Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

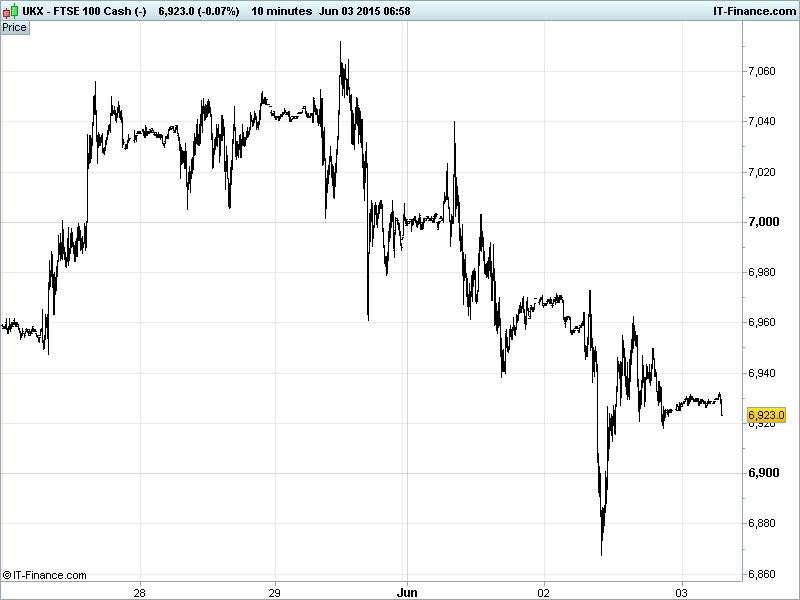

UK 100 Index called to open -3pts at 6925 after a decisive test of key rising support dating back to early April. The sharp bounce gives hope to bulls looking for a recovery, however, the break below 6930 suggests desire for continuation of current downtrend from 7050 highs and completion of a 7-day double-top. Still at lower end of longer-term converging pattern with potential already shown for a move lower. Watch levels: Bullish 6960, Bearish 6860.

The flat opening call comes after more choppy trading conditions for the UK Index on Tuesday as markets awaited an outcome to the Greek situation that never arrived. It’s widely believed that a ‘take it or leave it’ proposal will be presented to Athens today by creditors (according to a FT reporter on Twitter…) while Alexis Tsipras is said to have delivered his own proposal to the Eurogroup. Bored investors decided to turn their attention to the US Fed’s Brainard whose dovish chatter took over in the afternoon to massage European markets into the close.

US equities put in a modest Monday performance with the main driver being Greece once again but any hopes of a positive close dashed by some weak macro data – factory orders unexpectedly falling in April while both economic optimism and ISM New York missed consensus. A poor Q1 became a poor H1 performance (temporary factors not so ‘temporary’ after all), giving support to Brainard’s dovish comments about the need for ‘watchful waiting’ ahead of any potential Fed rate hike.

Asian stocks in the red, following cautious US and Europe trading sessions, as the saga of the Greek standoff with creditors persists, laborious negotiations go on and the possibility of Athenian default draws ever closer. Japan's Nikkei lower for a second day on account of weak US data taking the USD lower and strengthening the JPY at the expense of the earnings outlook for exporter names, and despite an improved PMI Manufacturing read overnight.

Chinese equities losing ground despite positive HSBC Services PMI data showing expansion for the fourth consecutive month in May and the fastest growth in 8 months, however, a drop in the composite read highlights continued weakness in the key manufacturing sector. As usual, given China's importance in terms of global growth, data being taken as stimulus negative rather than economic positive. Welcome to the new world!

Australia's ASX suffering from a stronger AUD and annual GDP growth falling further below trend despite a quarterly acceleration (pick up in mining export, household spending) with the response to China data likely weighing. This despite a positive performance by dual-listed miners in London yesterday.

In Focus today in Europe we have Services PMI prints from the UK and Eurozone with the latter’s unemployment rate and retail sales coming in at 10am. US MBA mortgage applications, ADP employment change (non-farms warm-up), trade balance and its own services PMI are the highlights this afternoon. See the live macro calendar for a full rundown with consensus.

US Light Crude ($60) broke out above resistance to the upside to re-test the $61.7 level before the dollar basket found support to cap further gains. Meanwhile, UK benchmark Brent ($65) tested its own resistance twice with a double top formation before returning, like its US cousin, to trade roughly where it was yesterday morning.

Core OPEC members have made it clear that it will continue to pump oil at the current rate in defence of its market share despite partners, including Venezuela (90% export receipts from oil), calling for a slowdown to boost prices. A senior delegate is said to have given a bullish outlook for a still oversupplied market while analysts are starting to seriously look at the prospect of OPEC actually hiking production. Bullish for whom, exactly?

Gold still holding on to the $1190 level, inching higher and refusing to give up the rising trend from mid-March. Interestingly the USD was less of a driver yesterday, suggesting the Greek saga taking priority. Support 1185, resistance 1195 as the yellow metal trades within a very tight range.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – it’s all part of the service.

UK Company Headlines: (Source: Reuters/DJ Newswires)

- BHP Billiton warns global commodity supply glut to persist

- Costain JV wins road improvement contract worth up to £600m

- Mears says trading in line with management expectations

- Ireland's Cairn Homes eyes London listing, seeks at least €350m

- Annual UK house price growth slowest in nearly two years – Nationwide

- Kier completes rights issue to fund Mouchel acquisition

- Dixons Carphone raises profit guidance on strong trading

- WH Smith says total group sales +1% for 13 weeks to 30 May

- Royal Mail names TUI boss Long as new Chairman

- IT security provider Sophos plans London IPO

- Workspace says FY pretax profit +43% to £360m

- UBM Acquires Brazilian Healthcare Trade Show for Undisclosed Sum

- Interserve JV named One Nine Elms preferred bidder

- Sterling Energy Acquisition of interest in Block C-10, Mauritania