Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

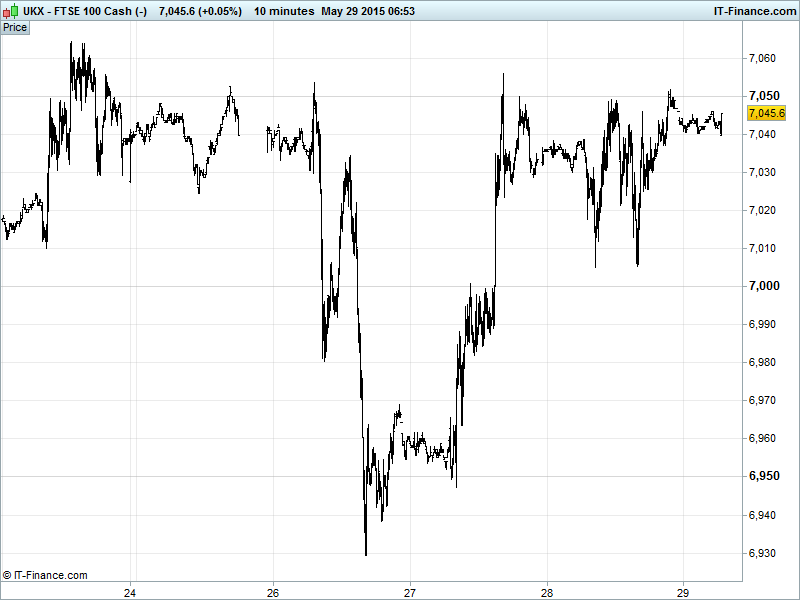

UK 100 Index called to open flat at 7040, with the index holding up around recent highs, and in a very narrow range overnight, showing appetite to break higher, but still failing to make any headway with April falling highs resistance. Potential for recent activity to be bullish reverse head and shoulders pattern which breaks 100pts to the upside. Greek headlines likely to decide? Watch levels: Bullish 7075, Bearish 6995.

The flat opening call comes after a choppy session yesterday that saw UK 100 sell off in the afternoon on the back of a disappointing US open with confusion rife surrounding Greek debt talks and a crisis in Chinese equities. The IMF is suggesting this morning that a deal between Athens and its creditors is unlikely by Sunday, and that it cannot rule out a Greek exit from the Eurozone as a possible outcome.

The EU’s Moscovici has been somewhat more upbeat with his outlook, suggesting that the Eurogroup is committed to seeing Greece remain in the fold despite there still being much work to do. Moscovici is the first to give his thoughts this morning. Expect more as the day evolves with potentially volatile trading to boot.

US markets receded yesterday to close lower with equity markets spooked by the Chinese sell off and Greece. San Fran Fed Pres John William echoed Yellen suggesting a US rate rise later this year is likely while Kocherlakota remained dovish on 2015 citing a loose labour market and lacklustre inflation. But all this talk of when a hike will happen is now meaningless and slightly tiresome. It’s going to happen and the issue is not when, but how. Wake us up when you can tell us that, Messrs. Fed.

Asian equities positive overnight, despite negative lead from Europe and Wall St (Greek uncertainty, mixed macro data, M&A, US rate rise), with weaker USD (profit taking ahead of potential weekend Greek deal strengthening EUR) and higher commodities prices (US oil inventories fell; barrel +2$) boosting resources names.

Fed chatter (William echoing Yellen’s caution; Kocherlakota dovish; Bullard policy not helped) also offsetting market uncertainty and choppy trading in China (more stimulus?) following yesterday’s equity sell-off and Shanghai’s brief flirtation with reversal and technical correction. End of bull-run?

Japan’s Nikkei extending winning run thanks to still weak JPY (even if it has rebounded from lows), still subdued inflation supporting continued stimulus, a rebound in industrial production and improved jobs data. Australia’s ASX outperforming led by banks, 1% fall in AUD and new home sales hitting 5yr high, offsetting poor private sector credit and business surveys.

In Focus today we have US GDP at 1330 with expectations for a contraction on the year, Chicago PMI at 1445 looking for an improvement in May (that’s only Chicago, though), University of Michigan Confidence also looking up. The Baker Hughes Rig Count rounds off the afternoon at 1800.

Gold flat around $1190 despite USD coming off its highs with safehaven tug of war between optimists and pessimists on whether a Greek deal is round the corner or not. Weakness saw test of March raising lows and support kick in at 2-month lows $1880. 2-month sideways trend intact, but can it counter the Downtrend and falling highs from mid-May?

Talking all things oily, both Brent ($64) and US benchmark WTI ($58) made a bounce off support levels around $61 and $56 respectively yesterday as US stockpiles fell more than expected. Both off overnight highs this morning amid record outflows from the biggest US Oil ETF, the United States Oil Fund, raising concerns that 2015’s 30% rally is set to stall.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – it’s all part of the service.

Key Overnight Macro Data: (Source: Reuters/DJ Newswires)

- UK GFK Consumer Confidence Miss, deteriorated

- Japan Employment Beat

- Japan Consumer Price Inflation Beat, slowed less

- Japan Industrial Production In-line, rebounded

- Germany Retail Sales Mixed

See Live Macro Calendar for full data line-up, incl. consensus expectations

UK Company Headlines: (Source: Reuters/DJ Newswires)

- Sabadell extends TSB offer timetable as approval process continues

- Allied Irish Banks appoints Bernard Byrne as CEO

- Afren noteholders agree to subscribe to notes of up to $369 mln

- British Land lets about 100,000 sq ft at Leadenhall building

- Synergy Health says FTC intends to seek to block Steris deal

- Monitise updates on payment of deferred consideration for Monitise Yazilim deal

- AstraZeneca to collaborate with Lilly on solid tumours clinical trial

- Equinix agrees to buy Telecity Group for 2.35 bln pounds