Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

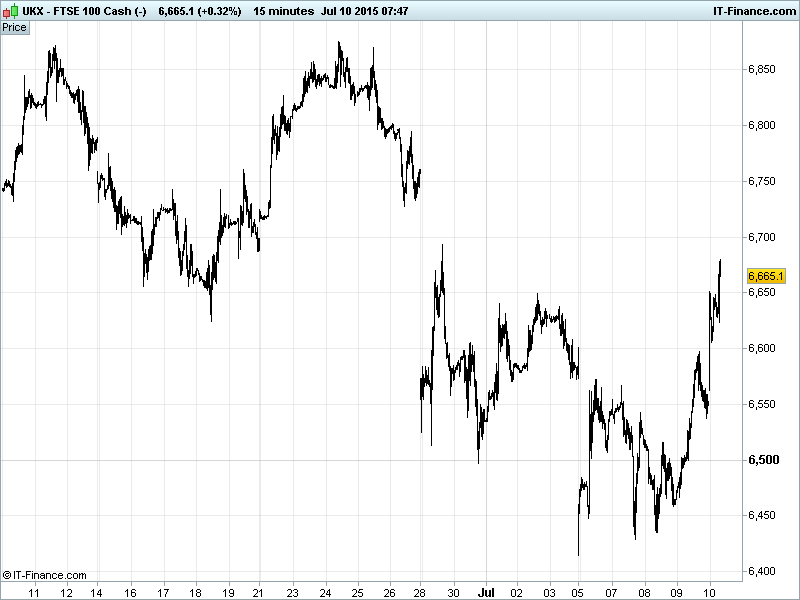

UK 100 Index called to open +85pts at 6665, with strong overnight gains allowing July 6650 highs to be revisited. The bounce maintains recovery from 6400 5.5-month lows and keeps alive the longer term uptrend from October. It also increases the chances of the end-Jun 6700-6720 gap being filled. However, this does correspond with falling resistance from end-May. Updated watch levels: Bullish 6705, Bearish 6590.

The positive opening call comes courtesy of heightened optimism of avoiding a Greek tragedy after its government presented late last night (on time) a reforms package worth circa €12-13bn, which is significantly more than previous commitments, much closer to creditor demands and could be enough to secure a €53bn bailout from neighbours by Sunday and stay within the single currency Eurozone.

Furthermore there are signs that Germany is bowing to international pressure (US, China, IMF) and softening its stance on Greek debt relief rather than pure debt restructuring for the troubled nation. This could be a big step in terms of providing the country with some room to begin a genuine recovery rather than finding itself back in the current bailout needing situation in another few years.

Note further recovery by Chinese equities helping boost overnight sentiment in Asia (even if half of stocks remain suspended) as the benchmark delivers its biggest two day gain since 2008 thanks to inordinate government and regulatory intervention aimed at offsetting what has become an equity market rout following a bubble bust. Keep an eye on the hitherto battered Mining Sector which could benefit.

US markets closed just higher, helped by China’s gains yesterday, rising optimism on Greece and oil snapping a 5-day losing streak on receding fears of increased Iranian supply. Fed comments were mixed with Evans saying he’d like to wait until mid-2016 and needs much convincing on anything earlier while George said should move modestly now, more risky to wait and shouldn’t fall into trap of waiting for more data. Nicely balanced rhetoric from the pair.

Asian markets higher across the board on market confidence in a thus far effective host of measures to stall a cascading selloff in the Chinese markets, not to mention Greece hopes, of course.

China’s Shanghai Composite continues to correct to the upside this morning after notching up its best session since 2009 overnight as those aforementioned brash stalling measures (forcing major shareholders to stop selling and start buying; allowing central bank funds to be used to buy shares; suspending more than 1400 stocks from trading) remain effective. Scary stuff, both for investors locked out of the markets and those in it with volatile trading into Friday’s session.

Hong Kong’s Hang Seng index also continuing to recover (+2% this morning following near 4% gains yesterday) after posting its steepest decline in seven years on Wednesday (-5.8%), when investors banished from mainland markets sold Hong Kong stocks to raise capital.

Japan’s Nikkei tracking pan-Asian optimism while Australia’s ASX ticking up with an overnight commodities bounce on a now downwards trending US Dollar Basket benefitting market barometers BHP Billiton (BLT) and Rio Tinto (RIO) while energy stocks carried the index higher on a 3% oil price rise.

In focus today will be any commentary on the Greek proposal. Good enough? Any sticking points? Hopefully not as time is running out. Thereafter macro data is thin on the ground bar the UK’s May Trade Deficit at 9.30am (consensus has it widening) and US Wholesale Sales and Inventory data with growth expected in May, but slowing from April. Note the Fed Chair Yellen speaking after the European close.

Talking all things oily, crude prices now nearly positive for the week following those 3% gains as the slippery substance settles into an uptrend supported by rising lows from Wednesday, propelled further by a softer USD and seeming confidence that an Iran nuclear deal remains further off than previously imagined. Current levels: WTI $54, Brent $59.

Gold volatile but outperforming into the weekend, well off Wednesday’s 4 month lows amid wider improvements in commodity prices though seemingly following market confidence higher, with a firmer Euro and weaker Dollar providing support rather than all-out fear & loathing. Currently $1162.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – it’s all part of the service.

UK Company Headlines: (Source: Reuters/DJ Newswires/Bloomberg)

- Alliance Pharma appoints Andrew Franklin as finance director

- Smith & Nephew buys Russian manufacturing business

- Petrofac gets $780 million project in Kuwait

- IHG agrees $938 sale of InterContinental Hong Kong

- French Connection says FD Castleton to step down

- Dragon Oil eyes 15 pct production growth in 2015