Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

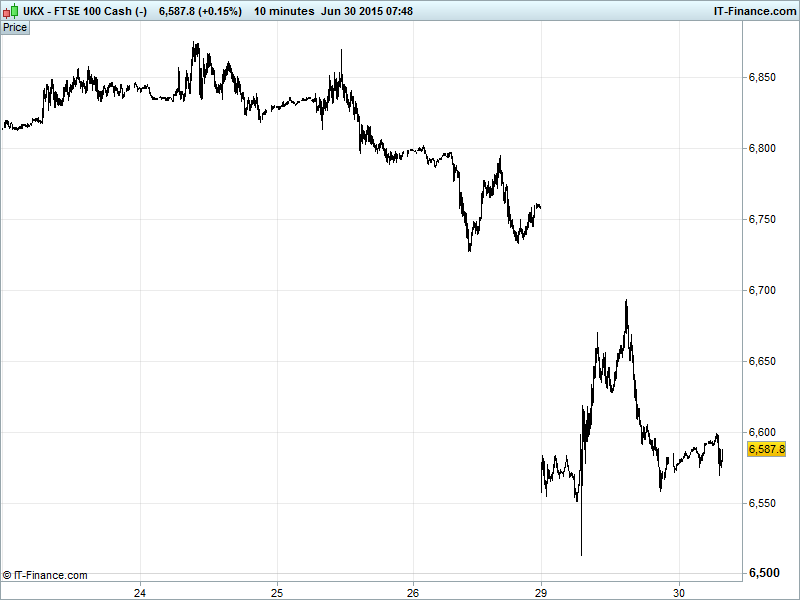

UK 100 Index called to open -45pts at 6585, still under pressure with an overnight bounce failing at 6000. Yesterday saw bullish appetite attempt to close the 200pt gap to 5-month lows, getting as high as 6695 by mid-afternoon, but gains had all but evaporated by the US close. Inability to hold above 6630 June 18 lows maintains downtrend from end-May. Watch levels: Bullish 6610, Bearish 6540

Another negative opening call comes after a volatile day with US stocks posting heavy losses - S&P500 suffering its worst day so far in 2015 – and China’s Shanghai composite attempting overnight to climb up the cliff it fell off last week as market concerns over Greece, whose credit rating was sent one notch further into junk territory by S&P (now CCC-, CCC previously), continue to take centre stage.

With Greece about to default on its IMF loans today and the probability of a Grexit now set at 50% (scary…!), Greek PM Tsipras remained standoffish, suggesting that, a) the EU will not eject Greece and b) the country will survive even if there is no further bailout program. He added that Grexit is an unfavourable outcome for all parties – Creditors included.

Elsewhere, the ECB’s Nowotny said the European Central Bank (ECB) needs to make a decision on whether or not to support Greece's banks through this week in the run-up to Sunday’s planned referendum on bailout conditions. Another ECB official (Coeure) said that while no-one wants an exit from the single currency for Greece, such an eventuality can no longer be ruled out.

Asian markets are posting gains, shrugging off Greek referendum news uncertainty which lead to losses for EU and US bourses and a $1.5tn rout for Global equities yesterday and resulted in ratings agency S&P further downgrading the beleaguered nation’s debt (default possible within 6 months).

As we move into Grefault Tuesday (inability to repay IMF debt, existing bailout expires) uncertainty reigns supreme regarding a Grexit scenario with the nation technically without a safety net from tonight for the first time in 5yrs, the state coffers dry, capital controls in place and banks closed. PM Tsipras as optimistic as ever (‘Europe doesn’t want Grexit’), while Europe says it’s up to Greece.

Shanghai composite reversing 3-day slide and still volatile as Beijing steps up efforts to right the ship of artificially inflated sentiment and help markets out of bear market territory. Traders weighing up what else the government might throw at markets (stimulus? halt IPOs?) to stem deflation of margin trading fuelled China equity bubble.

Japan’s Nikkei in the green despite news from Sony that it needs to raise $3.6bn via sales of shares and convertible bonds to finance production of image sensors for smartphones. Macro data from Japan mixed overnight, with slightly worse than expected Wages and Housing Starts.

Today’s macro-data, for what it’s worth, sees UK GDP at 0930, Eurozone unemployment rate at 1000 and US Chicago PMI & consumer confidence this afternoon. All looking mixed, all likely to be ignored. Check the live Macro-Calendar for a full rundown.

Gold’s rebound was short-lived, with gains to $1188 having now evaporated to $1175 which was a supportive level yesterday. The USD and JPY are benefiting more as a safehaven, with strength in the former making dollar denominated precious metal more expensive, in a relative sense, despite macro uncertainty.

Crude prices failed so far to completely fill the gaps they left yesterday morning and remain under pressure today as confidence prevails that, despite missing its own self-imposed deadline, Iran is nonetheless on course to strike a deal with US and European diplomats on its nuclear programme in the coming days, this likely flooding the market with Iranian oil and driving prices lower again. Brent treading water in anticipation at $62 while WTI doing similar at $58.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – it’s all part of the service.

UK Company Headlines: (Source: Reuters/DJ Newswires)

- Northgate FY profit rises

- Kier Group says talks ongoing for sale of mining ops at Greenburn

- Galliford Try JV sings development deal for major housing project

- Ocado reiterates target of international deal in 2015

- Eurasia Drilling says extends deadline for Schlumberger merger

- Fastjet launches new route to Malawi

- Plus500 says 13,499 UK customers' balances unfrozen

- Rio Tinto aluminium smelter in New Zealand faces possible power crunch