Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

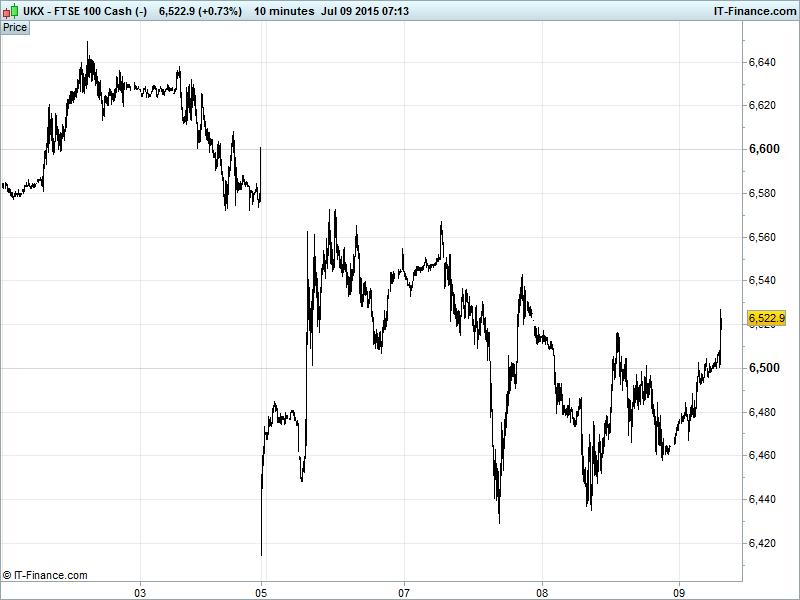

UK 100 Index called to open +20pts at 6510, with overnight gains delivering a breakout above 6500 and beyond the trend of falling highs from 25 June. This move, along with rising lows from 5 July, keeps the longer term uptrend from October alive (just). Bulls glad to see breakout but Bears still point to downtrend from late May. Watch levels: Bullish 6560, Bearish 6440.

Thursday’s positive opening call comes after sanguine US Fed minutes overnight all but reassured markets that a US interest rate rise won’t be coming this year, citing external, all eclipsing drivers Greece and China as ongoing cause for concern. Hopes of an imminent, amenable end to Greek bailout talks came as both the Fed’s Jack Lew and IMF’s Christine Lagarde consolidated their stance backing debt restructuring for Athens as, finally, the fact that Greek debt is not sustainable in its current form starts to hammer itself home and put the proverbial cat amongst the creditors.

PM Tsipras faces what is arguably his toughest day yet since storming to power, finalising as he must yet another new set of proposals for ‘tough economic reforms’ to present to creditors to unlock the opportunity to negotiate a new bailout program and secure his country’s place in the Eurozone.

Greek banks will remain closed until Monday next week, with a €1000 limit on the amount of cash foreign travellers can take out of the country hopefully tiding the banks over until much needed ELA can be released (hopefully), allowing them to re-open on the 13th.

US bourses closed with losses on Wednesday, although this was due to a technical glitch that saw trading suspended on the NYSE for over 3 hours with concerns of a cyber-attack (denied by the exchange) spooking the markets. Q2 earnings season kicked off stateside after-market with aluminium producer Alcoa posting mixed (read disappointing) results amid a commodity price slump and China slowdown.

Asian markets positive, after some volatility and despite the US closing lower, with traders optimistic on Greece getting a positive outcome to its bailout negotiation fiasco after the US and IMF ramped up pressure on Europe to avoid Grexit and talked of debt restructuring. Markets also happy to see some stabilisation in China as trading resumes and inflation data encouraged.

China bouncing back as continued government and regulator intervention to abate the bubble bust sell-off begins to take effect. Commodity related stocks, having been worst hit, lead the gains despite US major Alcoa reporting lower than expected Q2 results on lower aluminium prices. Hong Kong following mainland China higher.

Japan’s Nikkei higher thanks to the China rebound, but hindered by a stronger JPY after the Fed warned on external factors (China, Greece) and members remained divided about a US rate rise, thus taking the USD further back from July’s 6-week highs. Note Australia’s ASX just positive, hindered by weak commodities prices and a stronger AUD following the Fed minutes and better than expected employment data downunder.

Speeches are once again the pick of the day’s events with the ECB’s Noyer speaking at 9.30am and a joint performance by the German and French Fin Mins at 1.30pm. Other than that we’ve got the BoE’s interest rate announcement at 12pm which would be interesting were it not for the fact that rates are sure to remain at 0.5%. US jobless claims data rounds off the day at 1.30pm, looking for an improvement. As always, see the live Macro-Calendar for a full rundown.

Gold continues to bounce from 3.5-month lows, helped by Fed minutes weakening the USD. Still demand for the safehaven dampened by poor 2015 performance and the trend of falling highs from mid-June remains a hurdle at $1165.

Oil prices recovered throughout Wednesday as the US Dollar weakened on largely dovish Fed rhetoric, yet failed to punch through resistance ($53 for WTI, $58 for Brent) as Iran nuclear talks continue and a veritably ‘risk-on’ (Greece, China uncertainty) environment envelops the commodity markets in general. Current levels: WTI $52.7, Brent $57.9.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – it’s all part of the service.

UK Company Headlines: (Source: Reuters/DJ Newswires)

- Primark owner AB Foods maintains year guidance

- Spirent Communications's H1 revenue $218 mln vs $221 mln

- Balfour Beatty issues fresh profit warning, faces likely loss

- Fund manager Ashmore sheds $2.2 bln in assets in Q4

- Hays posts 9 percent rise in fourth – quarter net fees

- Builder Barratt sees better – than – expected profit in strong market

- Go-Ahead today announces that Keith Down, Group Finance Director, will be leaving

- Gulf Keystone Petroleum says output at both Shaikan facilities stable

- Plus500 says still facing regulatory scrutiny

- British fashion chain SuperGroup makes move into China