Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

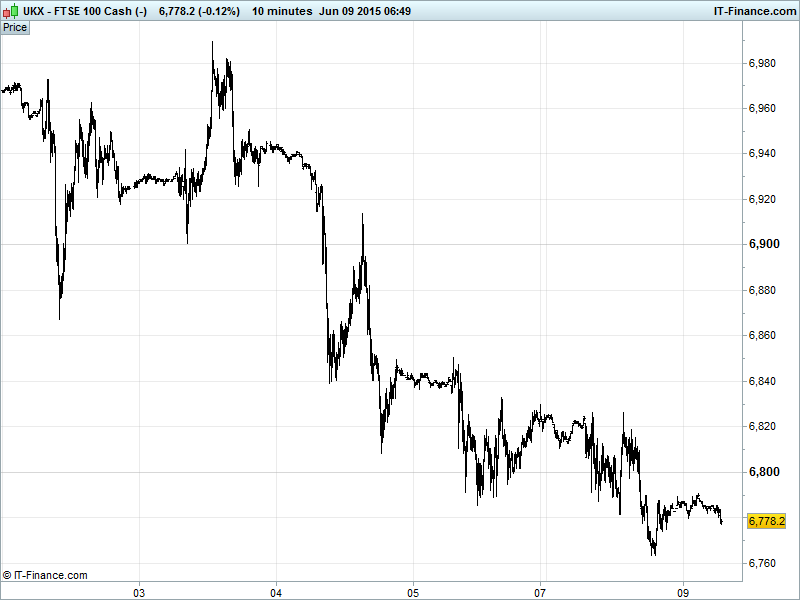

UK 100 Index called to open -5pts at 6785, with failure to progress holding the index in its downtrend from end-May. Overnight failure to regain 6800 keeps the index below 6810 May lows which may revert to resistance. Support around 200-day MA 6780 keeps bullish recovery hopes alive but for now the bears remain in control, still eyeing a breach of the 200-day MA and a revisit of 6670 April lows. Watch levels: Bullish 6835, Bearish 6755.

The mildly negative opening call comes after UK retail sales struggled to bounce in May from April’s sharp declines (despite consumer confidence approaching pre-crash levels) while the ‘pleading’ begins for Greece to strike a deal with creditors before the end of the month and the deadline for a bundled payment, some of which was not paid last Friday.

Markets are lacking confidence with Athens unwilling to ‘reach into the guts, heart and substance of the Greek private sector’ (paraphrasing Varoufakis) to implement growth-stifling Austerity measures. When you put it like that, Yanis…However, reports this morning that a bailout extension is being discussed lead us to expect more of what we’ve always got – a last minute lifeline; Greece to live to fight another day.

US bourses ended Monday’s session in negative territory with investors’ attention firmly fixed on their now familiar partnership-of-drivers (Greece and the US Federal Reserve). For the moment equities are under pressure with Dow Jones back in the red for the year to date on a strong dollar (though a little weaker after Obama’s ‘concern’ comments yesterday that were later denied) and with a first US interest rate rise heaving into view while negotiations in the Eurozone run short on time.

On the macro-front today we have the UK’s trade balance at 0930 looking to come in less negative than last month, and Eurozone GDP at 1000 expected flat. This afternoon sees US small business optimism where Fed hawks will be eyeing at least a hit on consensus, while a beat would almost certainly put a September rate hike on firmer foundations. With US wholesale inventories at 1500, it could pay to keep a watchful eye on the indices.

Asian equities are well in the red after a weak European/US finish. Disappointing China inflation data fanning flames of concern that demand cooling in world’s #2 economy and deflation pressuring prices while US prepares to hike rates, thus casting gloom over global economic outlook. Adding to the fray are worries about the Greece deadlock, the Ukraine/Russian situation and a USD reversal following Friday’s jobs report induced rally.

China inflation data delivered the slowest Consumer Price Inflation (CPI) since Jan’s 5yr low while Producer Prices (PPI) remained negative for a 39th straight month (<4% for last 5 months). Normally interpreted as stimulus and thus equity positive, data overshadowed by wariness to move ahead of the MSCI’s decision on including mainland equities in its indices, something which could see a big influx of foreign capital.

Japan’s Nikkei is the regional underperformer after the USD reversal saw the JPY strengthen at the expense of exporter stocks, consumer confidence remained depressed and comments from the Economy minister suggested Q1’s GDP growth may be unsustainable.

Hong Kong’s Hang Seng following Chinese equities lower on caution before the MSCI mainland verdict. Australia’s ASX the outperformer on China stimulus hopes, an improvement in business confidence, an unexpected jump in home loans and a rally in commodity prices thanks to the USD reversal.

Big UK Corporate news includes HSBC (HSBA) aiming for $5bn annual cost savings by 2017 (ironically costing $5bn to implement) cutting up to 25K jobs globally and selling businesses in Turkey and Brazil. The bank’s shares in Hong Kong are higher on the news. Watch the UK Retails after overnight BRC data showed UK sales failing to reverse April’s sharp falls in April despite consumer confidence at near pre-crisis levels.

Gold has found support at $1170 and rallied back towards $1180 thanks to the USD reversal making the yellow metal safehaven cheaper from a relative standpoint. Renewed interest also on Ukraine fears adding to those already firmly in place on Greece and Middle East. The downtrend from mid-May towards $1140 March lows still in play with resistance via falling highs likely around $1190.

Crude prices gained a few cents on Monday following poor China import data suggesting continued deflationary pressure and subsequent slump in demand from the world’s #2 economy and colossal consumer of raw materials. US benchmark WTI currently $59 while UK cousin Brent trading around $64 as a ‘believe it when I see it’ attitude prevails in the commodities sphere towards hopes of further stimulus.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – it’s all part of the service.

UK Company Headlines: (Source: Reuters/DJ Newswires)

- RPC Group FY revenue from cont ops rises 17%

- Creston full-year profits up 2%

- Fastjet says number of passengers carried up 52% in May

- John Menzies buys e-commerce logistics co for £7.5mn

- Plus500 updates on remediation plan for customers of Plus500UK

- Oxford Instruments full-year adjusted pretax profit falls