Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

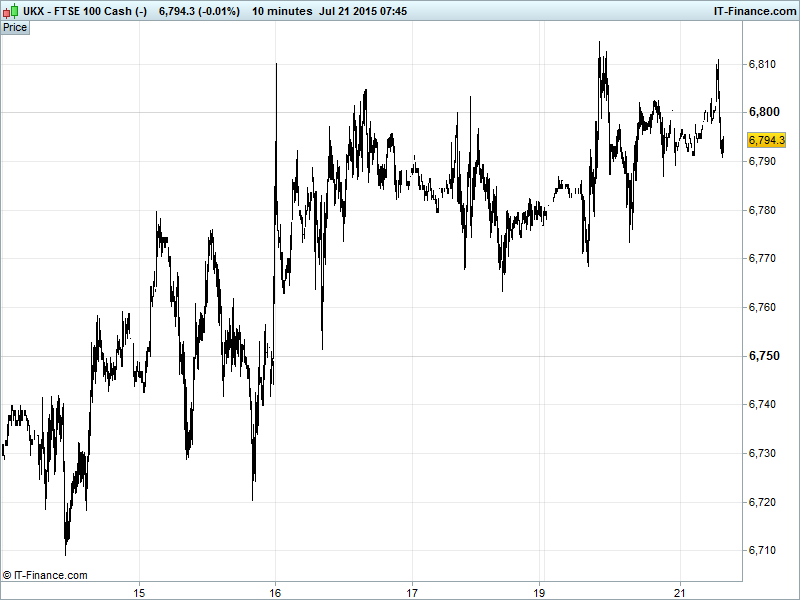

UK 100 Index called to open +5pts at 6795, still struggling to stay above 6800 but persistence suggesting appetite to better the level and revisit highs of 7000, giving the recent strong bounce from 6415 lows and 9-month rising support a second wind after a 3-session pause Updated Watch levels: Bullish 6820, Bearish 6780.

The positive opening call comes thanks to Asian bourses outperforming modest gains by US counterparts thanks to Greece debt crisis fears easing (banks open, ECB & IMF been repaid), a thus far positive earnings season, a regaining of poise by Chinese equities and a combined lower oil price and FX weakness (from strong USD) boosting exporters and travel stocks.

US markets posted small gains amid choppy trading, extending a 2-week rally, as a solid results season, M&A and fading Greek concerns allowed investors stay bullish despite commodities (precious metals, oil) falling close to their lowest levels since 2002 hindered by a USD which is underpinned by renewed focus on lift-off timing and trajectory for US borrowing costs after the Fed’s Bullard said there was a fence-sitting 50% chance of a September rate hike.

S&P500 little changed after briefly challenging its previous record close (fresh Nasdaq record) thanks to forecast-beating Q2 corporate results (Halliburton, Morgan Stanley, Lockheed Martin) offsetting drops by commodities producers. Note, however, shares in IBM -4.4% after hours as profits fell 17% and year-on-year revenue declines missed consensus and extended their run to 13 straight quarters.

Note research from Goldman Sachs suggesting buying European equities against selling US stocks while the US Federal Reserve has confirmed capital surcharges for the 8 largest US banks posing systemic risk with JPMorgan (JPM) the only one with a shortfall ($12bn).

Asian bourses trended mainly higher overnight, following Wall St’s cues as tech stocks bolstered US markets ahead of Apple and Microsoft corporate earnings reports. Positive performances also came despite commodities taking a hammering over the past 48 hours – notably the Aussie ASX preferring to absorb the RBA decision to keep interest rates unchanged for the foreseeable future. No policy easing imminent but pressure continues to ramp up on the Aussie Dollar with further depreciation deemed necessary (and likely) in order to secure balanced economic growth.

Japan’s Nikkei 225 still on the front foot with a weak Yen and confident tones from the BoJ which maintains the Japanese economic recovery is still on track with inflation inching upwards (along a knife edge, it seems).

Chinese foreign direct investment slowed sharply in June (+0.7% compared with +7.8% in May) as markets there traded without much direction overnight. Note converging highs and lows through July on the Shanghai Composite – more downside potential as trading suspensions get lifted? Chinese markets difficult to gauge of late since it’s not clear whether index moves are reflecting retail buyers or government intervention.

In focus today, amid another dearth of market moving macro data, will be results from Apple (AAPL) with all eyes on how the new watches are selling and how the key Chinese market is holding up. Microsoft (MSFT) will be of interest given IBM’s mixed card while Yahoo! (YHOO) may be forced to focus on a slowing core business post the Alibaba IPO. Bank of New York Mellon (BK) closes the season for the banks.

Crude prices have now broken below respective support levels with US light ($50.2) recovering back above $50 after dipping below overnight and Brent ($56) bowing to pressure from global supply glut worries and transfer of interest to corporate earnings season – from the macro to the micro.

Gold ($1104) attempting further gains after yesterday’s torrid session but still suffering falling highs and unlikely to do well going forward with equities benefitting from hopes of good earnings reports, a more risk-on mentality as Greek banks re-open and a dearth of macro data. Bulls nonetheless will look to $1110 today while bears will eye a continuation pattern and subsequent break down below $1100.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – it’s all part of the service.

UK Company Headlines: (Source: Reuters/DJ Newswires/Bloomberg)

- Cable & Wireless Comms says on track with first – quarter growth

- Oxford Nanopore raises £70m via placing

- PZ Cussons says performance since year – end in line with expectations

- IG Group full – year profit falls hurt by Swiss franc fluctuations

- IG Group says CEO Tim Howkins to retire

- Royal Mail keeps costs in focus after flat first quarter

- AO World Q1 UK revenue growth 6.5%

- Russia's Petropavlovsk on track to reach 2015 output capacity

- Galliford Try signs £46m contracts with Birmingham City University