Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

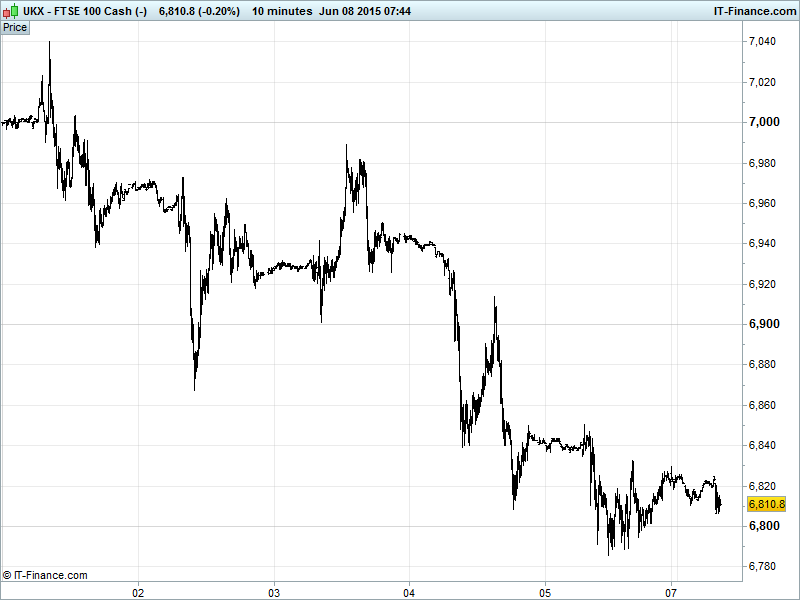

UK 100 Index called to open +5pts at 6810, hinting at recovery from its drop to 6800 but yet to deliver a decisive rebound with downtrend from end-May as yet unperturbed. Bulls still hoping for reversal and 250pt recovery towards 7050 while Bears egging the index on for another downside leg (130pts to April lows 6670), although watchful of 200-day MA 6771 for support. Watch levels creeping down: Bullish 6855, Bearish 6775.

The positive opening call comes after a choppy week with markets spooked – mainly by Greece but with consensus–beating US non-farms aggravating worries as fickle investors pre-empted a September interest rate rise on the other side of the pond.

There being no precedent to current issues within the Eurozone, no-one is sure how the situation will pan out with Greece making use of loopholes to extend deadlines and frustrated creditors seemingly underestimating the scale of the challenge in getting their proposals past a defiant Syriza party at large.

Following Friday’s postponement of a €300mn IMF payment, Athens is left with little time to make things right – a statement oft put forward by commentators but one which has yet to deliver any meaning in the form of either a deal or a complete breakdown in negotiations and subsequent ‘Grexit.’

US bourses closed mixed on Friday (Dow Jones -0.3%, S&P -0.1%, NASDAQ +0.2%) after a strong jobs report, seemingly taking account of the small uptick in the unemployment rate and, surprise surprise, Greece. Bearish sentiment just about winning out after the non-farms print was taken as a sign of an impending US Fed rate hike, rather than a rosy outlook for the US economy.

Asian equities offering mixed performance and divergent responses to macro data with Japan’s Q1 GDP upgrade taken as stimulus negative while China’s disappointing May trade data (export declines eased, but still down for 3rd month; imports plunged in spite of government assistance) is seen underscoring a sluggish domestic economy and pushing Beijing to bolster economic support.

This all the while dealing with Friday’s better than expected US jobs report which supports the case for the Fed raising rates this year and the Greek-Troika standoff saga showing no signs of abating with both sides claiming only their proposals are realistic and the EC President refusing to speak with Greek PM until Athens deliver already delayed proposals.

Japan’s Nikkei just the wrong side of breakeven despite a weak JPY (13yr low, thanks to US jobs report strengthening USD) with investors looking past the Q1 GDP revision and focusing on signs of a slowing in Q2. Stocks in China outperforming to 7yr peak on stimulus hopes and Hong Kong’s Hang Seng doing well as a result. Note Australia’s ASX closed.

Today’s limited macro-data has already seen some good German figures with its industrial production and trade balance beating expectations while the Chinese trade balance increased dramatically due to a fall in exports and an even bigger fall in imports (meaning the data is more bad than good…). This will likely be met, as it often is, by market confidence in further stimulus from the world’s #2 economy and major consumer of basic materials. Watch UK Index miners this morning.

Elsewhere, US labour market conditions has no consensus but will likely be eyed closely for its potential as an indicator of US economic health and to influence the capricious equity markets accordingly (and possibly counterintuitively).

Safehaven Gold being held back by US jobs report strengthening the USD and making the yellow metal more expensive to non-USD buyers. Off its lows after breach of $1170 support, but still in downtrend from mid-May with the sell-off towards March lows $1140 accelerating. Now well below major moving averages. Greek saga could make things either better or worse depending on how you are positioned.

Crude prices remain within sideways channels as does the US dollar basket as global supply glut concerns play the reality to OPEC’s dreamland populated by oil bulls. Brent crude around $63 this morning while US cousin WTI trading at $58.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – it’s all part of the service.

UK Company Headlines: (Source: Reuters/DJ Newswires/Bloomberg)

- Victoria Oil & Gas starts natural gas supply to 3 new customers

- Asia Coal Energy raises takeover offer for ARMS

- Phoenix IT swings to full-year profit

- Power producer Drax takes further hit from weak prices

- Drax FY Expectations Unchanged Despite Weak Power Market

- Sound Oil PLC Moroccan Country Entry - Signature of Farm In