Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

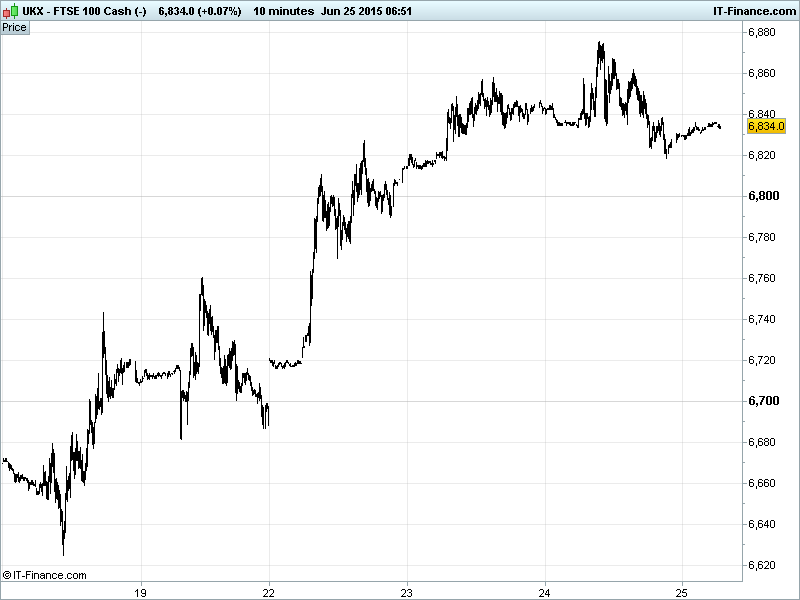

UK 100 Index called to open -20pts at 6825, maintaining the 5-session uptrend from 4-month lows and holding on to 200pt gains from the rebound. The sideways move of the last two days suggest the index still catching its breath (consolidation after quick gains) before deciding which direction to take. Another leg higher towards 7000? Or a retrace towards 6750? Updated watch levels: Bullish 6880, Bearish 6795.

The negative opening call comes amid a return to acrimony in Greek bailout talks with rejection of proposals being passed between the two camps like a proverbial football as both sides entrench themselves ahead of an important (to say the least) end-June ‘deal or default’ deadline. Tsipras and creditors are expected to meet this morning to try to formulate an agreement ahead of midday’s Eurozone finance ministers’ summit.

Aggressive language has started to be used by Greek officials with words such as ‘Armageddon’ and ‘annihilation’ being bandied around while the IMF’s Lagarde continues (rightly so) to lambast Athenian attempts to promote a reform package based on promises of ‘improved tax collection’ – five years of failure to do so is, as pointed out yesterday, pretty much the reason we’re in this situation in the first place.

Bargaining room is shrinking for the embattled Tsipras & Co. whose anaemic banking system relies absolutely on vital ELA funding from an ECB which is sure to turn the liquidity taps off in the event of a national default and exit from the common currency.

US markets had a bad day Wednesday (Dow Jones down 1%) in reaction to the latest breakdown in Greek negotiations while investors kept one eye on the Fed – Goldman Sachs’s Cohn piping to suggest the markets are not ready for a rate hike, a view continuing to be supported by macro-data, and indicating he would not be surprised to see some ‘interesting market reactions based on official change in rate policy.’

Asian equities echo mild losses in EU and US as Greece edges closer to a month-end default with bailout/aid talks (now a very high stakes game of chicken/pass the parcel blame) again failing to deliver the ‘staff-level agreement’ markets are pining after. After all the hype, a flurry of meetings late into the night produced continued standoff between Athens and its creditors, the former as stubborn as ever on what reforms are acceptable back home and the latter sitting tight on what will satisfy them enough to release the much needed funds.

The mud-slinging has resumed with Syriza talking of 'blackmail' by creditors all the while Greece's banking system sits on frozen water marginally thicker than paper as cash withdrawals continue to erode its capital base leaving PM Tsipras with few options to avoid collapse as the clock ticks. More talks today.

Japan's Nikkei is retreating on 4-day gains to an 18yr highs as Greek worries dominate investor sentiment round the world and a weaker USD (rate hike comments offset upward revisions to Q1 US GDP) saw a stronger JPY hurt exporters. While Greece takes centre stage, comments from activist investor Carl Icahn (he who regularly pressures of Apple) are also weighing after he suggested the market is extremely overheated, like in 2007.

China equities back in the red, likely hindered by reports that the PBOC is unlikely to cut rates or the RRR (reserve requirement ratio) for banks this month. However, on the stimulus front the big news is Beijing removing the country's 75% loan-to-deposit ratio which may allow the banking sector respond more promptly to monetary policy change. With worries of an overheated debt bubble, is this just fuel on the fire though?

In focus today we have more US macro data attempting to steal some of Greece’s limelight – personal income & spending expected to grow in May, jobless claims (initial looking up (bad), continuing down (good)) and PMI Services looking for an improvement.

Crude prices largely flat as traders wait it out with tanks at the US storage site in Cushing, Oklahoma almost full (despite an 8th straight decline in stockpiles) and talks being held between oil majors and Iranian officials in Tehran – the first time international oil groups have been publicly open about such endeavours. The spread between US WTI ($60) and Brent ($63) has now shrunk to $3 having been as much as $20 in 2013.

Gold bounced of $1170 thanks to weaker USD but has failed to regain $1180 despite Greek concerns. While the downtrend remains from recent $1204 highs the prospect of a sharp bounce as Greece edges towards default is quite possible.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – it’s all part of the service.

UK Company Headlines: (Source: Reuters/DJ Newswires/Bloomberg)

- John Wood Group sees H1 2015 results below yr ago

- Afren says COO David Thomas to join board as executive director

- FCA says debt management firms still failing UK's most vulnerable consumers

- DS Smith says FY reported revenue down 5 pct

- DS Smith strengthens Spain business with 190 mln euro deal

- UK Green Investment Bank reaches profitability, eyes stake sale

- Debenhams says on track to meet year expectations

- SkyePharma says FY trading in line with board's expectations

- London Stock Exchange says UK Index and Russell indexes making good progress

- John Wood Group enters into $250 mln deal with Antin Infrastructure

- Rare Earth Minerals says investments made good progress