Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

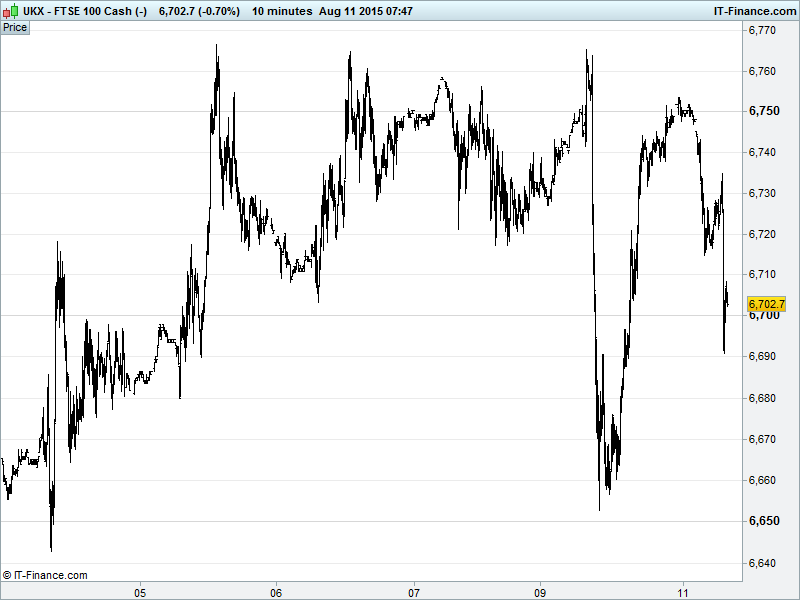

UK 100 Index called to open -30pts at 6705, with yet another sell-off from 6750 overnight serving to reinforce the level as bugbear resistance due to seemingly impenetrable trend-line of falling highs from June 4 and 200-day moving average just above. This maintains 2-month downtrend and increases likelihood of correction back to longer-term 10-month rising support at 6500 from whence we recently bounced. Watch levels: Bullish 6770, Bearish 6645.

The negative opening call comes despite news of Greek #3 bailout talks having completed and a deal (possibly higher than €86bn) within reach and only a few small details pending (incl. fiscal outlook, size). Scepticism (we call it realism) has us point to bailout history confirming that it takes but one small detail to scupper a deal.

Furthermore, after awful weekend Trade data the PBOC looks to be admitting that China growth picture not as rosy as it would like us to believe, taking extreme stimulus step of allowing Yuan to devalue almost 2% - the most in 20 years - to help exports and combat the inevitable growth slowdown. The move has rippled across Asian markets (equities and FX).

Asian stocks mixed overnight, despite positive US close, with Chinese stocks making 2-week highs after the Yuan devaluation and Hong Kong equities benefiting from the knock-on. Other regional markets suffering from USD rally reaction to China FX move, negating some of yesterday’s support for commodities (Copper, Oil, Gold) and denting raw material rebound.

US futures off their overnight highs this morning following some good gains on Wall St. yesterday - partly due to bargain hunting after last week’s downtrend but markets also benefitting from renewed optimism on Greek bailout negotiations which appear to be at or near their conclusion.

Plenty of US Fed chat with vice chair Fischer telling it like it is - that the US is in a situation of nearly full employment but very low inflation while Lockhart refrained this time from direct reference to a September (while maintaining a 1st rate rise is close) in contrast to last week’s untowardly hawkish comments.

More fallout from last week’s ‘Super Thursday’ saw BoE policy maker Miles said he had seen a reasonable case to vote for higher UK interest rates last week but did not find the arguments conclusive.

Stateside earnings season saw (Warren Buffet’s recent joint project with Brazilian private equity firm 3G) Kraft Heinz disappoint (Kraft profits up while Heinz made a loss) as the newly merged company gave its last set of results as two separate entities. No additional outlook given and no conference call held. Knock-on potential for EU stock Nestle which reports on Thursday, given similar happenings in the media sector earlier this week.

Elsewhere, a radical shakeup of Google’s structure saw it rebrand itself as new holding company ‘Alphabet’ whose largest subsidiary would be Google. Shares in the tech behemoth went up 5% in after-hours trading.

In focus today will be ZEW Survey results for Germany and the Eurozone, with consensus looking for the former to register small improvements for both the Current Situation and Expectations elements in August, taking them off 2015 lows. Note the Eurozone figure remains in a downtrend since April.

In the afternoon, US NFIB Small Business Optimism for July is forecast to rise slightly from June’s 15-month low following a sharp drop back from 2015 highs. Thereafter, consensus hopes for US Non-Farm Productivity to bounce back in Q2 although Unit Labour Costs may only register flat. To close the day, US Wholesale Inventories are seen growing slower in Jun, but sales accelerating.

Gold ($1099) made a breakout attempt from the narrowing channel that has imprisoned it near 5yr lows for the past 3-weeks, with a rough bearish double top pattern and buyers’ remorse quickly recapturing the yellow metal. Still testing that channel ceiling, however, as the USD basket battles resistance 97.8. Support at rising lows has the potential to decisively propel gold up above $1105 with sentiment appearing to be turning bullish on hitherto depressed commodities. Bargain hunting?

Crude prices made a small bounce with Brent ($50) having finally filled a 3 Feb gap and US Light ($45) bouncing near 12-month lows. Bullish bets likely supporting prices somewhat but there is still some work to be done before a bottom can officially be called – pressure remaining in the form of increasing oversupply with Iranian oil awaiting the go ahead to enter the market, not to mention US production seeing an opportunity to hammer the (evidently weakening) Saudis.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – it’s all part of the service.

UK Company Headlines: (Source: Reuters/DJ Newswires/Bloomberg)

- Ladbrokes first-half profit -44%

- Just Retirement agrees all – share deal with Partnership Assurance

- Serco maintains profit guidance, trading better than expected

- Game Digital reports lower hardware revenue in H2

- Gloo Networks to start trading on London's AIM

- John Wood Group awarded 3 year blanket order in Gulf of Mexico

- Johnston Press H1 underlying revenue £128.9m vs £135.1m

- SIG says H1 sales from Continuing Operations -2.7 pct

- Exillon says July avg daily production was 15,732 bbl/day

- YouGov says FY trading is in line with its expectations

- Eurasia Mining Starts Drilling at Monchetundra Platinum Project

- Card Factory Retains FY Expectations As 1H Revenue Grows

- Carillion JV Named Preferred Bidder on Midland Metropolitan Hospital Job

- Partnership Assurance 1H Profit Drops

- Synthomer Raises Dividend As 1H Profitability Improves