Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

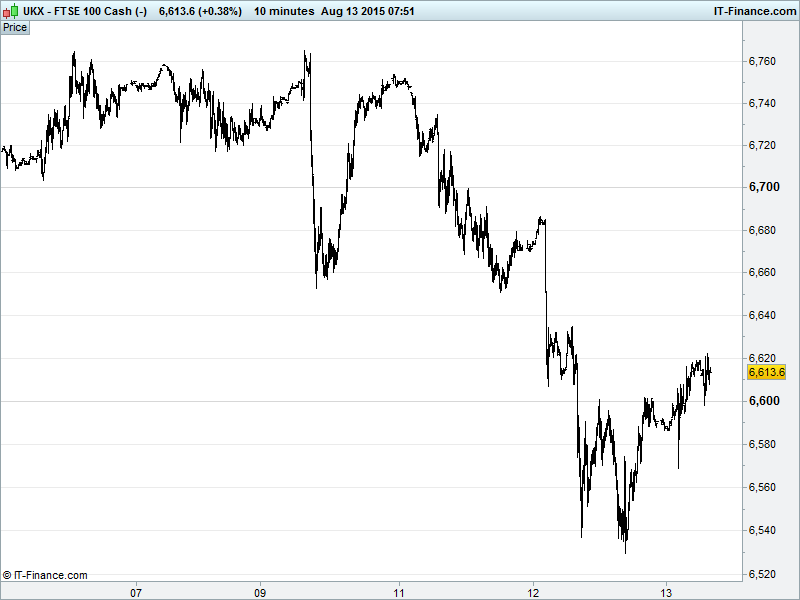

UK 100 Index called to open +45pts at 6615 (despite ex-divs taking off a heavy 35pts) with yesterday’s bounce from support at July rising support 6535 getting back above 6600 this morning. While we point to potential for recovery to recent 6750 highs and ceiling of 6-week narrowing pattern, any downside test of yesterday's lows could see sell-off to longer-term rising lows 6500, possibly even July lows 6415. Watch levels: Bullish 6660, Bearish 6580.

The positive opening call comes despite China’s renminbi currency fixing lower for a third day, with relief from declines having slowed, the overnight PBOC briefing emphasising no desire for persistent depreciation (10%?) as well as the intention to intervene when things ‘distorted’, effectively managing any devaluation. In other words, market forces more involved, but still on our terms.

Asian stocks largely higher, benefiting from US stocks rallying to close flat and traders reacting positively to Chinese central bank comments overnight, taking recent change in currency mechanism as a sign of a move towards market-based pricing and a step towards an improved profile for inclusion in IMF basket rather than revival of currency war in response to poor growth outlook.

Note uncertainty still rife about whether China’s move (or indeed US inflation data) scares the Fed from a September rate hike which gave Commodities some support at depressed lows thanks to a USD sell-off which has since seen a bounce. Germany (as usual) doing its best to pour cold water on Greek bailout deal, still wanting more concessions and commitment. The deal is being discussed in Athenian Parliament now, with approval needed promptly by Eurozone peers (especially Germany) to ensure funds in place to pay ECB next week. Note Debt relief still key and IMF involvement unsure.

U.S. stocks on Wall St. staged an afternoon rally, recovering from a second day of heavy losses following China’s currency devaluation games, while Dow Jones futures are maintaining the uptrend from yesterday afternoon’s lows 17125 this morning as hope prevails that initial volatility in the currency markets is subsiding. US markets also benefitting from a respite in commodity price pullbacks that helped resource based companies.

Stateside earnings were mixed on Wednesday with Macy’s (M) suffering from a strong USD that weighed on tourist spending and port delays that stung operations. Network equipment maker Cisco Systems (CSCO) reported higher than expected quarterly revenue and profit as strong US demand offset weakness elsewhere, while News Corp (NWSA) EPS beat expectations with revenue falling short.

In focus today will be Final July CPI figures for France and Spain following those of Germany this morning (inflation still very much missing in action). Greek Q2 GDP sure to show worsening contraction while US Retail Sales are forecast to have rebound in July with Business Inventories growth unchanged.

Gold ($1121) found support at $1120 within a rising channel as the yellow metal makes a brave escape attempt from those 5yr lows. Fears of a currency war adding shine to gold as an alternative currency that has no government to meddle in its value.

Crude prices still languishing near 2015 lows, Brent ($50) having now filled a 3 Feb gap and US Light ($44) doing nothing of interest this morning(!). This comes after US stockpiles were seen to have fallen, but at a slowing rate which rekindled those supply glut fears with gutsy US producers fronting up to Saudi led OPEC in what seems to be a game of chicken. Who’ll buckle first?

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – it’s all part of the service.

UK Company Headlines: (Source: Reuters/DJ Newswires)

- Derwent London's H1 net rental income up 5% to £66.9m

- Michael Page to pay special dividend after strong growth

- Cineworld says film release programme for H2 is encouraging

- Glencore cuts FY industrial capex ceiling to $6b, H1 copper production down 3%

- Glencore posts 3% fall in H1 copper output, cuts capex

- Independent Oil and Gas updates on its Skipper asset and funding plans

- Nomad Foods to acquire continental European Findus Group businesses

- IGas Energy comments on onshore oil and gas exploration timetable

- Ophir Energy H1 pretax loss narrows to $123.3m

- Grainger says acquired 929 tenanted PRS units since the start of yr

- Drinks bottler Coke HBC sales up slightly

- Ithaca Energy says FY production guidance remains unchanged at 12,000 boepd

- BHP says iron ore operations disrupted by Tianjin port blasts

- Tui Profit Rises Despite Tunisia, Greece Impact