Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

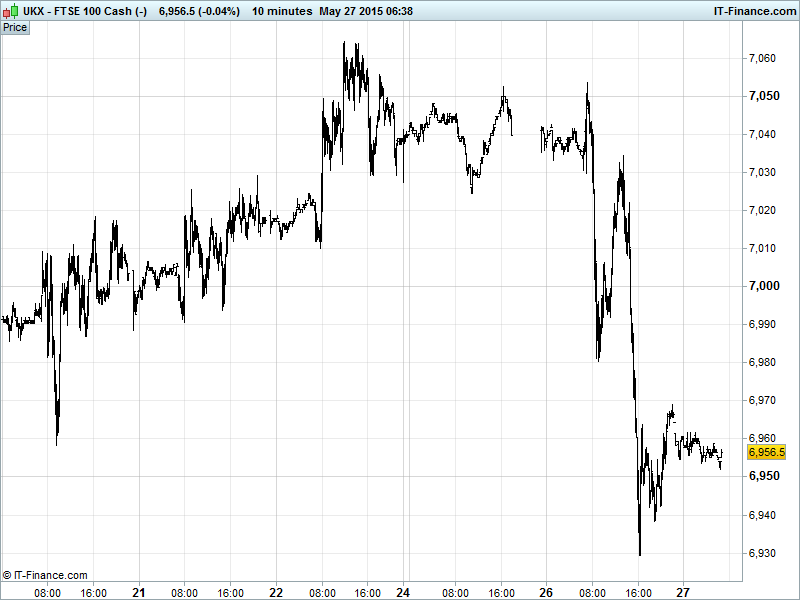

UK 100 Index called to open +10pts at 6960 having found support at 6935 100-day MA following sharp sell-off from April falling highs 7050 yesterday. While this puts paid to the trend of rising lows from May 7, the longer term uptrend from mid-December remains alive even if in competition with downtrend from mid-April. New watch levels: Bullish 6990, Bearish 6920.

The positive opening call comes after the UK 100 pulled back to 3-week lows on Tuesday as mild panic entered the markets with Greece again at the forefront of investor sentiment. As a June deadline approaches for Athens to make its next IMF repayment, both the Greek government and its creditors are scrambling to ease fears of an imminent default and potential exit from the Eurozone.

FM Varoufakis is confident as usual – and maybe rightly so given the implications of a Grexit, ever more probable while remaining the worst possible outcome, for other struggling economies Spain and Portugal. ‘What about us?’

US markets have also taken a break from declines overnight after joining UK stocks in Southerly moves yesterday – Greece weighing there too while a dovish Lacker of the Fed again put a June interest rate rise back on the table, citing a perceived rebound from a weak Q1 with inflation picking up and oil prices….firming?

Asian equities in the red, following European and US markets lower, perturbed by Greece’s proximity to a June 5 cash crunch and/or default, contagion fears following Spanish regional elections demonstrating austerity rejection and heightened expectations that the US Fed will raise rates this year, derived from better US data and comments from the Fed’s Lacker who said a June hike should be considered.

Japan’s Nikkei just above water, holding a 9-day rise, despite USD strength (driven by US data, US rate rise expectations and EUR weakness) taking JPY weakness close to levels last seen in June 2007 - something which would normally benefit exporters. Good news with Small Business Confidence rising more than expectations although tempered by a calm BoJ despite subdued inflation, and suggestions of no new easing.

Chinese equities taking their winning streak to 6 days after China Industrial Profits rebounded in April and Consumer Sentiment was stable with a drop in business optimism offset by a rise in consumer willingness to spend before the recent rate cut. Supportive stimulus hopes persist as questions remain over the strength of underlying growth in the world’s #2 economy.

Australia’s ASX is the region’s major underperformer, despite an uptick in the economy’s Leading Index turning higher, with energy names held back by a strong USD hindering commodities prices and after construction work data plunged, extending its weak 2014 trend. China stimulus hopes and Industrial Profits rebound offering no assistance despite the two nation’s export links.

In Focus today we have a quiet one with Spanish mortgage lending at 0800 - no specific expectations but surely hopes it will remain in growth mode after the last print’s impressive 30% improvement in house mortgage approvals. US mortgage applications follow at 1200 with the Bank of Canada rate decision at 1500, no change expected at 0.75%.

Gold has bounced at $1185 thanks to rising support dating back to mid-March, and despite continued USD strength which would normally hinder the dollar-denominated safehaven commodity. Having fallen through the major moving averages, watch for these serving as resistance on any run higher. Support $1185, Resistance $1205.

Crude prices still trending down in characteristically volatile style. The prospect of Shell commencing drilling in the Arctic circle will bode well for US energy security while putting pressure on global prices as yet more oil finds its way into the market. Note Saudi Arabia likely to react accordingly to a challenge to its market share. US light ($59) and Brent Crude ($65) trading up a little this morning while remaining well within falling channels since those late April/early May highs.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – it’s all part of the service.

Key Overnight Macro Data: (Source: Reuters/DJ Newswires)

- Australia Westpac Leading Index Rebound

- Australia Construction work Miss, deteriorated further

- China Industrial Profits Rebounded

- China MNI Consumer Sentiment Unchanged

- Japan Small Business Confidence Beat, Improved

- Germany GFK Consumer Confidence Beat, improved

See Live Macro Calendar for full data line-up, incl. consensus expectations

UK Company Headlines: (Source: Reuters/DJ Newswires)

- Irish govt backs sale of Aer Lingus to BA-owner IAG

- A.G. Barr says on track to meet full – year expectations

- Rolls-Royce wins €80mn military contract

- Polypipe says UK operations revenue up 6.3% for first four months of 2015

- Plus500 says trading hit by recent problems

- Hansteen buys 13 properties in Germany for €21.7mn

- APR signs deal with Botswana Power Corporation and National Electric Utility

- Brewin Dolphin posts 9% jump in adjusted H1 pretax profit

- Fitbug Holdings finance director to leave

- Workspace buys property in Clerkenwell, London for £16.6mn

- Arrow Global Q1 adjusted EBITDA rises 41%

- Card Factory says expectations for full year remain unchanged

- London housing shortage helps boost Telford Homes profits

- Wizz Air FY profit soars, sees more growth in 2016

- De La Rue posts 22% fall in operating profit