Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

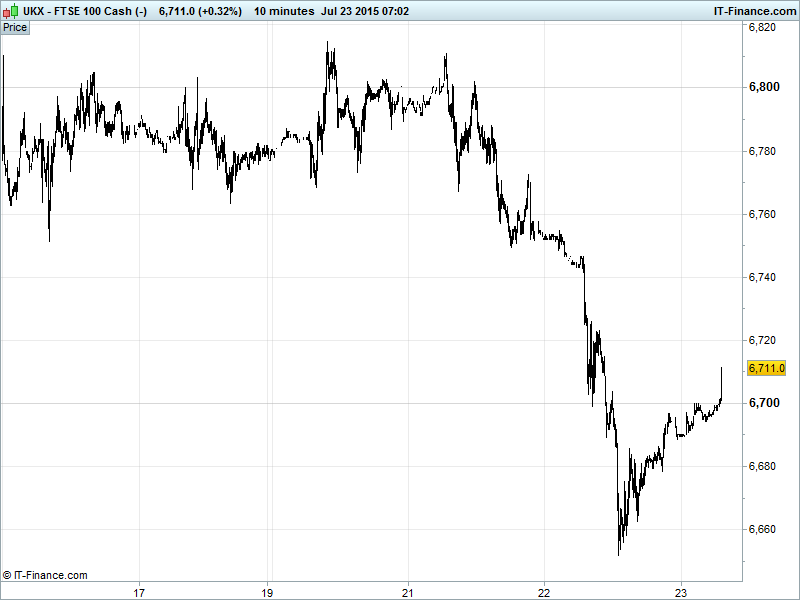

UK 100 Index called to open +40pts at 6705, having bounced from 6650 support and breaking back above the 6700 level and the falling resistance from Tues highs 6810. Strong possibility pullback served as digestion of recent rally from 6400, with another 350pt gains taking us back to 7000 from whence we fell in late May. Note 200-day moving average 6750 could be hindrance near-term. Updated Watch levels: Bullish 6725, Bearish 6685.

The positive opening call comes despite a continued commodities rout as Greek worries further recede thanks to lawmakers in Athens approving the second round of reforms necessary to complete negotiations on a third bailout. While the vote sailed through thanks to opposition support, the PM Tsipras suffered persistent dissent meaning snap elections a real possibility.

US markets closed in the red as disappointing corporate results from Apple and Microsoft weighed along with more commodity price declines (supply glut, demand concerns) and despite strong US housing data and solid reports from Boeing and Coca. The Nasdaq understandably underperformed after technology company results failed to inspire (note Apple cut CAPEX by $1bn).

Asian bourses had a mixed session, again following a weak lead from Wall St, with Nasdaq the main underperformer given Apple’s disappointingly record-breaking Q2 results (results beat, but the outlook for the remainder of 2015 and lower iPhone sales sent investors packing).

Japan’s Nikkei225 edged up 0.4% while the Shanghai Composite is on a strong front foot this morning, a rally that would be impressive if it wasn’t fully engineered by the People’s Government after it effectively outlawed falling equity prices. Madness, but watch for potential stabilisation of commodity prices as a result (with one eye firmly planted on the USD…).

Aussie business confidence is looking up for Q3 after the most recent print came out at 4, up from last quarter’s 0. The reading’s been in decline since late 2013 and the beginning of the downturn in commodities on which the Aussie economy depends so heavily. Those two 2015 rate cuts by the RBA finally starting to take effect? Note also the Aussie government toned down austerity in its last budget statement.

For those watching the banks, Credit Suisse (CSGN) this morning beat Q2 forecasts and confirmed full year targets ahead of a major shake-up by well-respected new CEO Tidjane Thiam who jumped ship from the UK’s Prudential (PRU).

In focus today will be UK June Retail Sales, expected to ring up an acceleration in growth while UK BBA Home Loans are also seen higher supporting consumer confidence and a still buoyant housing market, even if BoE Governor Carney is hinting at an impending rate rise from historic lows.

In the afternoon, the Chicago and Kansas City Fed Indices are seen improving in June but remaining just negative, while US Jobless Claims are forecast almost unchanged along with Eurozone Consumer Confidence. Growth in the US leading Index is expected to have slowed.

Results-wise, the plethora of US corporate updates continues with updates from Amazon (AMZN), AT&T (T), Caterpillar (CAT), Dow Chemical (DOW), General Motors (GM), Kimberly-Clark (KMB), McDonalds (MCD), Starbucks (SBUX) and Visa (V) with all eyes on the impact of a stronger USD and the outlook for the rest of 2015.

Crude Oil still under pressure with US Light back below $50 (currently $49) and Brent at support $56. Note the US Dollar Basket found support around 97.5 while the July uptrend remains in play, a worry for commodities as a whole and likely to trump a Chinese market recovery in the end.

Gold ($1098) recovering after bouncing off $1087 yesterday, though still failing to outshine falling highs since 19 July. Watch for more downside if the Dollar basket recovers back towards 98 and above.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – it’s all part of the service.

UK Company Headlines: (Source: Reuters/DJ Newswires/Bloomberg)

- SABMiller quarterly sales rise on Latin American, African demand

- Unilever's second – quarter sales top estimates

- Sales growth picks up at Britain's Kingfisher

- Premier Foods sees Q1 sales fall

- Mothercare posts first – quarter UK sales rise

- Howden Joinery says well placed to achieve its FY expectations

- De La Rue says FY overall expectations remain unchanged

- Alliance Trust actively engaged in addressing shareholders' concern, anticipates changes in fall

- Thorntons says requested cancellation of listing on LSE

- Daily Mail lowers guidance as advertising markets deteriorate

- TSB Banking Group reports fall in first – half profit

- Aberdeen Asset Management sees $15 bln in Q3 net outflows

- Britvic to raise about 90 mln stg via share issue

- SSE expects dip in profits from supplying energy this year

- RBS to sell loans to Deutsche Bank, Apollo in 400 mln stg deal

- Electrocomponents' Q1 underlying sales growth increased to 5 pct