Still in downtrend from Monday with possibility of breakdown at 6550 to revisit 9-month rising lows 6500, maybe even July lows 6415. Watch levels: Bullish 6605, Bearish 6540.

The flat opening call comes despite China’s renminbi halting its three day slide, stabilising after PBOC fixed reference FX rate higher for first time since Tuesday’s shock devaluation. This suggests new market-forces based pricing mechanism can indeed work both ways, backing up comments China not simply seeking to aggressively devalue FX to boost exports and counter slowing GDP growth in the world’s #2 economy.

Continued weakness for commodities is hurting sentiment (oil at fresh 6.5yr lows) as is the run-up to the Greek Parliamentary vote on a third bailout, which is to be discussed at Eurogroup meeting of Finance Ministers this afternoon. Germany still making things difficult while IMF still demands debt relief before participating. Note French and German Q2 GDP also disappointed this morning adding to Eurozone woes.

Potential for risk-off into weekend with uncertainty how China FX moves will pan out in the weeks to come as well as whether Greece will get bailout agreed in time or need a bridge loan to pay back ECB by Aug 20. Then there’s the contentious issue of whether US data (inflation especially) is good enough for a September rate rise or external factors such as China’s own FX move will see the Fed hold off.

Asian stocks largely lower overnight after lacklustre cues from the US, as investors weigh up a marginally stronger Chinese currency and oil price declines weigh on Energy-related stocks. Equities in China nonetheless set for best week in nearly two months led by commodities amid speculation of further Yuan weakness.

US stocks little changed Thursday with trading volatile and a widespread reluctance to make significant moves given the sporadic activity earlier in the week. A lacklustre performance came despite macro data showing a rise in US July retail sales which beat expectations, keeping risk-on mentality alive as treasuries hit new lows (yields up on a sub-par US bond auction) while the Atlanta Fed lowered its US Q3 GDP estimate to 0.7% from 0.9%.

In focus today will be Eurozone Q2 GDP after the French and German misses this morning and a likely worsening of the region’s CPI in July. The Greek vote is likely to be a done deal thanks to Pro-European opposition support and any comments from the Eurogroup meeting are likely to, thankfully, come after the close.

Lots more US Data today with slowing Producer Prices likely adding to debate about inflation not being enough to see Fed raise rates next month even if Industrial Production and Uni of Michigan Consumer Confidence are forecast to have improved in July. For Oil traders watch for the Baker Hughes Rig count this evening. More rigs back on-line, accentuating the global production glut?

Brent Crude ($49) settling into a range with boundaries either side of $50 while US Light ($42) sank to a 6.5yr low on rising OPEC output (highest in 3yrs in July) as the US/Saudi game-playing continues. Meanwhile, Goldman Sachs in a 6 Aug report estimated the global supply glut to be currently running at around 2m bpd and that storage facilities will be full by Autumn – this compounded by BP’s refinery in Whiting, Indiana closing 2/3 of capacity for unscheduled damage repairs such that it looks as if Goldman’s prediction could ring true even sooner.

Gold ($1116) peaked around $1125 before pulling back below hitherto rising support yesterday. Bullish traders raced to take profits ahead of more potential US Fed chatter with China’s currency seen to stabilise following this week’s devaluations. Support found around $1113 with the yellow metal still buoyant amid a lack of trust in pretty much everything that’s coming out of the world’s #2 economy this week.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – it’s all part of the service.

UK Company Headlines: (Source: Reuters/DJ Newswires/Bloomberg)

- Glencore exits three mines for $290m

- Lamprell says CEO James Moffat retires

- Highland Gold says total H1 2015 production +1% YoY

- IP Group's portfolio company First Light Fusion completes £22.7m funding round